A November Inflation Rebound Is Nothing to Fear

· Fed services and manufacturing survey data indicate inflation eased in November.

· That implies little change for the November data compared to October.

· The six-month average would imply annualized growth is around 1.4%

Inflation growth is about to rise again…

This is another important week for the monetary-policy outlook. On Wednesday, the U.S. Bureau of Labor Statistics (“BLS”) releases its consumer price index (“CPI”) update for November. This will be the last major piece of economic data the Federal Reserve receives before making its next interest rate decisions at the December 17-18 meeting of the Federal Open Market Committee (“FOMC”).

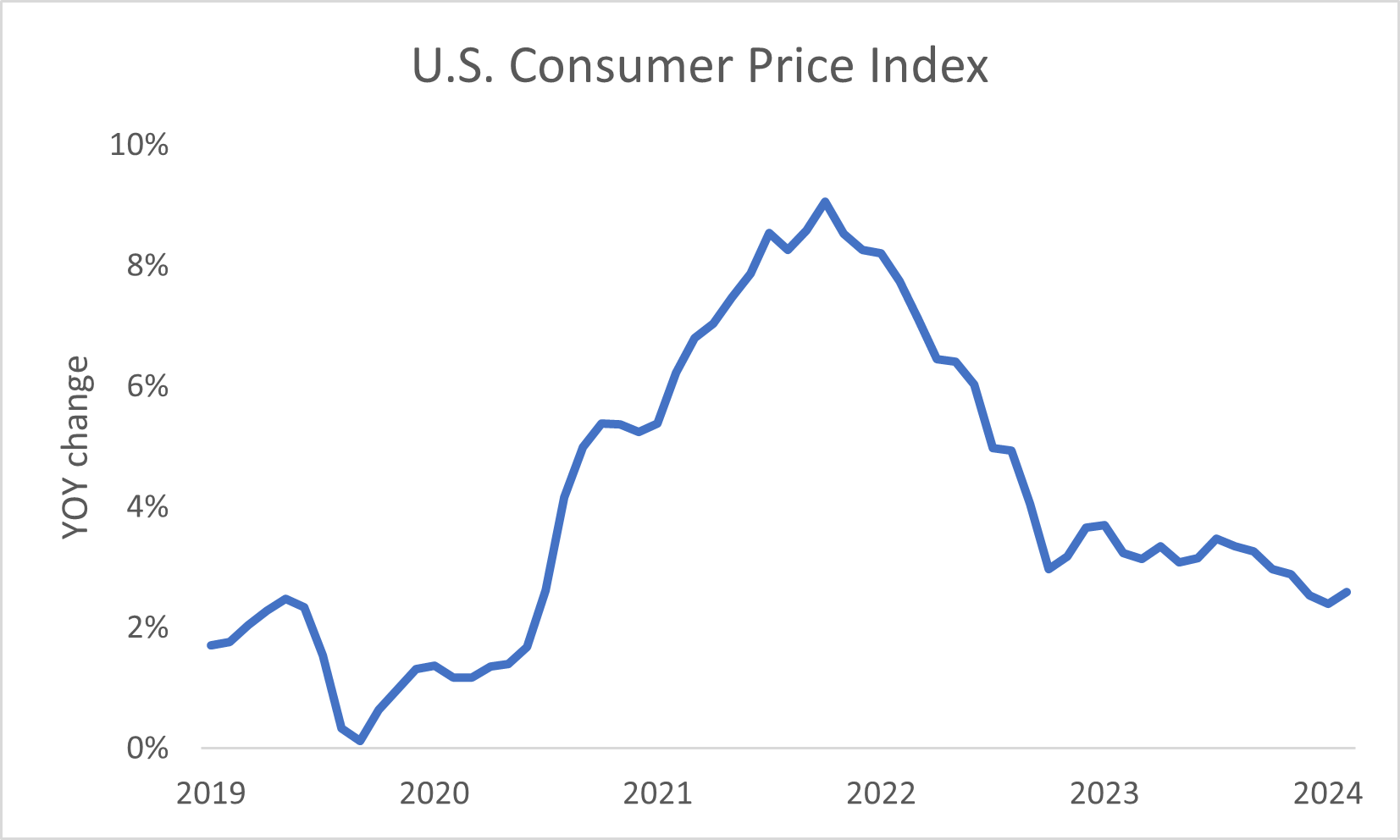

Until recently, price pressures had been steadily easing. Headline CPI got as low as 2.4% on an annualized basis in September. That was the closest we’ve been to the central bank’s 2% target since February 2021. Yet, last month, the measure rebounded, worrying investors inflation is about to take off.

However, those fears appear overblown. Over the next couple of months, we’re losing the weakest monthly growth numbers from the last year. Due to the way annualized data is measured, it’s going to make price pressures seem like they’re accelerating. Yet, at the start of next year, the highest monthly growth data is going to start disappearing.

Based on recent data I’ve been observing, prices barely budged last month. That means the pace of growth should be in-line with October’s 0.2% increase. That implication being headline inflation numbers should rapidly drop when we start to lose the high monthly comps at the start of next year. The change will support more Fed rate cuts, underpinning a steady rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

Every month, a number of regional Fed banks reach out to manufacturing and services companies in their districts. They ask those businesses about the level of activity they’re seeing. They want to gauge whether commerce has improved, worsened, or stayed the same.

I like to follow the results from the Dallas, Kansas City, New York, and Philadelphia Fed banks. Those four districts combine for about 25% of national gross domestic product. By looking at the results we can get a sense of what’s transpiring nationally. In addition, the data comes out just before the end of each month, so it’s like having an early look into what might unfold when entities like the BLS release market-moving data.

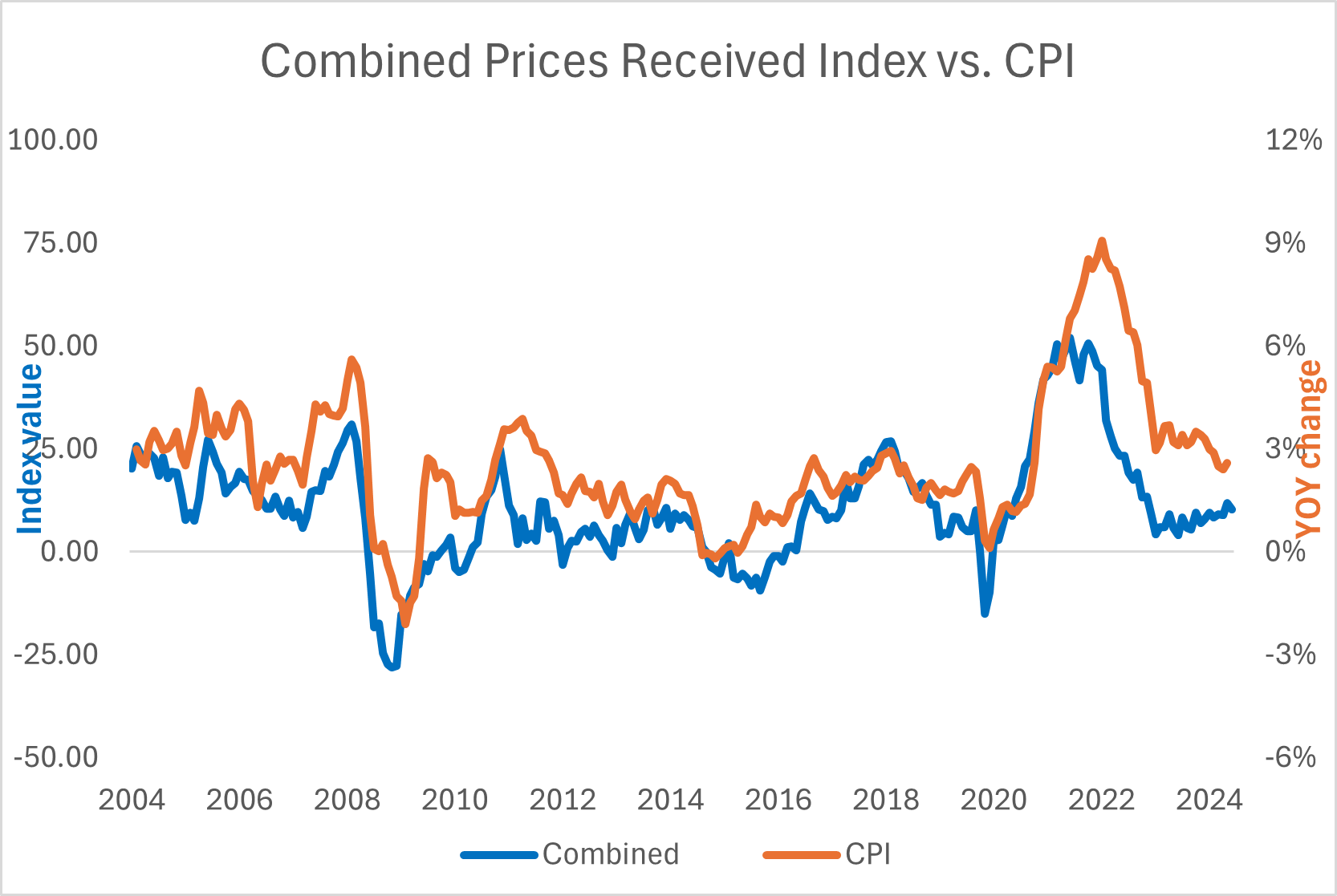

Today, we’re focusing on the prices-received results. The reading measures what those companies’ customers are willing to pay for the goods or services they’re buying. So, it’s akin to CPI. I want to break it down by the individual parts and then consider them together. So, let’s start with the manufacturing survey results…

As you can see in the above chart, the prices received gauge tends to be a leading indicator of inflation. Back in April 2020, the measure hit the cycle low just ahead of CPI. Then in November 2021, the gauge peaked about seven months prior to national prices. Ever since, our manufacturing index has been headed lower.

As you’ll notice on the right side of our graph, prices received have been stabilizing. The trend began in July 2023 and has been holding steady. And this past month is no different. My combined manufacturing index had a reading of 10.4 compared to 11.8 in October.

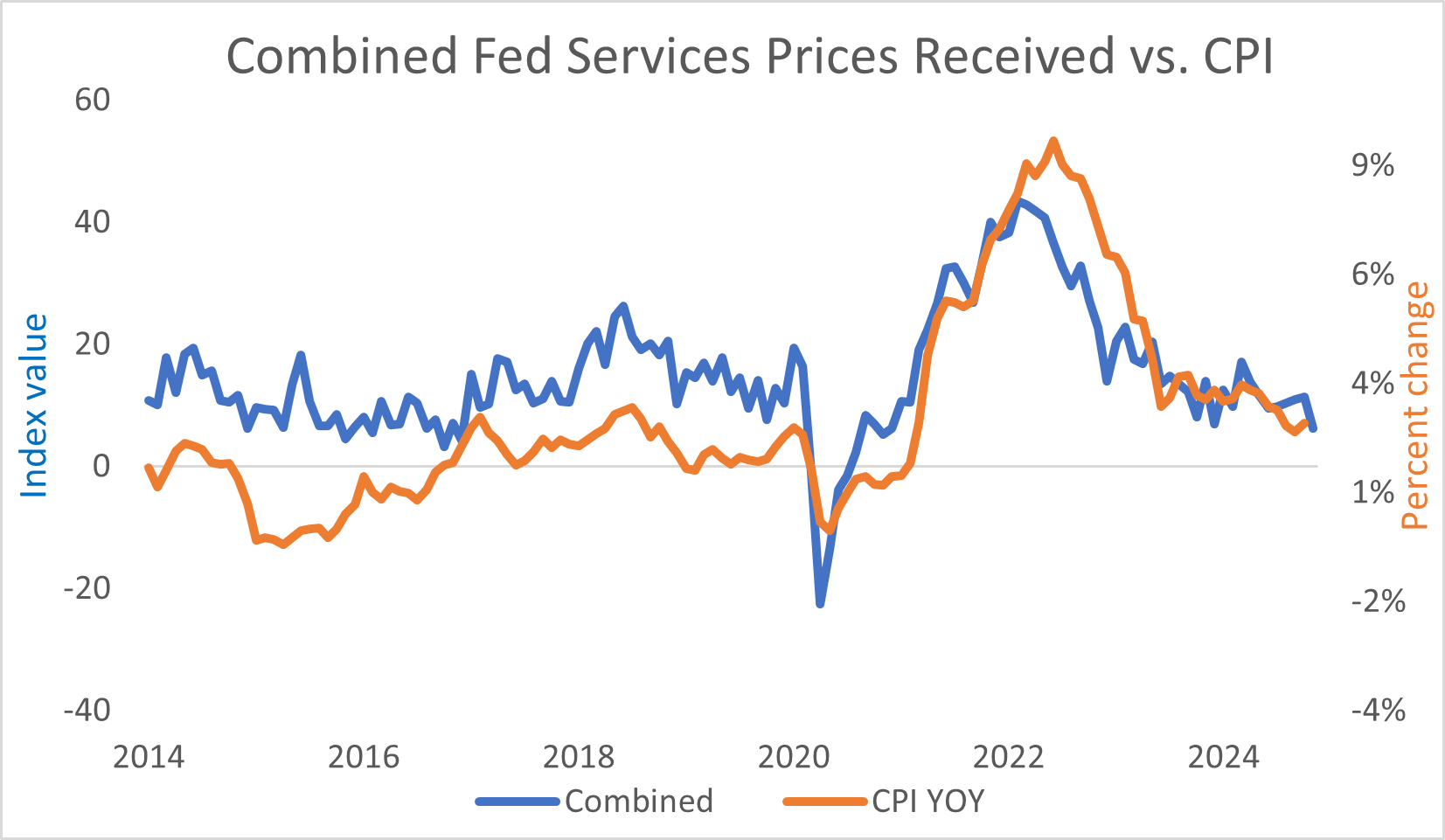

The story’s similar for the services sector surveys. Take a look…

Like the manufacturing data we previously studied, we can see that service sector hiring tends to closely track with the broader national picture. The combined index data rose ahead of domestic numbers several years ago, but ever since have led it steadily lower. And now, it appears to be flat lining. In fact, the services gauge was almost cut in half this past month, falling from 11.4 in October to just 6.3 in November.

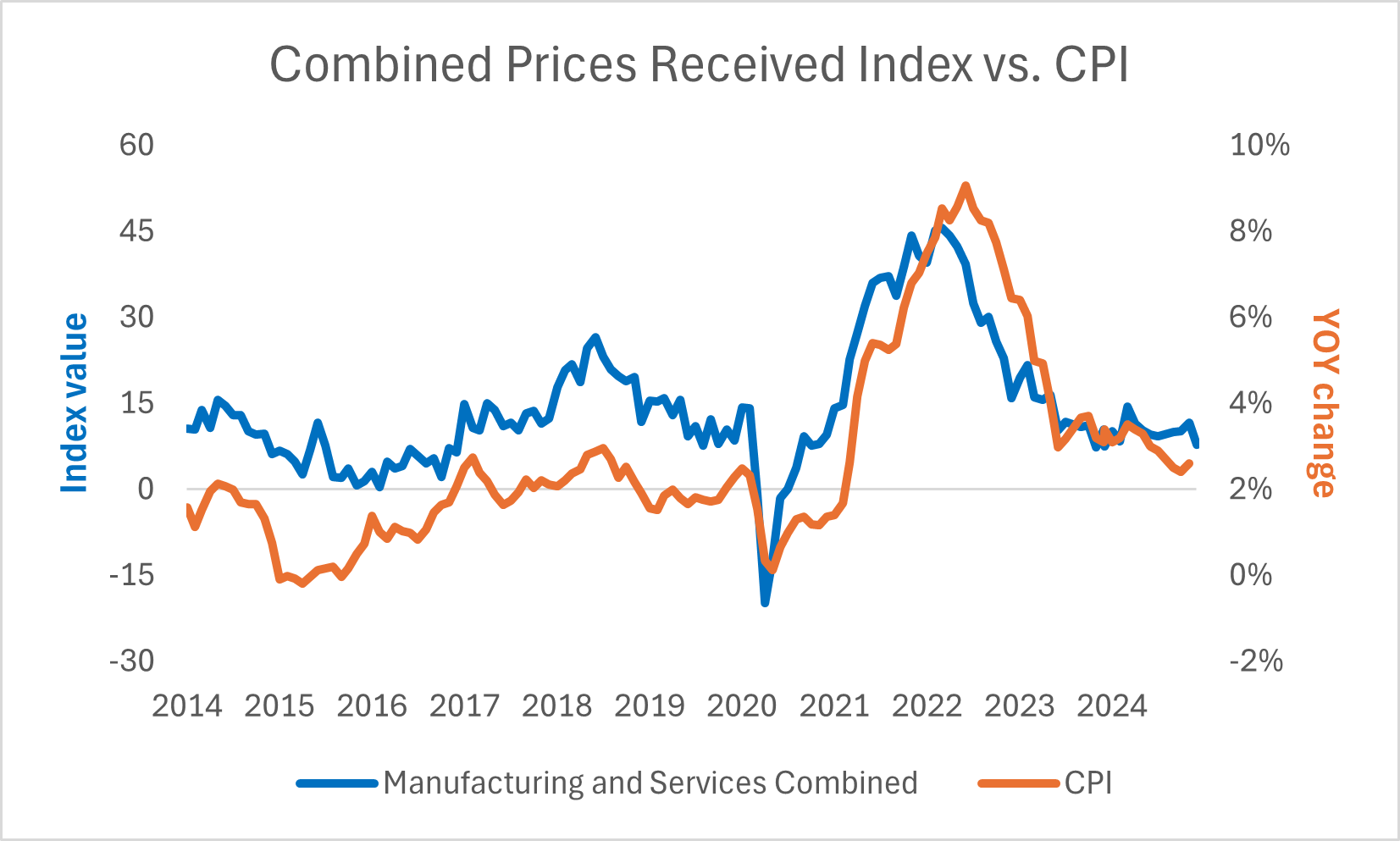

However, I wanted to take it one step further. I combined both the services and manufacturing results to give us a more complete picture…

For this combined measure, I tried to give the two indexes a weighting similar to what each would receive from the BLS. I weighted services as 65% of the average and goods at 35%. Again, the combined index tracks very closely with headline inflation, leading it higher and lower.

According to my results, the combined prices-received index dropped in November compared to October. In fact, it hit the weakest level we’ve seen since December 2023. That tells me we shouldn’t see a similar result to the 0.2% increase experienced just last month.

If that proves to be the case, it will mean the six-month average rate of growth for CPI is 0.12%. If we annualize that out over 12 months, that gets us to a 1.4% rate of annual growth.

We care because that type of growth is far below current levels and well below the central bank’s 2% target. Remember, like I said at the start, at the start of 2025, we’ll start to lose the highest inflation readings from early 2024. In fact, if the current pace of growth holds, we could see annualized numbers drop below 2% as soon as February or March.

That’s a huge deal for the monetary policy outlook. Currently, Wall Street is only pricing in two rate cuts next year… one in March and another in June. If inflation growth starts to plummet, that outlook should change in a hurry. Because the gap between price growth and borrowing costs would expand rapidly. That would mean the cushion for rate cuts is rising. Then, two reductions could quickly become four.

So, don’t be surprised when we receive data on Wednesday that makes CPI looks like it’s rising. But instead of being caught up in the here and now, look ahead to where the conversation is going. Because the outlook should point to stable economic growth, underpinning a steady rally in the S&P 500.

Five Stories Moving the Market:

China's consumer inflation hit a five-month low in November as fresh food prices pulled back while factory deflation persisted, suggesting Beijing's recent efforts to shore up faltering economic demand are having only limited impact – Reuters. (Why you should care – the data point to the need for more stimulus from Beijing or run the risk of economic growth worsening)

Japan’s economy grew at a faster pace than initially estimated, indicating more strength in the recovery; Japan’s gross domestic product grew at an annualized pace of 1.2% in the three months through September from the previous quarter, compared to the preliminary estimate of 0.9% - Bloomberg. (Why you should care – the upward revision to economic growth is likely to support Bank of Japan rate hikes)

Syrian President Bashar al-Assad’s government has fallen after a stunning territorial advance by opposition groups over the past few days; Assad and his family arrived in Moscow, where they were granted asylum by the Russian government – Bloomberg. (Why you should care – the development points to the weakened state of Iran and Russia’s military due to drawn out conflicts with Israel and Ukraine)

President-elect Donald Trump called for an immediate ceasefire between Ukraine and Russia to end “the madness” in the region; the announcement came hours after Trump met with Ukrainian President Volodymr Zelenskyy in Paris – USA Today. (Why you should care – a cease fire would be the first step in negotiating a peace deal)

China's central bank resumed buying gold for its reserves in November after a six-month pause, official data by the People's Bank of China (PBOC) showed; the PBOC was the world's largest official sector buyer of gold in 2023 – Reuters. (Why you should care – the resumption is likely a signal China will keep building reserves despite higher prices)

Economic Calendar:

China – CPI, PPI for November

Japan – GDP for 3Q

Eurozone – Sentix Investor Confidence for December (5 a.m.)

U.S. - NY Fed Consumer Inflation Expectations (9 a.m.)

U.S. – Wholesale Inventories for October (10 a.m.)

Treasury Auctions $81 Billion in 13-Week Bills (11:30 a.m.)

Treasury Auctions $72 Billion in 26-Week Bills (11:30 a.m.)