Don’t Expect A Hiring Rebound in June

Services and manufacturing surveys show hiring worsened in June.

Labor gains this year continue to fall behind pace.

The slowdown will increase pressure on the Fed to cut rates.

June is typically a robust month for job gains—but that doesn’t appear to be the case this year.

This week brings a key update related to the economic growth outlook. On Thursday, the U.S. Bureau of Labor Statistics (BLS) releases its payroll data for June. Wall Street is expecting an increase of 120,000 jobs. If that proves correct, it will be a major letdown compared to the typical June increase of 295,000 employees since 2015. It would also establish the weakest annual pace of hiring we've seen during that period…

This year is already off to a rough start, based on data through May. Businesses have added just 619,000 new employees in the first five months of the year—compared to an average gain of 1,308,000 since 2015. That means we’re nearly 700,000 hires behind the typical pace. In other words, job gains in the second half of the year would need to be exceptionally strong just to reach a “normal” annual total.

As the chart above shows, June tends to be one of the easiest months to find gainful employment. Yet based on recent Fed business surveys, that wasn’t the case this year. Hiring appeared mediocre at best. If the national numbers confirm that, it will imply the economy is still losing momentum. That would strengthen the case for additional interest rate cuts from the Federal Reserve later this year—and could support a steady rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

Every month, several regional Fed banks reach out to manufacturing and services companies in their districts. They ask those businesses about the level of activity they’re seeing to gauge whether commerce has improved, worsened, or stayed the same.

I follow the results from the Dallas, Kansas City, New York, and Philadelphia Fed banks. Together, these four districts account for roughly 25% of national gross domestic product. I focus on the employment and inflation components of the data. By analyzing the results, we can get an early read on national trends—especially since this data is released just before month-end, ahead of market-moving reports like those from the BLS.

Today, we’re focusing on employment. Let’s break down the individual components before looking at the broader picture.

Starting with the manufacturing surveys…

The chart above shows the hiring trend in the sector since early 2019. After the pandemic collapse, factory hiring surged. But since then, the numbers have gradually eased. On the right side of the chart, you’ll notice that since peaking in January, manufacturing employment has been declining. This likely reflects increased adoption of artificial intelligence and uncertainty around tariff policy. According to the Fed’s manufacturing data, hiring contracted last month.

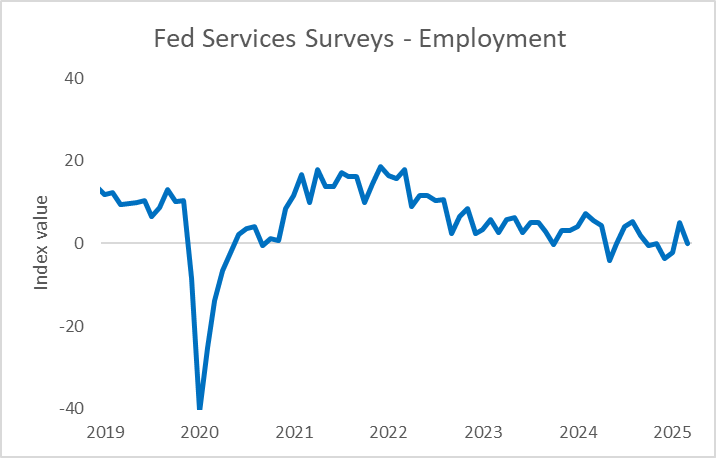

Now let’s turn to the services sector…

The chart above shows that services-sector hiring weakened in June. While the index didn’t dip into negative territory like manufacturing, it barely stayed positive. In fact, if not for hiring in the Kansas City district, the gauge would have declined. Again, uncertainty around trade negotiations and the looming July tariff increases likely caused companies to hold off on adding staff.

To get a clearer national picture, I combined the two data sets into a single chart. Based on the domestic employment breakdown, I weighted the services data at 80% and manufacturing at 20%...

In the chart above, I used a three-month rolling average to smooth out volatility and better capture the trend. As you can see, the combined Fed survey data tends to lead to national hiring. The three-month average rose in December—just ahead of a strong nonfarm payrolls report. But it rolled over at the start of this year. In June, the three-month average barely remained positive.

Bottom line, manufacturing and services employment continues to slow. If the BLS confirms this trend later this week, it will mean the hiring pace is falling further behind the historical norm.

So, if we get weak data on Thursday, don’t be surprised if Wall Street’s expectations for rate cuts shift again. Fed officials like Chair Powell and Governor Christopher Waller have signaled they’re open to easing policy if employment falters. That would likely push borrowing costs lower and support a continued rally in the S&P 500.

Five Stories Moving the Market:

Federal Reserve Chair Jerome Powell kept his monetary policy options open, saying steady economic activity was giving the central bank time to study the effects that tariff increases have on prices and growth before resuming interest-rate reductions - WSJ. (Why you should care – Powell said he wouldn’t take any meetings off the table as it relates to easing rates)

Bank of England Governor Andrew Bailey said Britain's softening labor market and rising uncertainty in the global economy had "definitely" hurt economic growth and investment intentions; while speaking at the ECB’s Central Banking Forum in Sintra, Portugal, Bailey emphasized the downward risks to Britain's economy rather than the threat of inflation – Reuters. (Why you should care – Bailey said the BOE will continue to lower interest rates gradually)

Sweeping tax legislation passed by the Senate would make it cheaper for semiconductor manufacturers to build plants in the U.S., delivering a win to chipmakers and boosting U.S. efforts to expand the industry domestically – Bloomberg. (Why you should care – the proposal would increase the investment tax credit from 25% to 35%, encouraging companies to break ground by next year)

U.S. manufacturing remained sluggish in June, with new orders subdued and prices paid for inputs creeping higher, suggesting that the Trump administration's tariffs on imported goods continued to hamper businesses' ability to plan ahead – Reuters. (Why you should care – the outcomes are likely to weigh on future hiring plans)

The Bank of Japan’s key interest rate is below the level at which it neither stimulates nor restricts growth, while underlying inflation is set to rise slowly, according to Governor Kazuo Ueda – WSJ. (Why you should care – the statement implies the BOJ is likely to raise interest rates even more, causing the yen to rally)

Economic Calendar:

South Korea – CPI for June

ECB’s de Guindos (Vice President) Speaks (4 a.m.)

Eurozone – Unemployment Rate for May (5 a.m.)

ECB’s Lane (Chief Economist) Speaks (6:30 a.m.)

U.S. - MBA Mortgage Applications (7 a.m.)

U.S. – Challenger Job Cuts for June (7:30 a.m.)

U.S. – ADP Employment Change for June (8:15 a.m.)

ECB’s Lagarde (President) Speaks (10:15 a.m.)

U.S. - Energy Information Administration Crude Oil Inventory Data (10:30 a.m.)