*Editor’s note: There won’t be any commentary from 8/1 through 8/8.

Duration Dialed Down: Macro Signals from the QRA

The Treasury releases quarterly refunding details on Wednesday.

Expect it to remain focused on short-term borrowing.

The plan should help to ease long-term yields.

U.S. sovereign bond yields face another important hurdle tomorrow…

Since taking office in January, Treasury Secretary Scott Bessent has pursued one clear goal - lowering the yield on 10-year U.S. Treasurys. He has continued to emphasize that doing so would ease borrowing costs for households and businesses, given that this rate underpins many types of loans. The White House, he said, is committed to using every tool at its disposal to influence long-term yields.

Initially, Bessent assumed the Federal Reserve would make his job easier by cutting interest rates. After all, at the end of last year, central bank policymakers had endorsed four rate reductions for 2025. But since then, things have changed. Inflation and economic uncertainty — especially surrounding the White House’s tariff policies — have led the Federal Open Market Committee to pause more easing until the outlook becomes clearer.

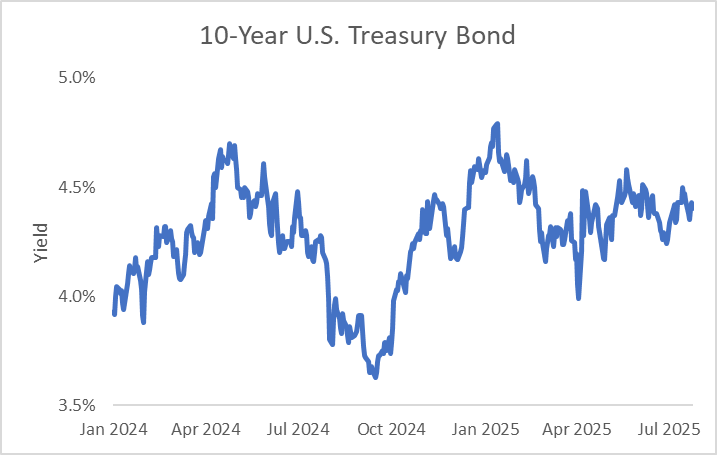

As a result, Bessent has shifted to broader efforts to manage long-term financing costs without direct monetary intervention. He’s leaned on fiscal levers like deregulation and energy price stabilization to massage yields lower. And as the next chart shows, he’s seen some success. After starting the year near 4.8%, and briefly dipping below 4%, the 10-year yield has settled around 4.4%...

Yet, as I’ve stated previously, the stakes remain high. With roughly half of the $28 trillion in publicly held U.S. government debt maturing over the next three years — and an average coupon of just 3.3% — refinancing at current rates could add as much as $300 billion to the deficit, according to Wells Fargo. Without help from the Fed, that task could prove daunting.

Later this week, Bessent has a chance to further the cause. On Wednesday, the Treasury will release its Quarterly Refunding Announcement (“QRA”). If it sticks with the current strategy of leaning into short-term issuance, that could support demand for longer-dated Treasurys. Any resulting drop in yields may serve as another tailwind for the S&P 500 Index

But don’t take my word for it, let’s look at what the data’s telling us…

Each quarter, the Treasury outlines what it plans to borrow to meet the government’s financial commitments. It also provides a breakdown of the maturity mix and updated funding projections. Together, these details give investors insight into how high spending may go — and for how long.

Yesterday, the Treasury revised its third-quarter net borrowing estimate from $547 billion (April projection) to $1.01 trillion. The increase stems from a lower-than-expected starting cash balance and projected weaker net cash flows. However, Treasury stated that excluding the lower starting balance, the updated borrowing estimate is $60 billion less than forecast in April.

Still, the real catalyst arrives tomorrow morning when we learn more detail about the mix of debt maturities the Treasury will employ.

When Bessent first assumed his role, Wall Street expected a shift toward longer-term borrowing. Momentum investors shorted Treasuries at the start of 2025, anticipating higher yields on longer-dated paper. But when the new Treasury Secretary stuck to short-term issuance, yields began to ease.

Today, with yields holding steady, market participants expect the Treasury to continue favoring short-term debt. The rationale: by issuing shorter-duration securities, the Treasury can contain long-term borrowing costs — and potentially pivot to longer-term issuance after the Fed has lowered rates. For many institutional investors, that outlook could be bullish for stocks.

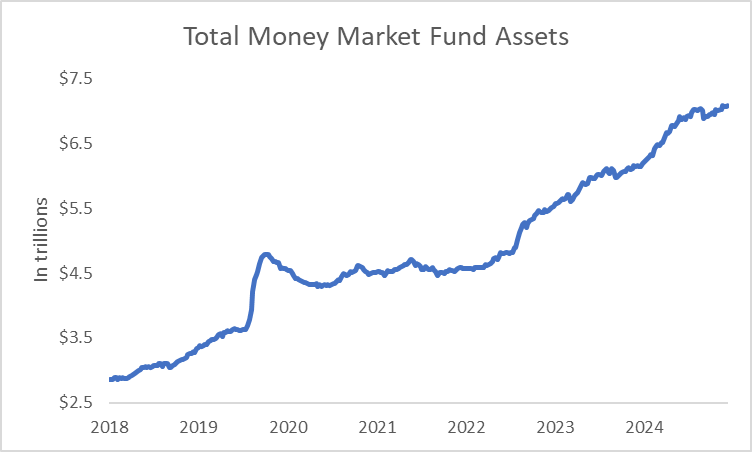

Meanwhile, money market funds are sitting on record levels of cash…

As of now, $7.1 trillion is parked in money market assets — nearly double the $3.6 trillion seen before the pandemic. These funds typically invest in highly liquid, short-term instruments and are locking in attractive yields: the 2-year note pays 3.9%, and 3-month Treasury bills offer 4.3%. With Wall Street expecting four Fed rate cuts over the next year, now may be a prime opportunity to secure current yields on shorter-duration debt.

This surge in money market assets presents an advantage for the Treasury. It can issue additional short-term debt without significantly raising yields due to quick maturities and strong demand. Conversely, limiting long-term issuance could tighten supply, pushing asset managers to bid up prices on existing 10-year notes — and thereby nudging yields lower.

As I mentioned earlier, every basis point Bessent can shave off borrowing costs now helps reduce future interest obligations. If it sparks a growth rebound — driven by lower financing costs for households and businesses — so much the better. Higher growth could mean more tax revenue without increased outlays.

So, if Wednesday’s QRA confirms expectations, it could pave the way for easing 10-year yields and a steady rally in the S&P 500.

Five Stories Moving the Market:

Top U.S. and Chinese economic officials met in Stockholm for more than five hours of talks aimed at resolving longstanding economic disputes at the center of a trade war between the world's top two economies, seeking to extend a truce by three months – Reuters. (Why you should care – these talks and a trade deadline extension are expected to facilitate a meeting between President Donald Trump and China’s President Xi Jinping this fall)

Taiwan's President Lai Ching-te is set to delay a diplomatically sensitive trip his team had floated to the Trump administration for August that would have included stops in the United States – Reuters. (Why you should care – delaying the visit, which is sure to upset Beijing, is a signal the White House is focused on trade talks with China)

Prime Minister Mark Carney said his government is still deep in trade talks with the Trump administration, despite recent comments from the US president that suggested a deal with Canada wasn’t a priority – Bloomberg. (Why you should care – Carney said discussions are in the “intense” phase, and negotiators will spend all week in Washington, D.C.)

Celestica raised its full-year revenue forecast for the third time in a row as demand grows for its cloud-computing segment; the manufacturer of components such as microchips for artificial intelligence hardware, now expects its revenue to reach nearly $11.6 billion in 2025 compared to guidance for $10.4 billion in the fall – Bloomberg. (Why you should care – AI demand is boosting business and margins)

Business leaders on both sides of the Atlantic breathed a sigh of relief that the U.S. and European Union had averted a bruising trade war with their agreement on tariffs and investment; now attention is shifting to assessing the deal’s winners and losers – WSJ. (Why you should care – European industry leaders said this is likely a best-case scenario for European companies because it avoids a bigger fight and removes uncertainty for the road ahead)

Economic Calendar:

Earnings: AMT, GLW, JCI, PYPL, SBUX, STX, TER, UNH, UPS, V

U.K. – BOE Consumer Credit for June (4:30 a.m.)

U.S. – Goods Trade Balance for June (8:30 a.m.)

U.S. – Retail, Wholesale Inventories (Preliminary) for June (8:30 a.m.)

U.S. – FHFA House Price Index for May (9 a.m.)

U.S. – S&P CoreLogic Case-Shiller Home Price Index for May (9 a.m.)

U.S. - JOLTS Job Openings for June (10 a.m.)

Treasury Auctions $80 Billion in 6-Week Bills (11:30 a.m.)

Treasury Auctions $30 Billion in 2-Yaer Floating Rate Notes (11:30 a.m.)

Treasury Auctions $44 Billion in 7-Year Notes (1 p.m.)

U.S. - American Petroleum Institute Crude Oil Inventory Data (4:30 p.m.)