Employment Metrics Point to Easing Growth and Fed Rate Cuts

The supply of labor compared to demand is steadily moving back into balance…

This morning, there were two key pieces of employment data released… the U.S. Bureau of Labor Statistics’ (“BLS”) Job Openings and Labor Turnover Survey (“JOLTS”) and Automatic Data Processing’s National Employment Report for February.

Each of the data point to a labor market that continues to gradually loosen. In other words, the pace of hiring continues to slow while the number of job openings is on the decline. Both of these metrics are moving back toward pre-pandemic levels of activity. That’s something our central bank has sought as a guide for when to consider cutting interest rates once more.

But let’s take a look at the data…

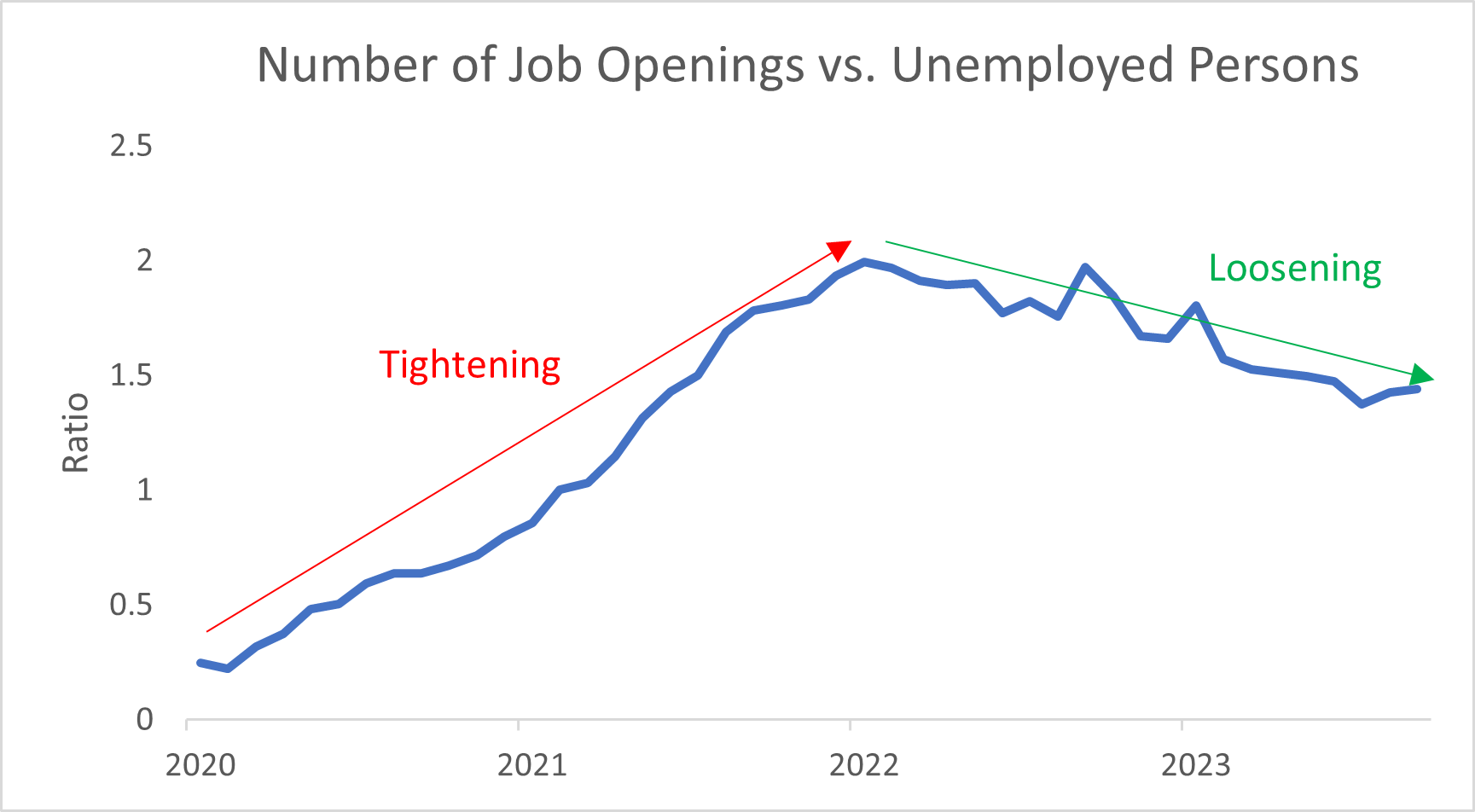

According to the BLS, the number of job openings held steady in January at 8.9 million compared to the downwardly revised number for December. That means the ratio of available jobs compared to unemployed persons is unchanged at 1.4...

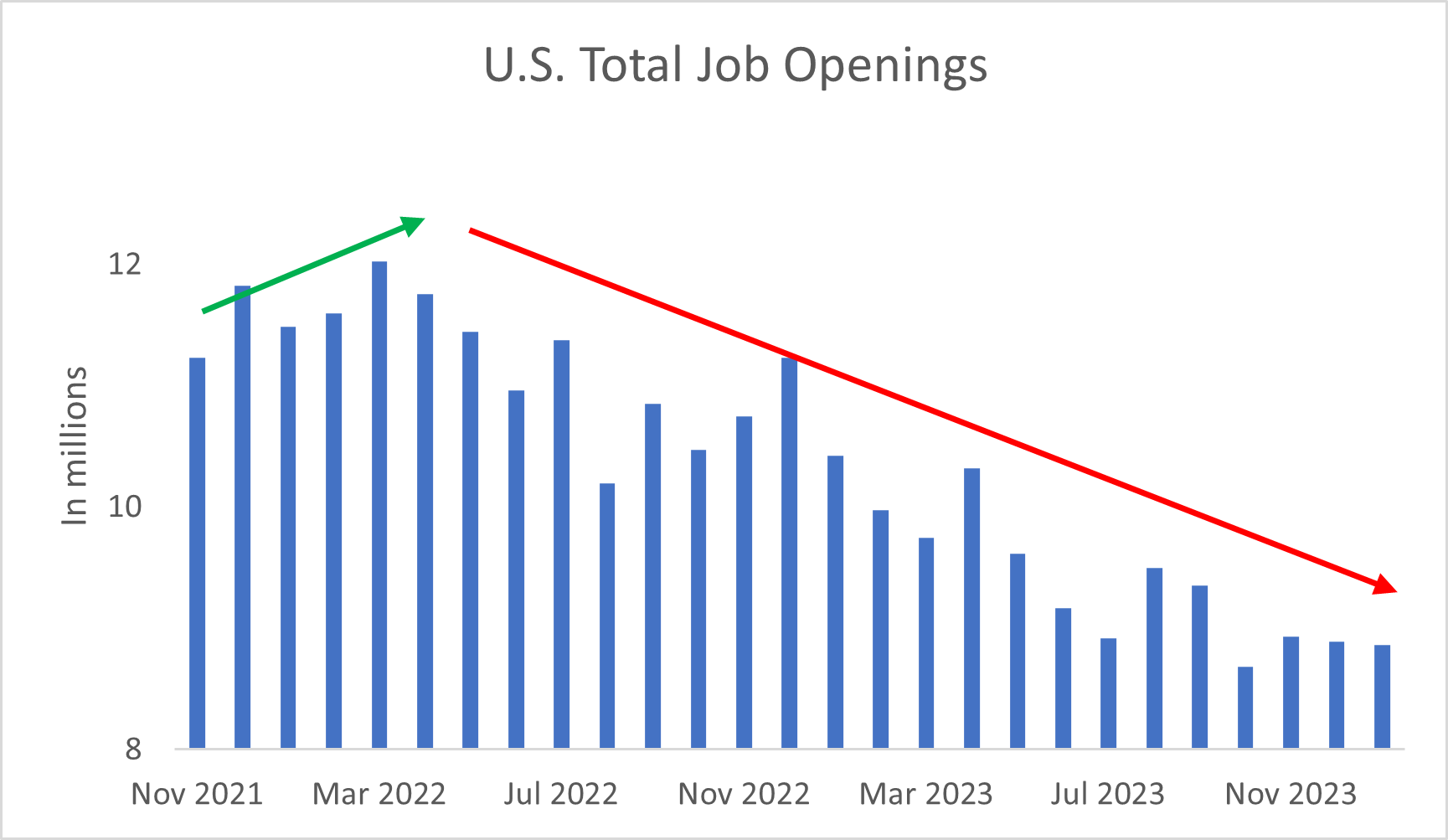

Now, the ratio isn’t quite back to the pre-pandemic level sub-1, but it’s well below the peak of 2 set in March 2022. In addition, the estimated number of available positions is well below the April 2022 peak of 12 million and headed back toward the pre-pandemic level of around 6.8 million…

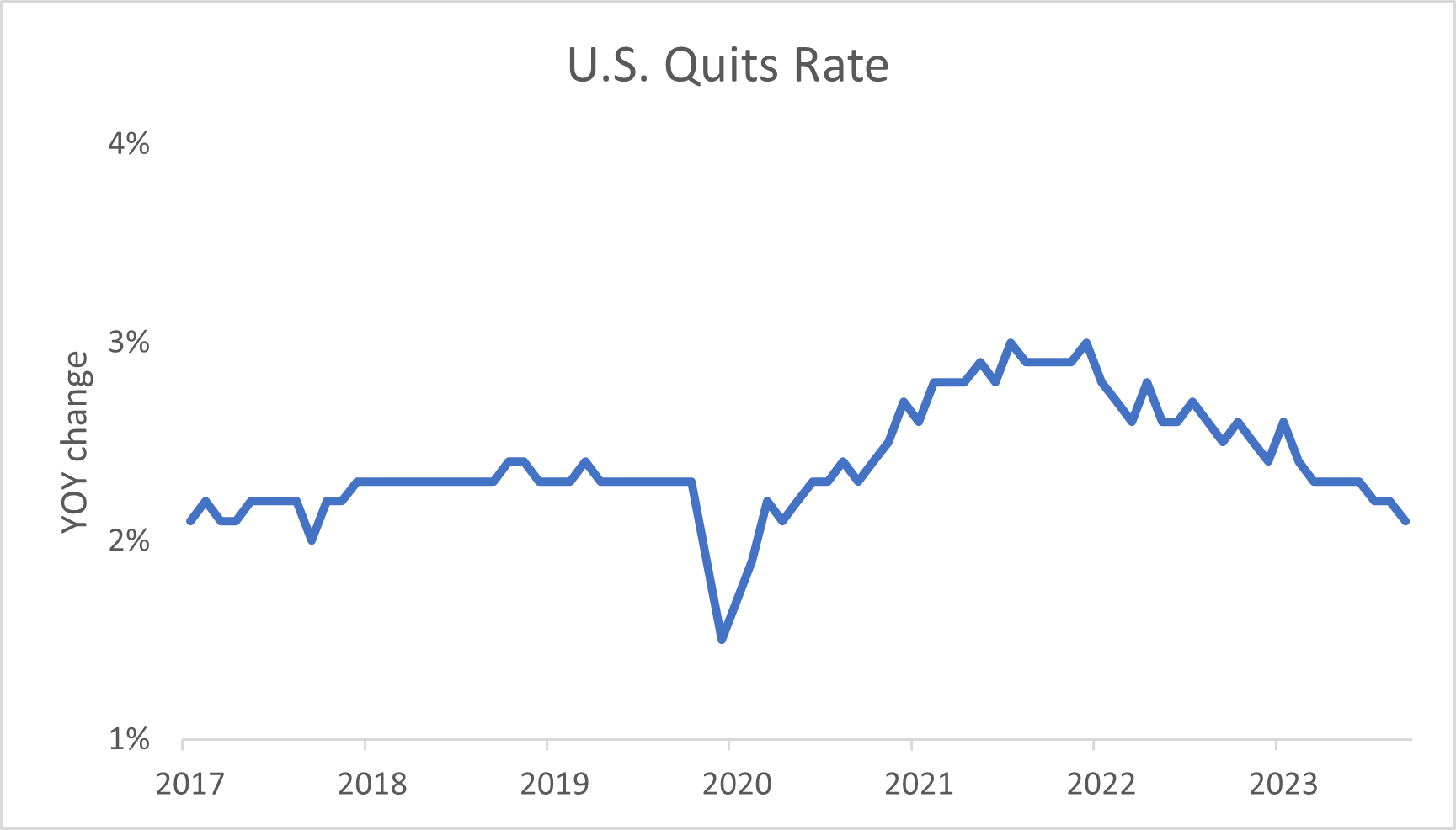

And the quits rate keeps dropping. In January it hit 2.1% compared to 2.2% in December. This marked the lowest level since labor demand exploded higher in mid-2021. The decline suggests employees are finding fewer attractive opportunities elsewhere...

The BLS also released revisions of its prior JOLTS estimates as part of this morning’s numbers. The total for 2023 was reduced by 438,000 jobs while the 2022 number was cut by 1.1 million. In other words, the labor market isn’t as tight as previously reported.

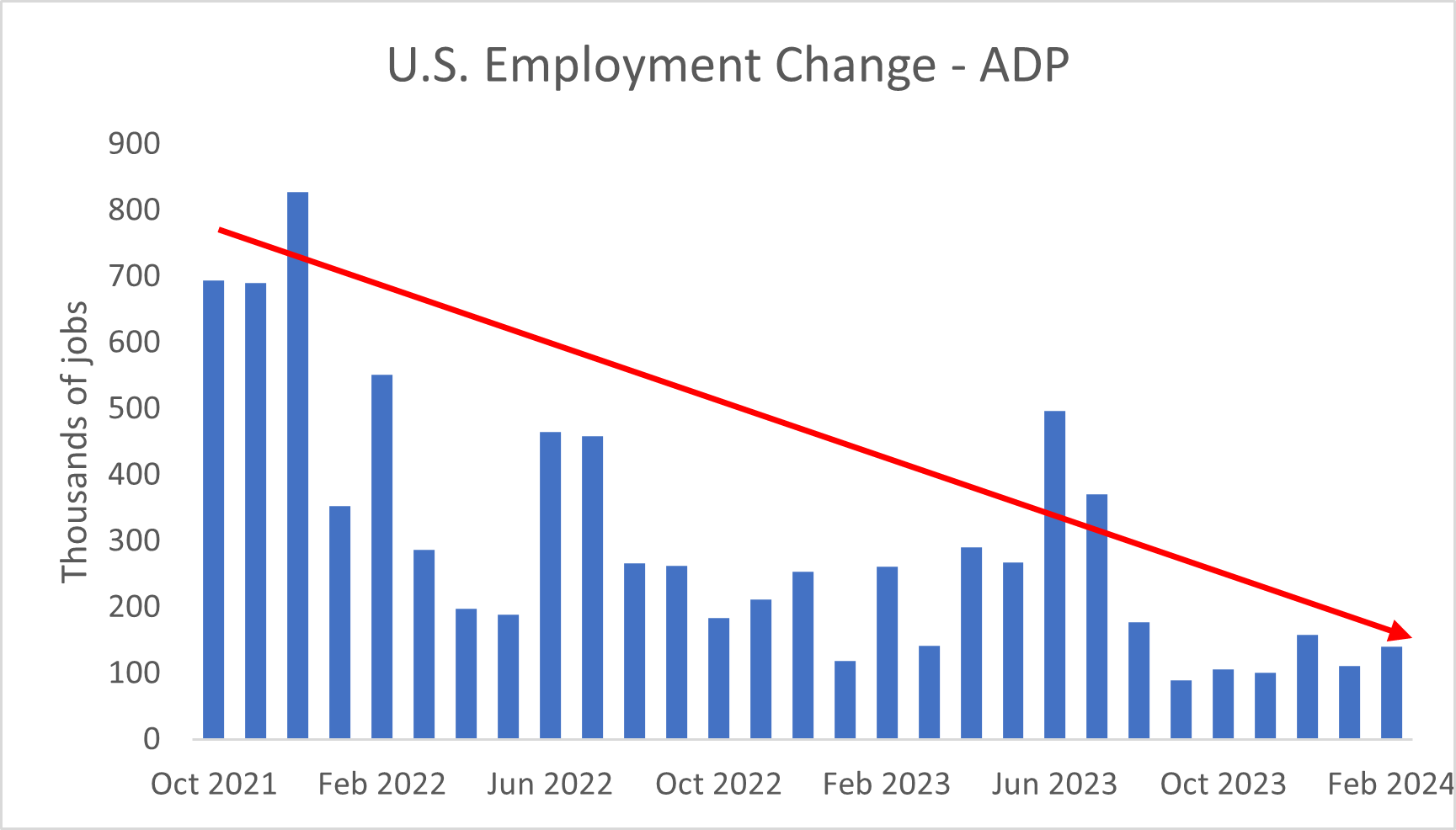

This would keep with the February employment data from ADP. According to the payroll-processing firm, companies added 140,000 new workers last month compared to 111,000 in January and the one-year average of 204,000...

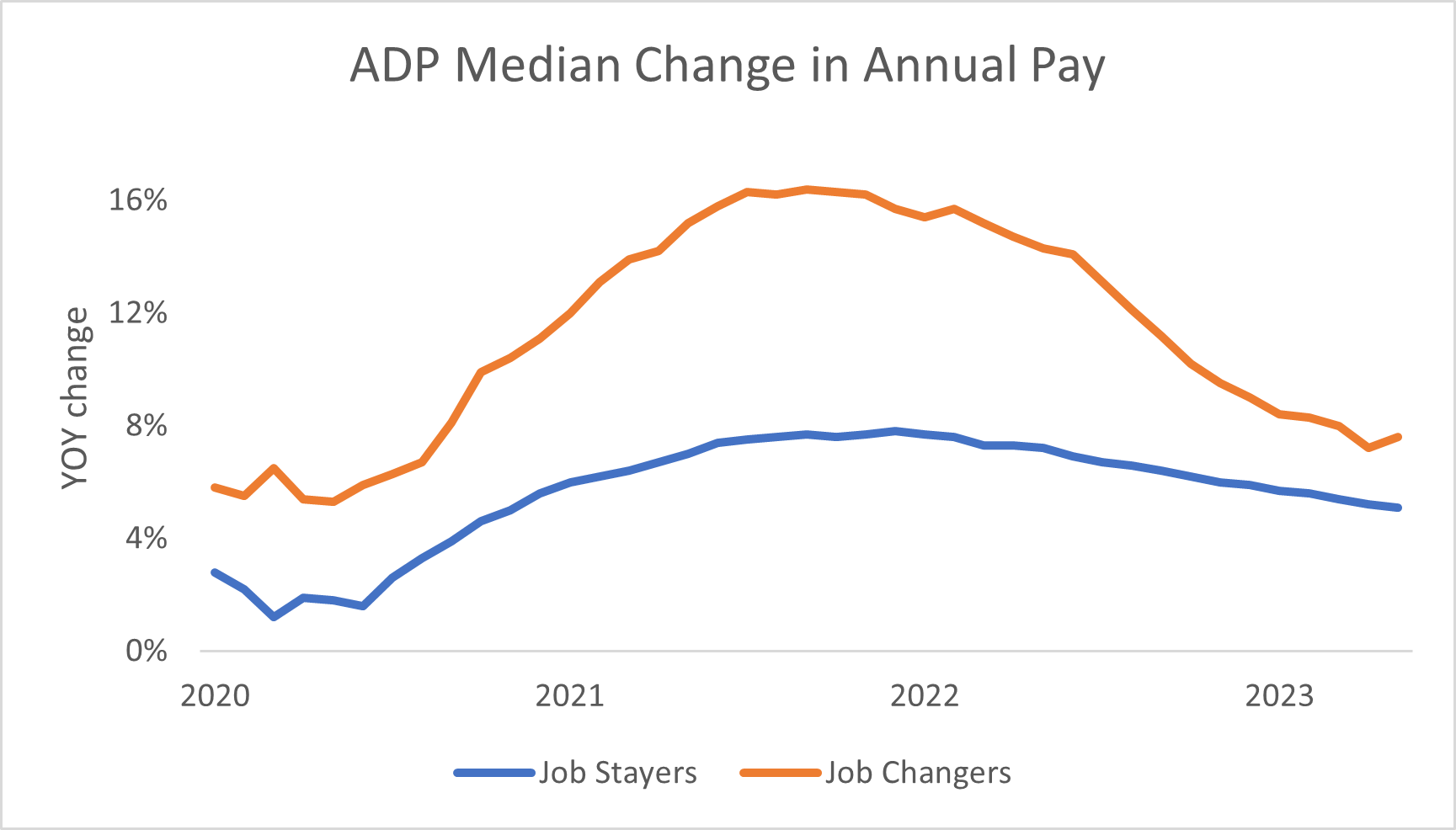

At the same time, pay increases continue to ease. According to ADP, job stayers saw a 5.1% jump while job changers experienced a 7.6% bump in compensation. Both numbers are well below their respective 7.8% and 16.4% peaks set in 2022...

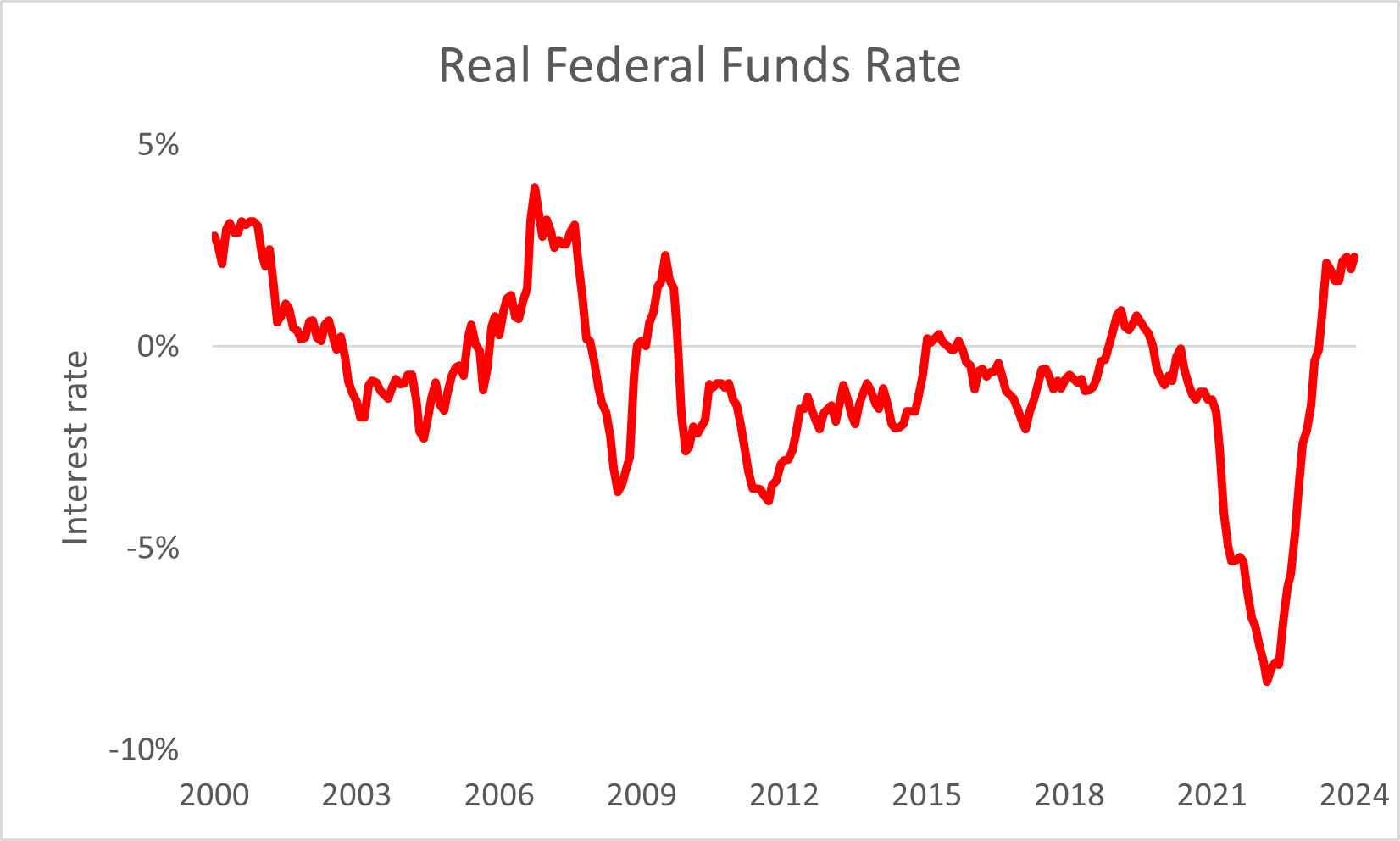

The data point to economic and inflation growth that continues to cool. The change would support the Federal Reserve cutting interest rates later this year. Based on the real rate of interest (fed funds minus inflation), the central bank should have plenty of room...

So, like I said at the start, economic momentum is slowing. High interest rates are forcing households to spend more on needs and less on wants, weighing on goods demand. We can see it in items like the 0.8% contraction in January retail sales and hearing it from retailers like Walmart and Target.

And as the data keep cooling, it will lead to central bank rate cuts. The shift will allow households and businesses to refinance debt and borrow once more. And while the economic dynamics may mean near-term pain, the Fed’s forthcoming adjustments should lead to the next economic boom and a steady rally in the S&P 500 Index.