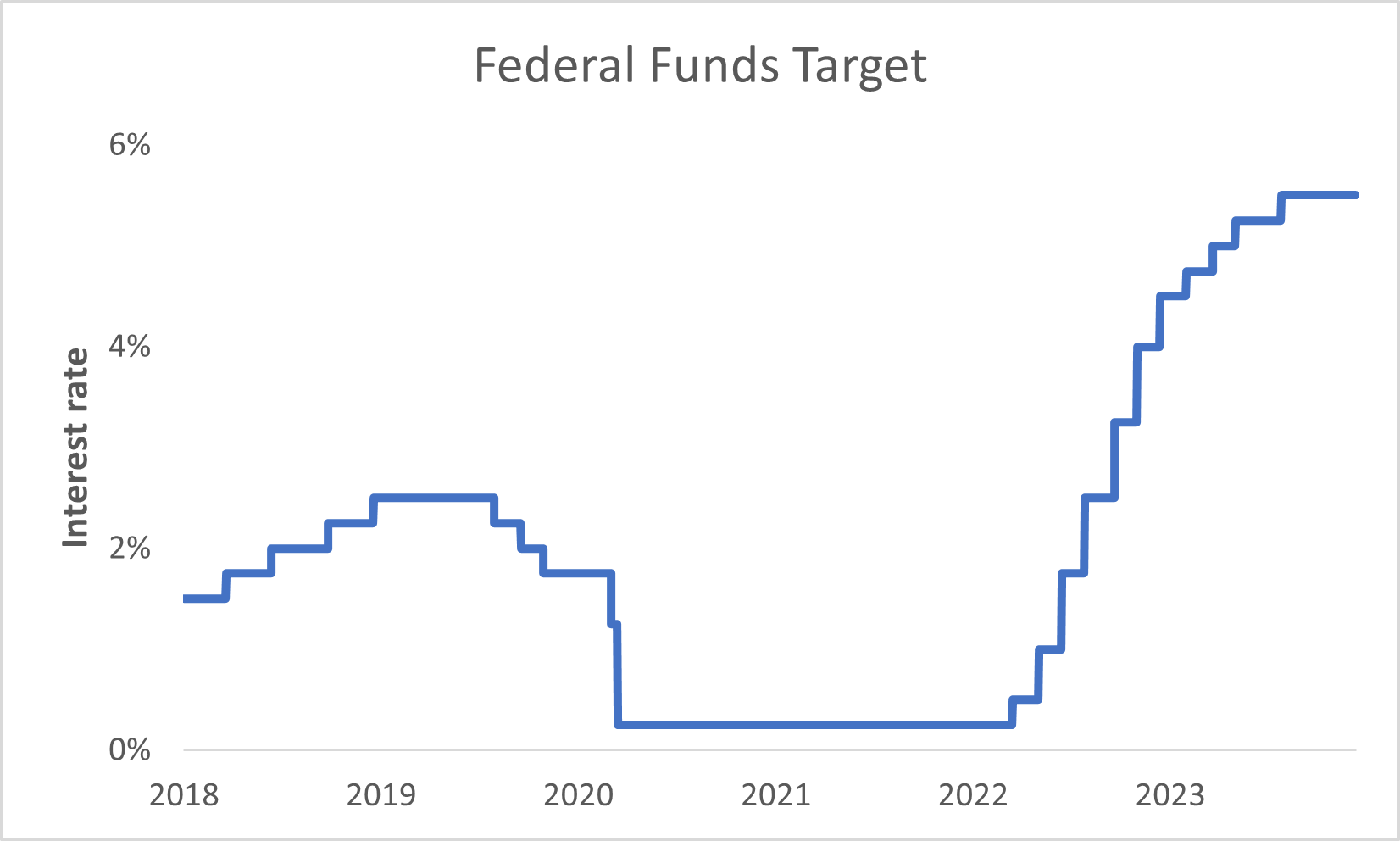

After a torrid series of rate hikes over the last 20 months, the Federal Reserve has finally restocked its tool kit to fight the next economic downturn…

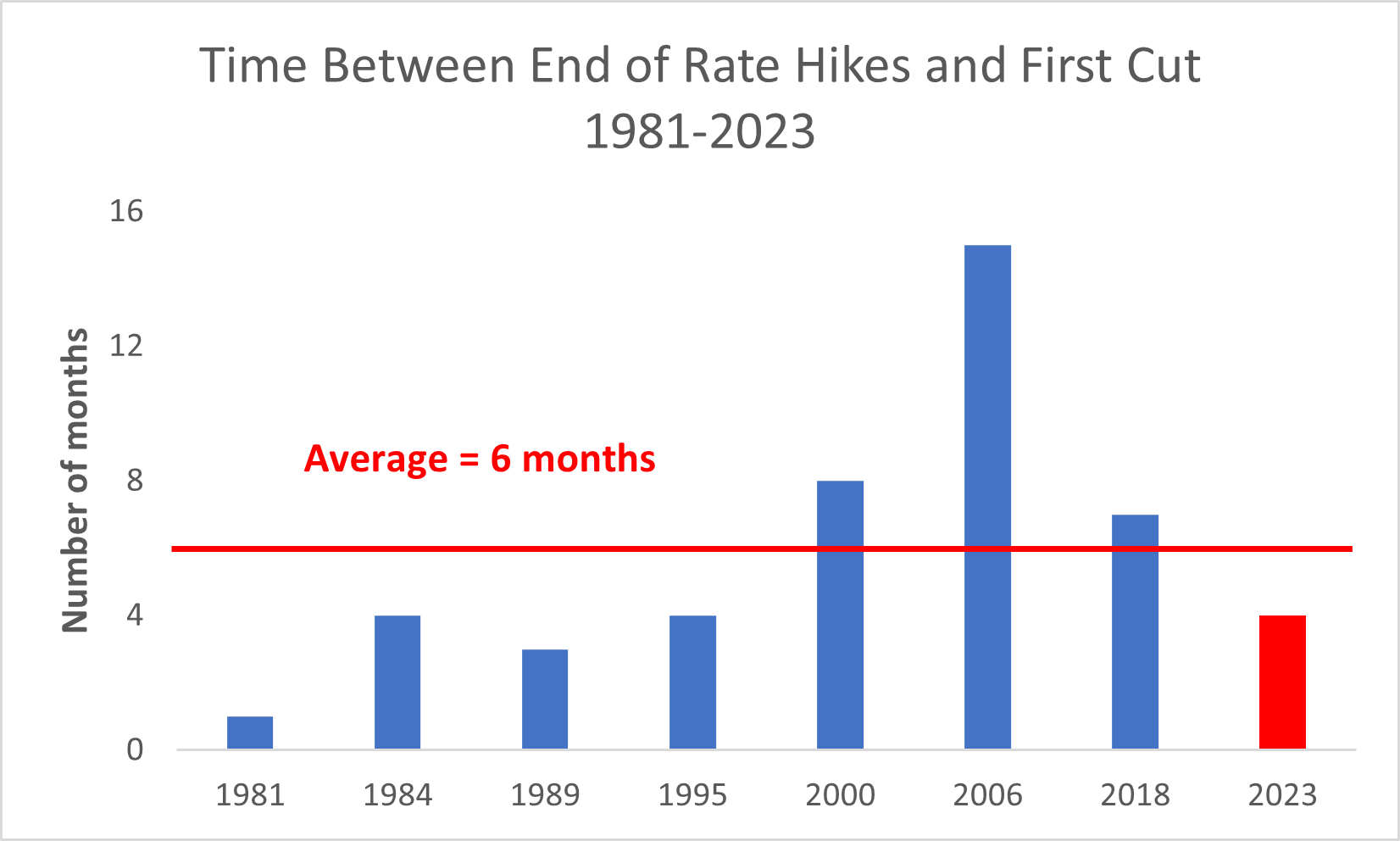

In fact, the Fed has held rates steady since July. The last time it left rates unchanged for this long was a seven-month stretch in 2019, prior to cuts. Since 1981, the average stretch without a decline has been six months…

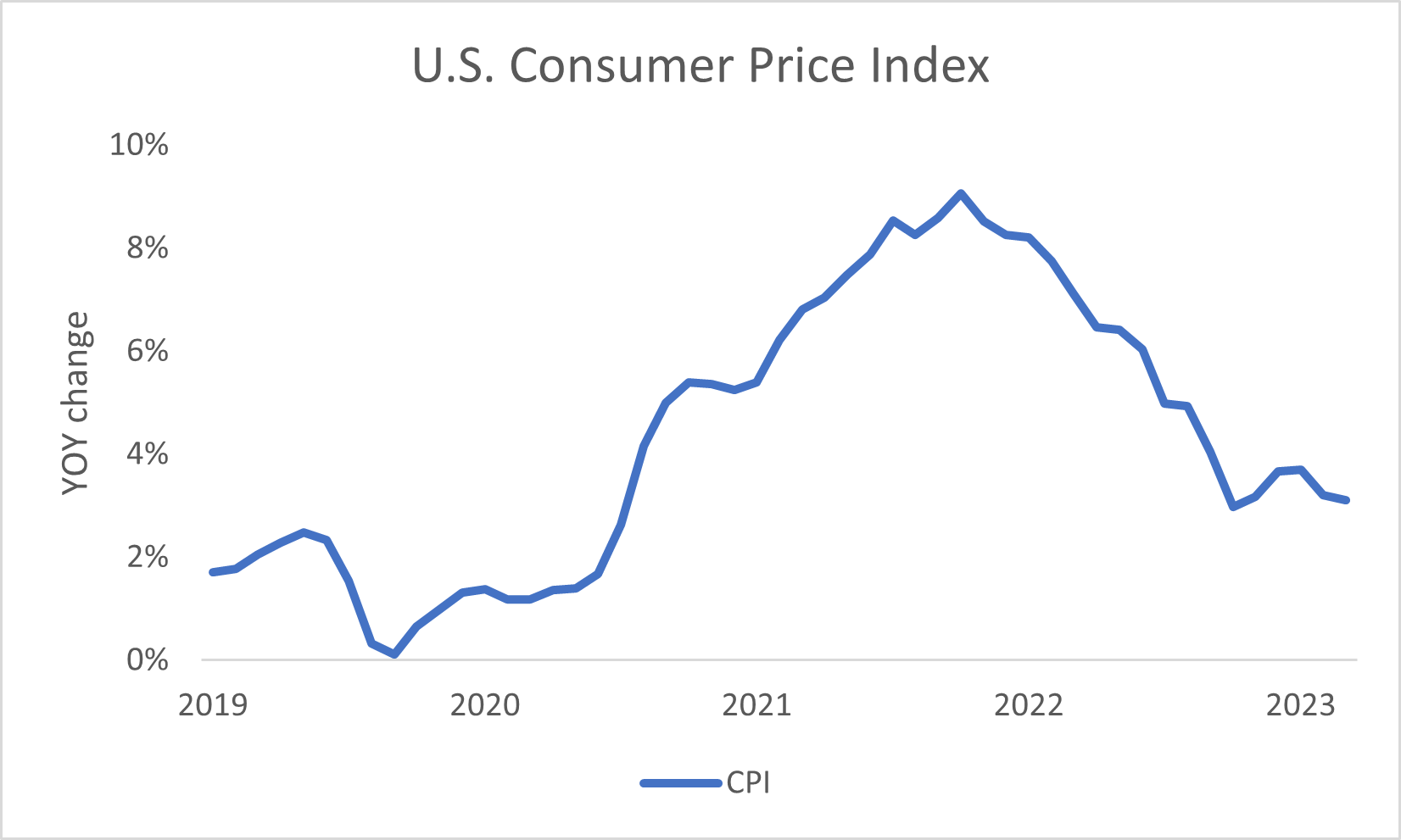

But yesterday’s release of CPI data told us the central bank now has plenty of room to lower rates once more…

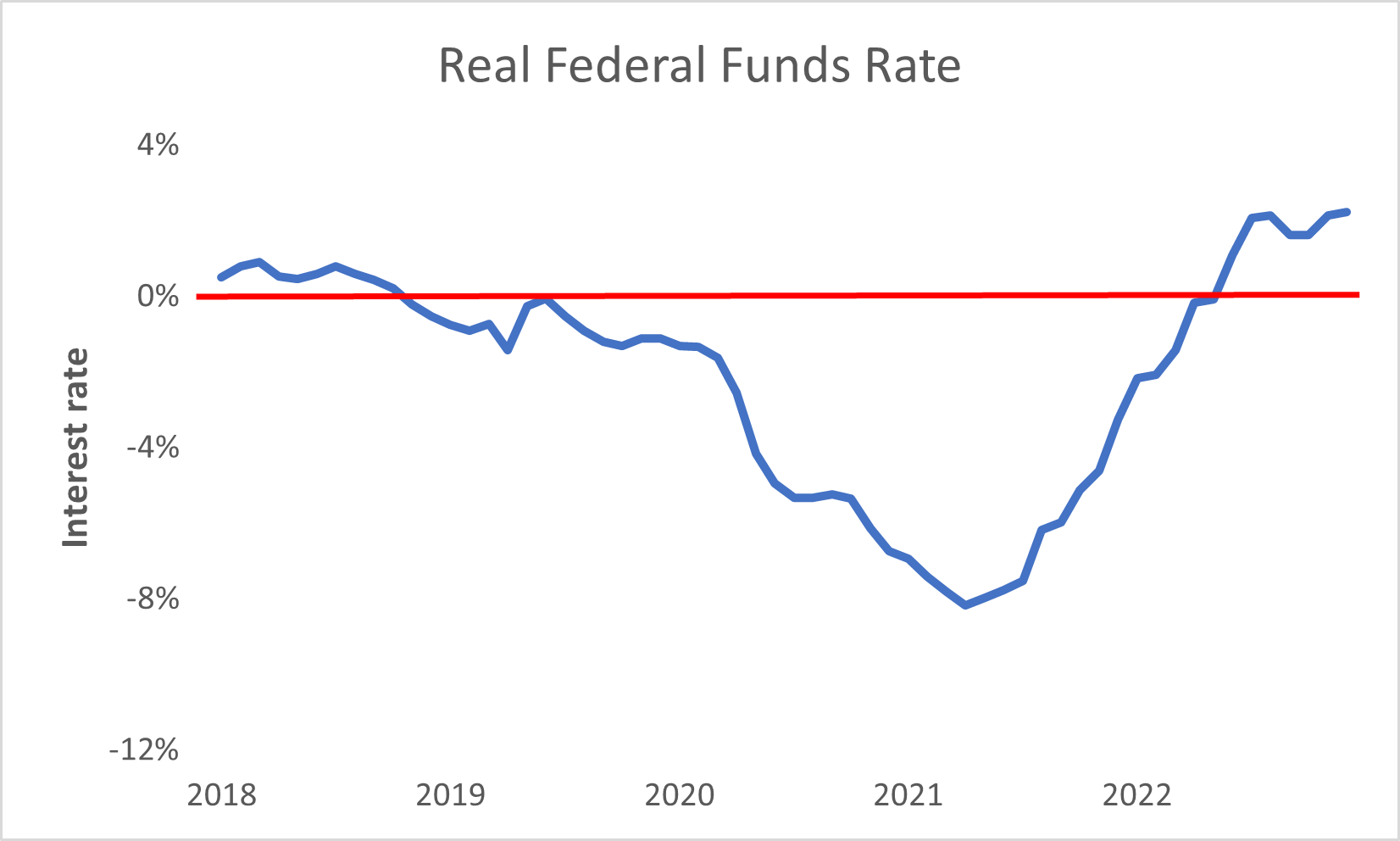

We can see this by looking at the real federal funds rate (effective fed funds minus CPI). With the release of November data, the real fed funds rate is at 2.2% compared to -8.2% back in March 2022…

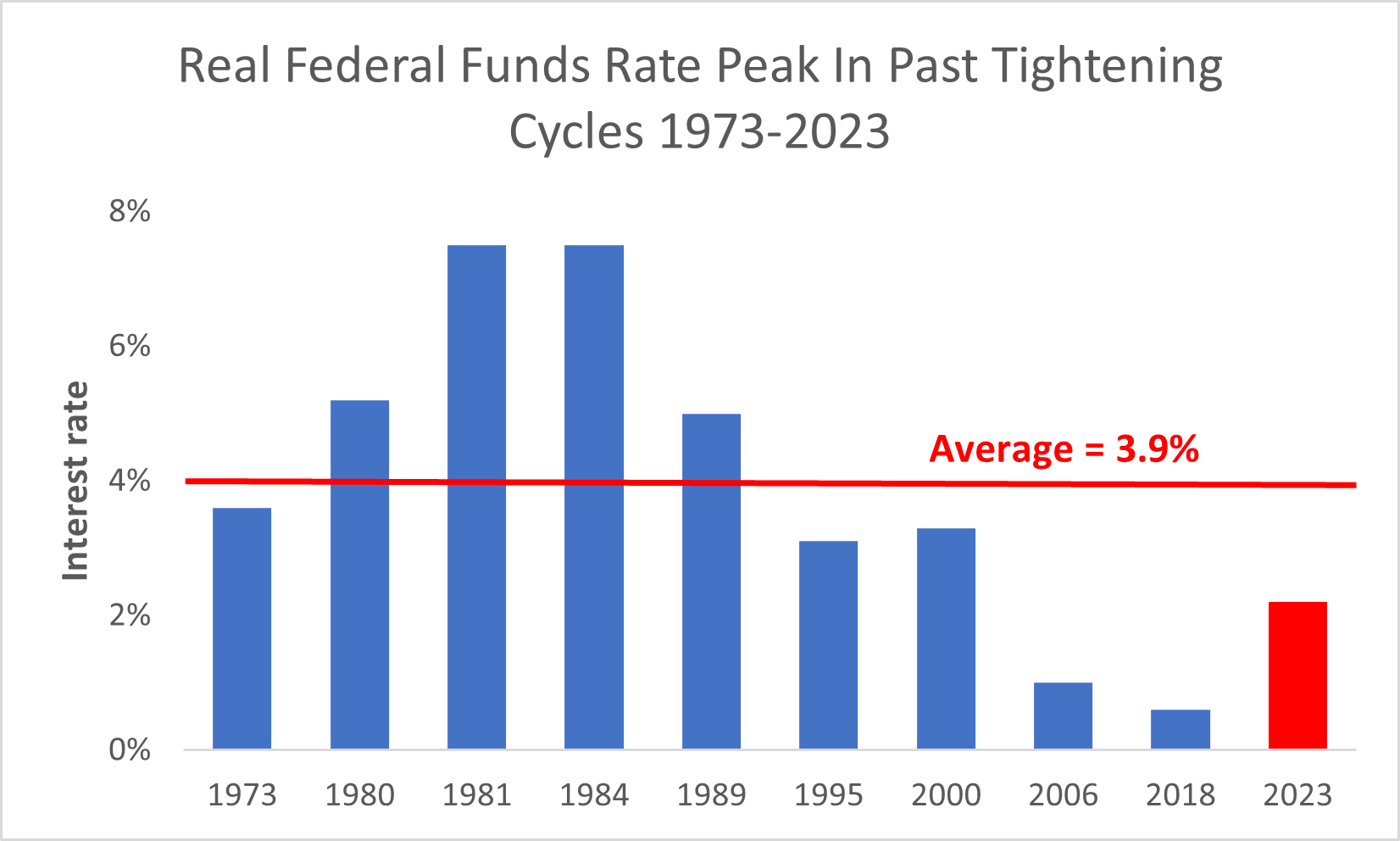

That’s important because every rate tightening cycle since 1973 has ended with positive real fed funds. The average has been 3.9%...

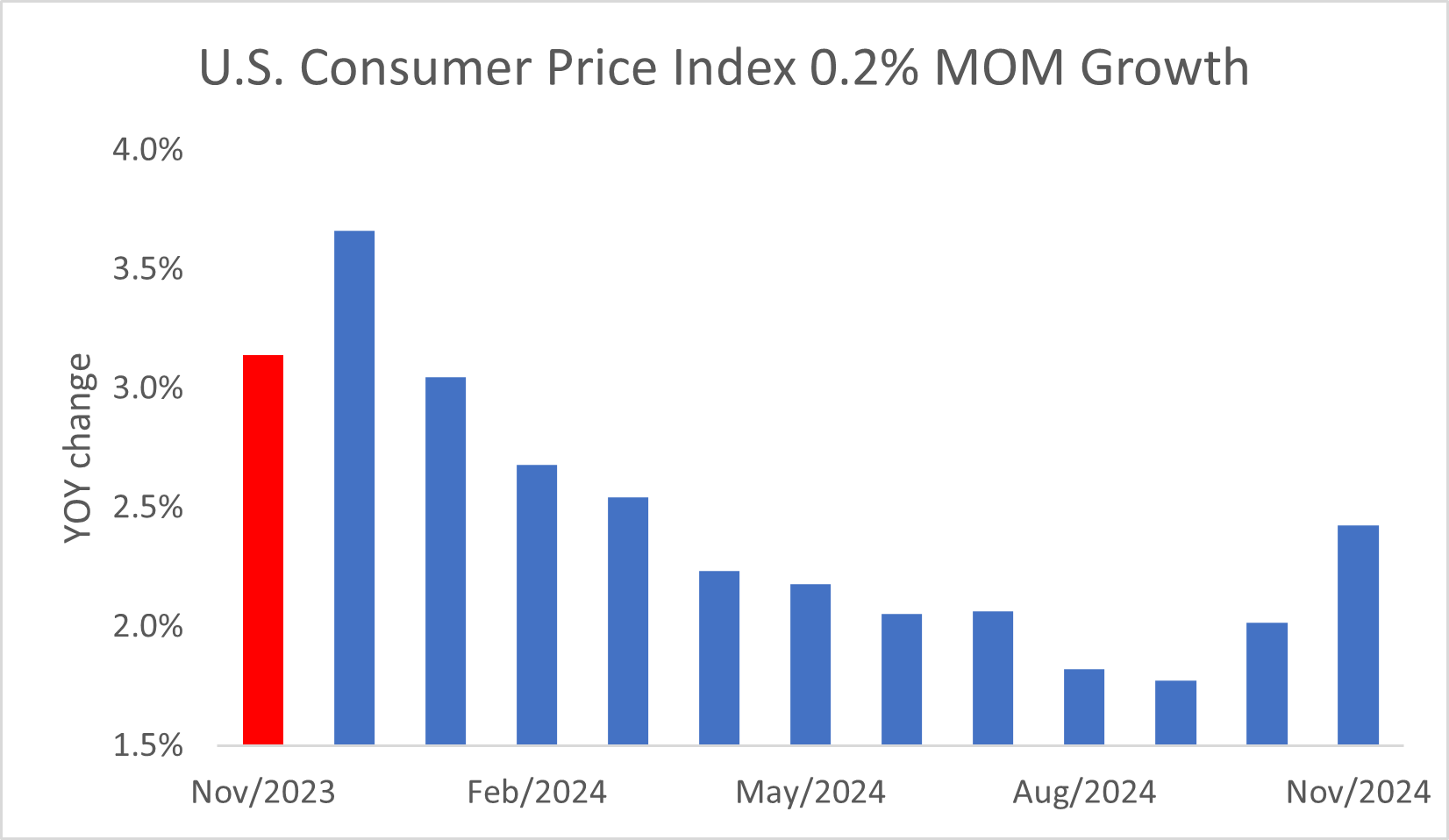

Over the last three months, as economic activity has slowed due to diminishing COVID savings, inflation has averaged less than 0.2% growth MoM. Based on that type of gain, CPI could be back below 2% by August 2024…

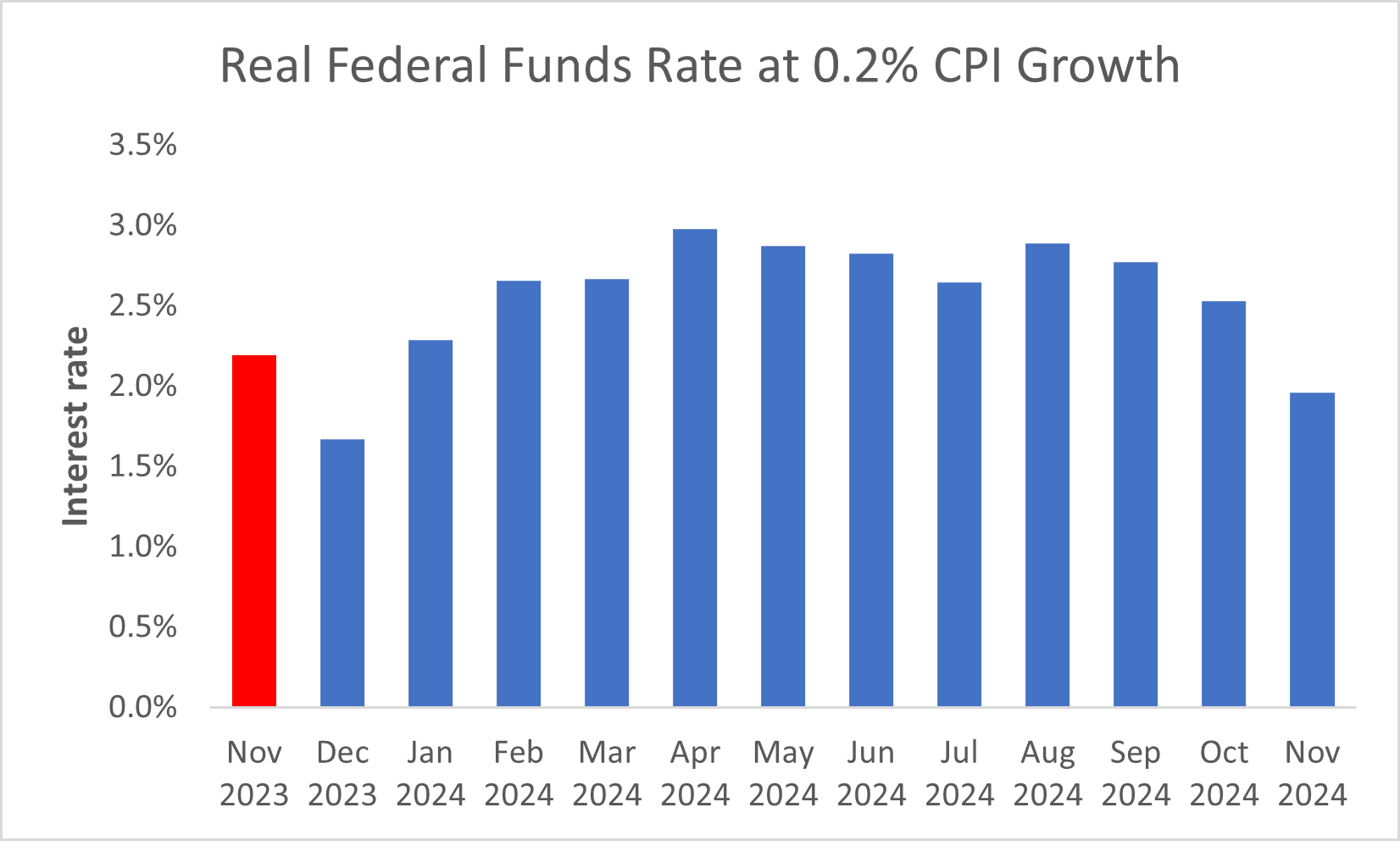

The change means the Fed will have even more room to ease. Based on current expectations for 100 bps of cuts over the next 12 months, real fed funds would still be at 2% next November...

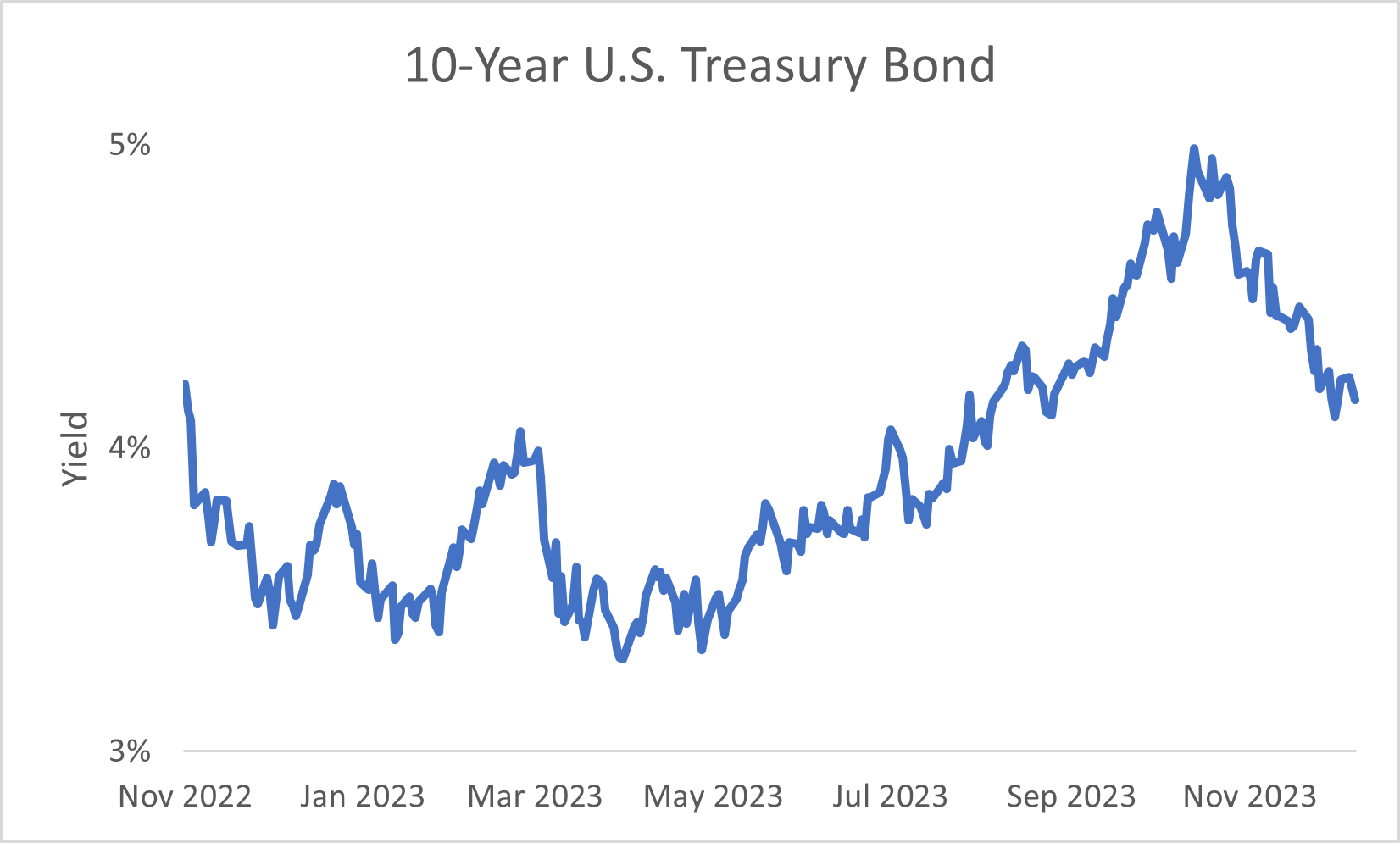

In other words, even then, interest rates would be weighing on inflation and the central bank would still have plenty of room to ease. That should continue to keep downside pressure on bond yields as investors try to lock in peak rates…

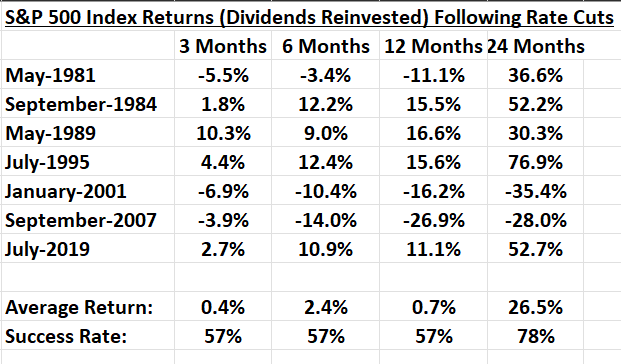

And while rate cuts may initially stoke economic concerns, they should act as a long-term tailwind for patient investors and the S&P 500 Index…