Have a Simple Game Plan to Ensure Investing Success

Have a Simple Game Plan to Ensure Investing Success

Don’t make this common investing mistake…

In 1995, I had just graduated from college. I was determined to make my mark in the financial world. But there was one small problem… I had to find a job. And, as I quickly found out, a lot of other people had the same idea.

So, after some trial and error, I landed my first job at a small brokerage firm in Richmond, VA, called Wheat First Butcher Singer. My plan was to use that as my launching pad to success. But to get my foot in the door, I took whatever job I could.

The opportunity came with a caveat… it didn’t pay very well. In fact, my starting pay was a $14,000 base salary plus time and a half for anything over 40 hours per week. Now, it may have been 30 years ago, but that wasn’t a lot of money at the time. So, I took advantage of every chance to work late and grow my paycheck.

The next step on my path to success was investing. But, when you’re practically broke, that’s hard to do. You see, given the lack of funds, I wanted to buy the right assets at the right time. So, I got wrapped up in the advice of the older, more experienced people I worked with. They told me to wait for a stock-market pullback.

And that’s when I made the mistake that I see many people make today… I didn’t have a game plan.

I was taking advice from individuals with more money who focused on single stocks. They were right to be observant of high and low price-to-earnings multiples. Meanwhile, I was seeking to play it safe and invest in an index fund… one that owned many different companies.

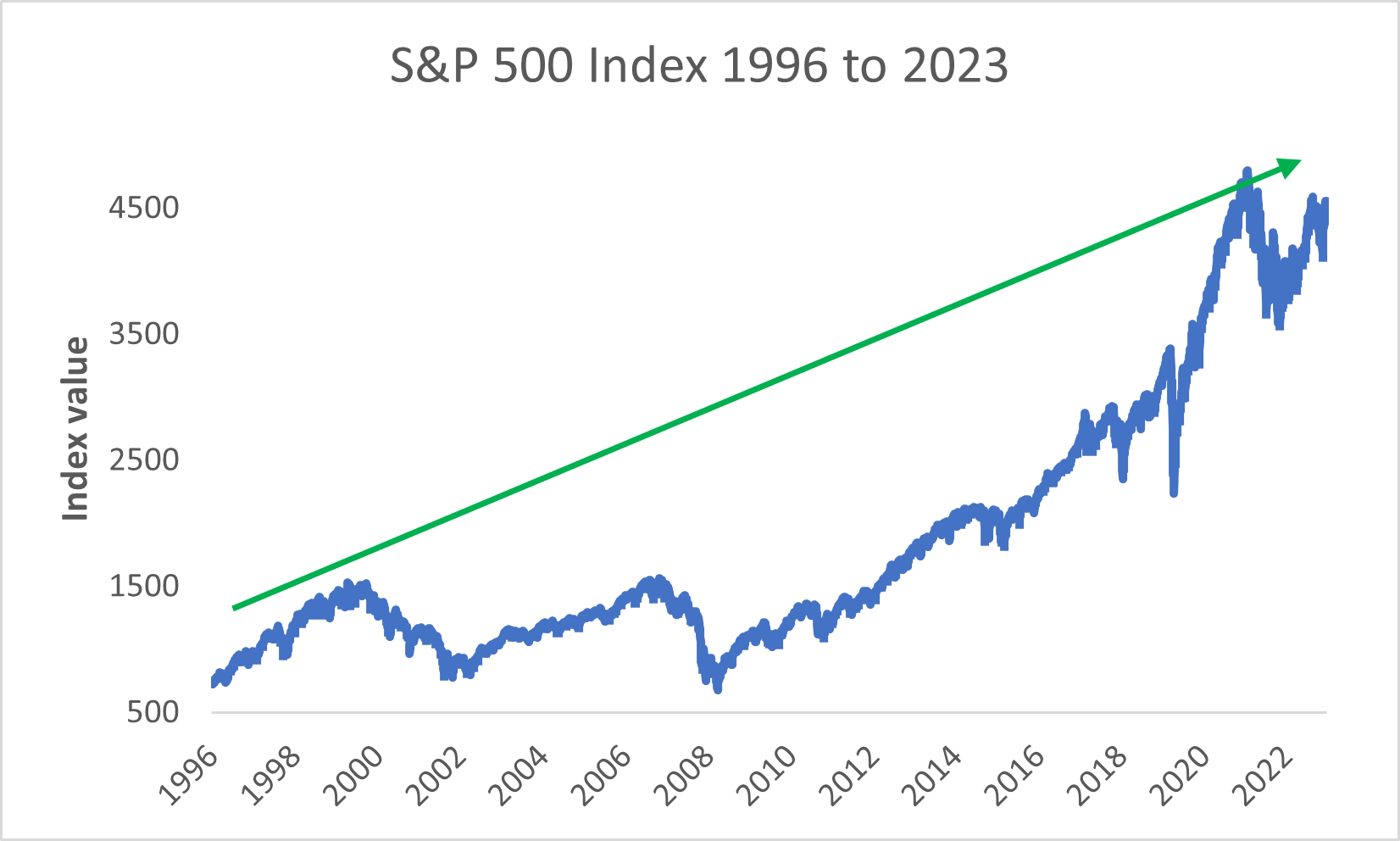

But, if I had a better strategy around what I wanted to accomplish, I would have started putting money to work in an S&P 500 Index fund. That cash would have compounded at a 9% annual rate for a gain of 908% today. Instead, I learned a lesson the hard way, that I hope can spare you, and especially beginning investors, the same agony.

But don’t take my word for it, let’s look at what the data tells us…

Like I said, the first part of the investing process is having a game plan. Identify how much money you can afford to spend and then determine what you’re willing to part with. A good rule of thumb is to never invest funds you can’t afford to lose.

Now, my objective was to not lose money. The problem was it held me back from my bigger, more important objective… making money. If I spent more time understanding my risk tolerance, the funds I had to work with, and what I wanted to purchase, I would have had a better strategy.

I would have realized that purchasing shares of an S&P 500 Index fund would have eased my risk concerns and started making me money. There are two main reasons why…

My first point is asset diversification. Like I said earlier, an index fund buys into many different businesses. That’s important because not every company in the index will do well at the same time. In addition, certain sectors will be in favor for various reasons while others are not. In other words, while many companies in the index may perform well, others will disappoint.

You see, if you own just one company’s shares, you’re tied to that business’s fortunes. If it’s doing well, you’ll probably be up huge. But, if sales are struggling, you’d better plan on taking your lumps. And, if that entity goes out of business, you’ll get wiped out.

That’s where asset diversification protects you. If you own the stock of companies across a broad array of sectors, you’re insulated from the swings up and down in a single stock. Because, while one’s falling, there’s likely another rising. Most times the gains and losses offset one another. So, you may not experience the huge upside of owning a single stock that does well, but unless every company in the index goes bankrupt at the same time, you won’t be wiped out either.

And that brings me to the second point… steady returns.

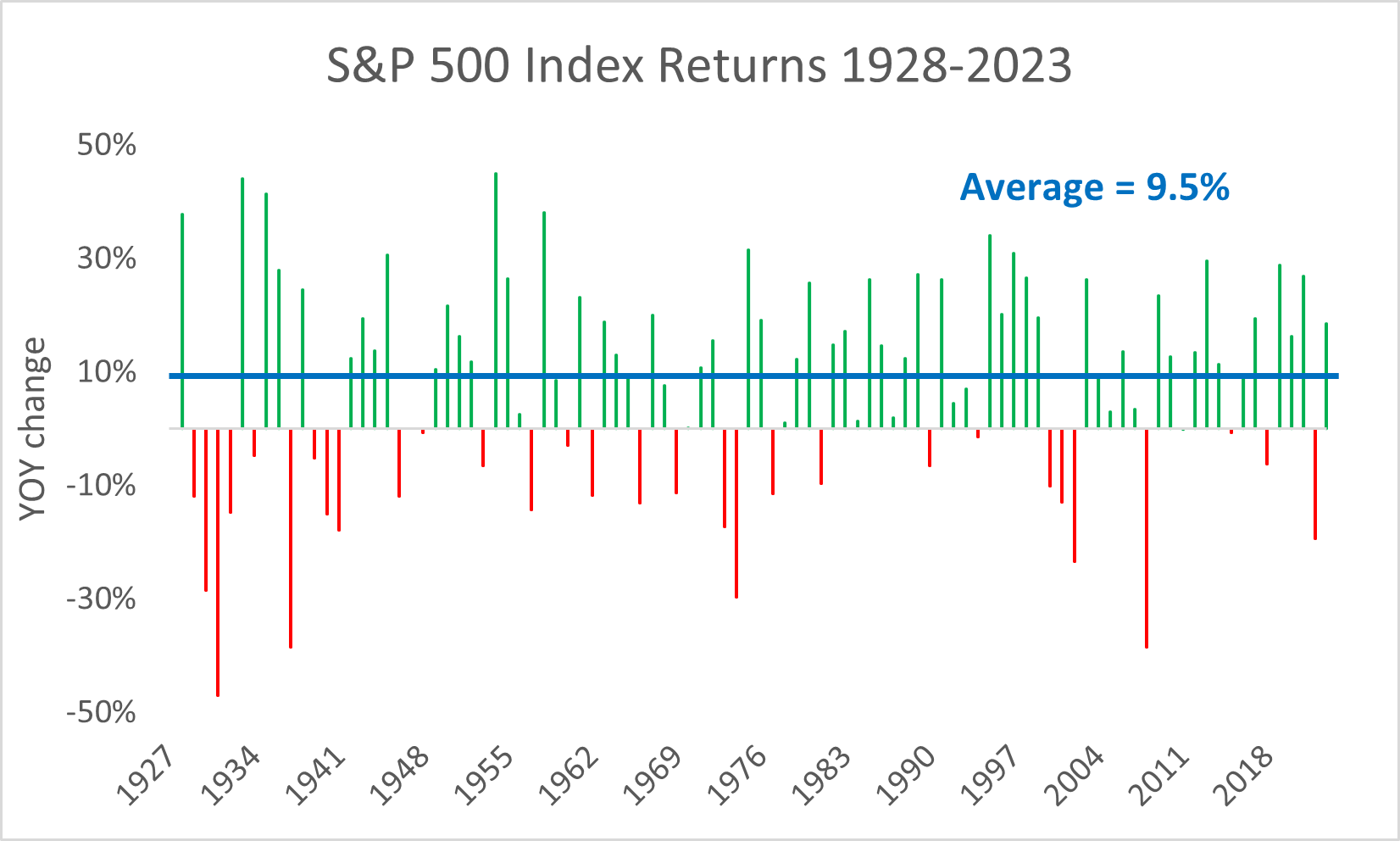

If we go back and look at the S&P 500’s performance over time, what stands out is the year in and year out gains…

The above chart shows the index’s absolute returns (dividends invested) for every year going back to 1928. What you’ll notice is that there are some very bad years in addition to some very good ones. The worst year was 1931’s 47% drop while the best was 1954’s 47% surge.

But you’ll also observe that over time, the gains add up more than the losses. And, for patient stock investors, they tend to average a 9.5% annual return. That number stands out because of the returns I failed to capture for not investing back in 1996. Like I stated, I could have earned 9% per year over the last 30 years. That’s on par with the index’s lifetime gains.

So, as I highlighted earlier, don’t make the same mistakes I did, and hold yourself back from making money. Come up with a game plan that you’re comfortable with and a strategy for sound investing. Start with something simple like an index fund. Consider buying shares of the SPDR S&P 500 ETF (SPY). It invests in the shares of the companies in the S&P 500 and pays dividends on a quarterly basis.

Instead of throwing everything you have into the investment all at once, spread it out. Maybe invest 25% or 50% up front and then ease into the balance monthly. That way you don’t have to worry about buying at the highs. And then, after you start seeing returns, and feel comfortable with the process, start looking into portfolio diversification and single stock ideas.

That way you can sleep soundly at night.