Inflation Math Points to 170 Basis Points of Easing Potential

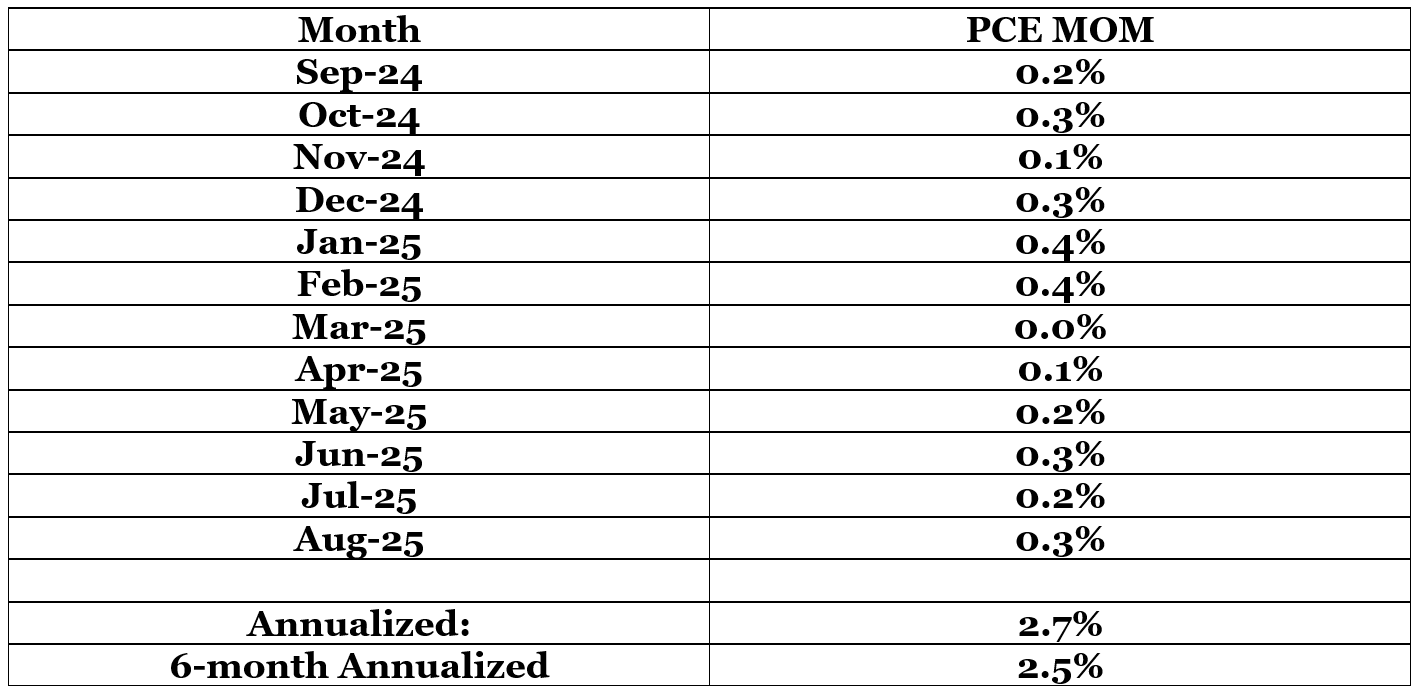

The Cleveland Fed anticipates 0.3% monthly PCE growth for August.

That would produce an annualized inflation rate of 2.7%.

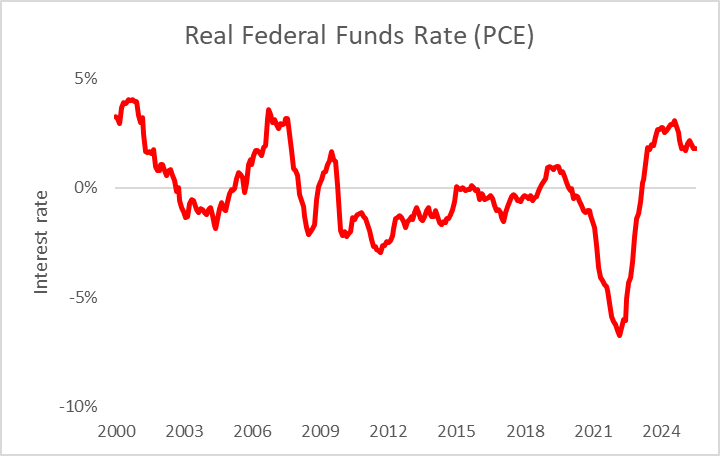

Such an outcome would imply a real interest rate (fed funds minus PCE) of 1.70%.

The end of this week brings the next key update on inflation. The U.S. Bureau of Economic Analysis (“BEA”) releases its August personal consumption expenditures (“PCE”) data. The latest numbers will likely show price pressures holding steady across key categories, allowing policymakers to continue cutting interest rates without fear of further stoking inflation growth.

Our central bank relies on this index when making monetary policy decisions. The Fed considers PCE a more comprehensive inflation gauge because it measures total spending on goods and services consumed by individuals, including purchases made on their behalf—such as health insurance. By contrast, the U.S. Bureau of Labor Statistics’ (“BLS”) consumer price index (“CPI”) focuses on out-of-pocket spending by urban consumers.

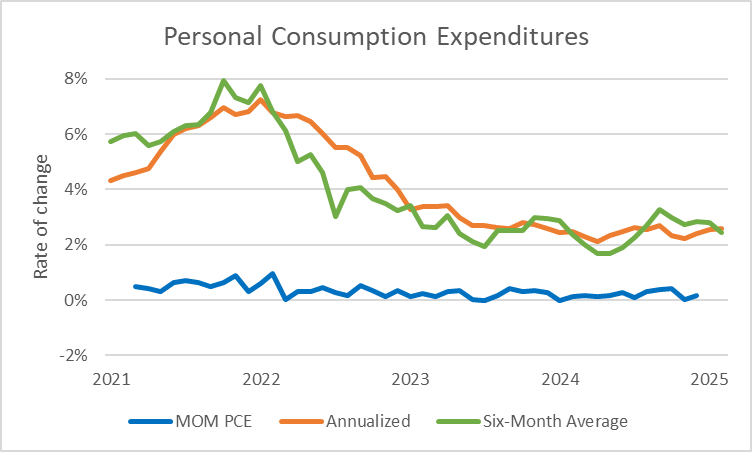

Consequently, the individual weights within PCE are less concentrated than those in CPI, making PCE less volatile. That stability reinforces the Fed’s preference. As shown in the following chart, while the pace of price increases is still above the 2% target, it has been steadily flattening out since peaking in mid-2022…

Growth in services prices increased, while the same measure for manufacturing eased, according to regional Federal Reserve bank business surveys. This trend should have a greater influence on PCE than it does on CPI. Based on the numbers I reviewed, the Fed’s preferred inflation gauge—like CPI a couple of weeks ago—saw little growth in August. That should support the case for easier monetary policy later this year. The shift will underpin a steady long-term rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

A couple of weeks ago, BLS released its consumer and producer price index data for August. Within those indexes, several readings offer insight into PCE trends. According to the data, items such as medical care services saw prices contract, shelter and insurance held steady, while energy, financial services, lodging away from home, and transportation rose.

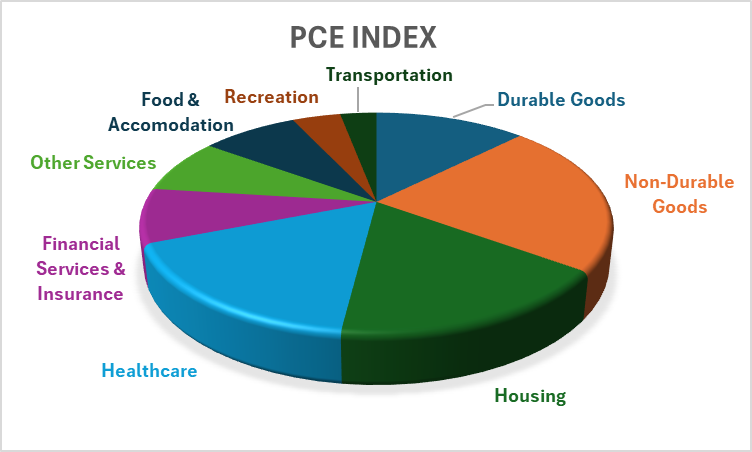

Housing and medical expenses each account for roughly 17% of the PCE index, while other categories have weightings ranging from 3% to 8%. I compared the BLS inputs to the relative PCE weightings, and the numbers suggest a slight rebound in the pace of growth in August compared to July.

Confirming this is the Inflation Nowcast from the Federal Reserve Bank of Cleveland. The Fed’s economic staff continuously updates its outlook based on the most recent data. According to their forecast, PCE growth in August was 0.3%, or 0.1% higher than in July.

Now, let’s examine what that means for the annualized growth rate…

The table above details the pace of monthly PCE growth over the past year. To estimate the annualized rate when the new numbers are released at the end of this week, I substituted last August’s 0.1% growth with this year’s forecast from the Cleveland Fed. When you add up the monthly totals, the annual rate rises slightly to 2.7%.

What’s even more interesting is what happens to the six-month annualized pace of growth. Much like last month, due to the calendar shift, we lose the “hot” 0.4% increase from February. In addition, PCE has been growing at a rate of around 0.2% per month for the last five months. So, if the Cleveland Fed’s prediction is right, that would mean the annualized six-month pace of growth should hold steady at 2.5% for a second straight month.

As Powell said last week, policymakers can’t disregard the potential inflationary impact of tariffs. But downside risks to the labor market are increasing. The Fed doesn’t want to see the job market collapse while waiting to determine whether the inflation fallout will be one-time in nature or long-lasting. So, if the central bank doesn’t see signs of inflation taking off, it’s inclined to ease rather than stay on hold.

Based on July’s data and the early indications for August, price growth isn’t heating up. When subtracting August’s 2.7% PCE forecast from the effective federal funds rate of 4.4%, it suggests 170 basis points of potential rate cuts.

If August’s PCE confirms the Cleveland Fed’s 0.3% forecast, it will support the case for rate normalization. With inflation steady and the labor market slowing, the Fed has room to keep easing. That should underpin steady upside in risk assets like stocks.

Five Stories Moving the Market:

Nvidia Corp. will invest as much as $100 billion in OpenAI to support new data centers and other artificial intelligence infrastructure, a blockbuster deal that underscores booming demand for AI tools like ChatGPT and the computing power needed to make them run – Bloomberg. (Why you should care – the agreement is likely to support steady demand and backlog for networking and semiconductor companies that support the buildout of AI infrastructure)

Changes in immigration, tax and regulatory policies are set to drive down underlying interest rates in the U.S., and make current monetary policy far too restrictive for what the economy needs to keep inflation at the Fed's 2% target, according to Federal Reserve Governor Stephen Miran – Reuters. (Why you should care – Miran’s statement signals he’s likely to favor a rate cut at the upcoming monetary policy meetings in October, December, and January, before his term expires)

Atlanta Fed President Raphael Bostic said inflation concerns would make him hesitant for now to declare support for cutting rates again in October, even though economic risks have shifted in recent months toward greater worries about employment – WSJ. (Why you should care – while Bostic’s comments may create some headline risk, Atlanta’s president isn’t a voter on the rate setting FOMC again until 2027)

Federal Reserve Bank of St. Louis President Alberto Musalem said he supported last week’s interest-rate reduction as a way to take out insurance against a weakening labor market, but sees limited room for more cuts amid elevated inflation – Bloomberg. (Why you should care – Musalem, who’s voting roll ends in December, sounds as if he is unlikely to support rate cuts at the next monetary policy meeting in October)

The Federal Reserve needs to be "very cautious" in removing restrictive monetary policy with inflation still above the central bank's 2% target and remaining persistent, according to Cleveland Fed President Beth Hammack – Reuters. (Why you should care – Hammack, who has hawkish tendencies, will be a voting member of the FOMC next year)

Economic Calendar:

Earnings - MU

Japanese Markets are Closed

Riksbank (Sweden) Monetary Policy Announcement (3:30 a.m.)

Eurozone – HCOB Eurozone Manufacturing, Services, Composite PMI for September (4 a.m.)

U.K. – S&P Global U.K. Manufacturing, Services, Composite PMI (Preliminary) for September (4:30 a.m.)

BOE’s Pill (Chief Economist) Speaks (5 a.m.)

U.S. – S&P Global U.S. Manufacturing, Services, Composite PMI (Preliminary) for September (9:45 a.m.)

Fed’s Bostic (Atlanta) Speaks (10 a.m.)

U.S. – Richmond Fed Manufacturing Index for September (10 a.m.)

Treasury Auctions $85 Billion in 6-Week Bills (11:30 a.m.)

Treasury Auctions $69 Billion in 2-Year Notes (1 p.m.)

BOC’s Macklem (Governor) Speaks (2:15 p.m.)

U.S. - American Petroleum Institute Crude Oil Inventory Data (4:30 p.m.)