Inflation's Slide Isn't Over

Don’t let the recent rally in bond yields scare you… inflation growth is headed even lower.

Last week, the stock and bond markets overcame two big hurdles. In its quarterly refunding announcement, the Treasury said it would borrow less money than previously predicted. And in its latest monetary policy announcement, our central bank said it was making good progress toward its goals to lower interest rates, but needed more time and data to be certain it could do so.

The two data points helped to drive the yield on 10-year U.S. Treasuries lower. They began the week around 4.2% and fell to 3.8% in a hurry.

Yet, at the end of the week, the latest employment figures from the U.S. Bureau of Labor Statistics showed job gains were much stronger than expected. The change ignited fears the Fed might hold off on rate cuts late this year as a result. Those worries were further stoked when Chairman Jerome Powell reiterated in a 60 Minutes interview that upcoming policy decisions will be data-dependent.

Bond yields have recovered most of their losses as a result. But skeptical investors, cautious on the potential for interest rate cuts, may be getting ahead of themselves.

The key driver of the rapid rate hikes between March 2022 and July 2023 was runaway inflation. So, the catalyst for the coming rate cuts will be cost growth that continues to cool. And based on what I’m seeing, next week’s consumer price index (“CPI”) data will show inflation keeps slowing. That should act as a long-term tailwind for the S&P 500 Index.

But don’t take my word for it, let’s look at what the data is telling us…

The first place I like to check for recent inflation trends is in the manufacturing surveys from regional Fed banks. Each month, the Dallas, Kansas City, New York, and Philadelphia Feds ask manufacturers in their districts about the state of activity. The questionnaires ask those companies about things like new orders, lead times, employment, and production. It inquires about whether costs are rising, falling, or unchanged.

But we must focus on “prices received for goods.” The number indicates what customers pay manufacturers for their finished product. It’s akin to CPI. So, the direction of prices received is an indicator of whether inflation is rising or falling.

Now, the states where those four banks are headquartered – Texas, Missouri, New York, and Pennsylvania – account for roughly 23% of domestic economic output. So, we can get a decent idea of national demand. But the results come out ahead of CPI, so it’s like having an early look into the data.

And the latest readings show prices received fell…

In the above chart, I combined the readings from the four central banks into a single gauge. It’s called the combined prices received index (CPRI) and is represented by the blue line. I then compared it to CPI, which is represented by the orange line. As you can see, CPRI tends to be a leading indicator. It peaked in October of 2021. Yet, it wasn’t until June of 2022 that CPI finally reached a 40+ year high before starting to roll over.

For January, our gauge had a reading of 5.7 compared to December’s 8.4. That’s close to the recent low of 4 made in November 2023 and a far cry from the peak of 52 back in November 2021. The important signal here is that price growth keeps falling.

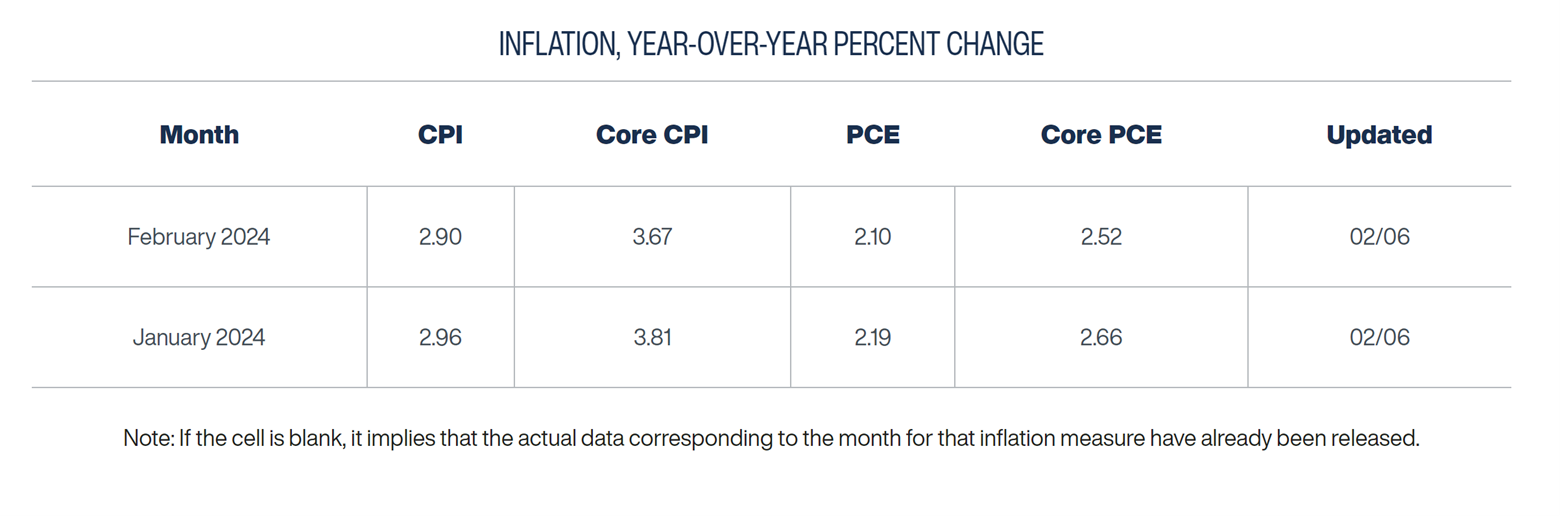

The next place I want to look for inflation trends is the Cleveland Fed’s inflation Nowcast estimate. The economic team updates its models and outlook daily for both CPI and the Bureau of Economic Analysis’ inflation measure, personal consumption expenditures (“PCE”). Take a look…

In December, CPI unexpectedly shot up to 3.4% from 3.1% the month prior. The change stoked speculation that inflation was back on the rise. But, as you can see in the table above, the Cleveland Fed expects price pressures to keep easing. Even with the release of the most recent economic numbers, it still anticipates inflation will fall to 3% for January and 2.9% in February.

So, I wanted to get an idea of what type of month-over-month growth the Cleveland Fed’s economic team is anticipating. That way, I can combine those numbers with the most recent monthly CPI data to get an idea of the trend. Then, I can forecast what annualized inflation might look like over the next year.

Now, from October through December, CPI has averaged 0.13% monthly growth. But, if I add in the Cleveland Fed’s January and February expectations, the monthly average rises to 0.18%.

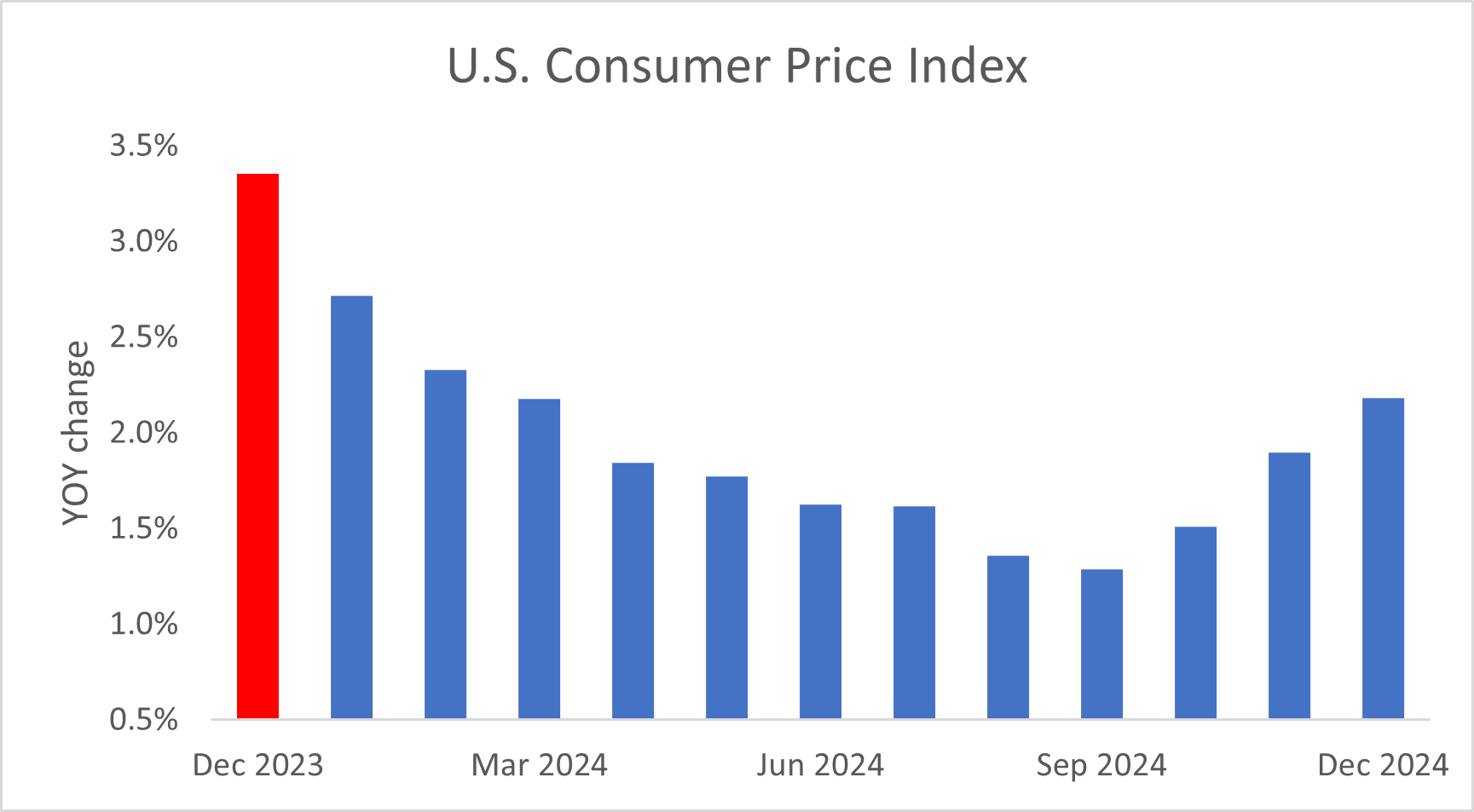

So, using the BLS CPI Price index, I ran my forecast based on a 0.18% pace of monthly growth. Take a look at the results…

The red bar on the left indicates December CPI growth of 3.4%. But, as you can see, the numbers are headed decidedly lower moving forward. The annualized rate of growth should fall to 2.7% when the January numbers are released. But then, by April, headline inflation will be back below the 2% level. And by September, it will have fallen as low as 1.3%.

So, like I said at the start, inflation isn’t done falling. We’re seeing signs the measure is returning back to more normal, pre-pandemic levels. And, if my model is correct, we could see CPI growth fall back below the Fed’s 2% sooner than later.

The change will act as a tailwind for the stock market. Because easing price pressures should increase the Fed’s conviction that inflation growth is slowing. That will give the central bank room to start cutting interest rates once more. The change will weigh on Treasury bond yields and lead to a steady rally in the S&P 500.

Five Stories Moving the Market:

Bank of England Deputy Governor Sarah Breeden said she had become less worried that interest rates would need to rise again as inflation pressures gradually abate; Breeden, the Monetary Policy Committee's newest member, said she was now thinking about how long interest rates would need to stay at their current level, instead of whether they would need to rise further – Reuters. (Why you should care – the BOE’s biggest hawk is backing down on her call for more rate hikes)

German industrial output extended its slump to a seventh month in December, underlining the struggles gripping Europe’s largest economy; the statistics office said production fell 1.6% in December compared to the expectation for a 0.5% decline, led by chemicals and construction – Bloomberg. (Why you should care -this is another sign Europe’s biggest economy continues to struggle)

The Palestinian militant group Hamas said it had delivered its response to a proposed ceasefire deal for Gaza that would also involve the release of hostages, and the United States said it still believed an agreement was possible – Reuters. (Why you should care – easing tensions in the Middle East would help to end attacks on ships in the Red Sea, relieving oil supply and inflation concerns)

Federal Reserve Bank of Philadelphia President Patrick Harker said a soft landing for the U.S. economy is in sight, pointing to falling inflation and a still-strong labor market - Bloomberg. (Why you should care – Harker’s comments imply the economy is on a path that will allow the central bank to normalize monetary policy)

New Zealand’s unemployment rate rose to 4.0% in the fourth quarter of last year from 3.9% in the third quarter, further confirming that a slowdown in the economy continues to play out – WSJ. (Why you should care – the unemployment rate has risen back to pre-pandemic levels, signaling the central bank can start to cut interest rates)

Global Macro:

Federal Reserve Bank of Cleveland President Loretta Mester said that if the U.S. economy performs as she expects it could open the door to rate cuts, but she’s not ready yet to offer any timing for easier policy amid ongoing inflation uncertainty – Reuters. (Why you should care – Mester, a noted hawk, said she feels the forecast for three rate cuts this year is reasonable)

Treasury Secretary Janet Yellen said that while losses in commercial real estate are a worry, U.S. regulators are working to ensure loan-loss reserves and liquidity levels in the financial system are adequate to cope; she said the increase in interest rates, higher vacancy rates thanks to shifting work patterns triggered by the pandemic and a wave of commercial real estate loans coming due this year – Bloomberg. (Why you should care – the Treasury Secretary is trying to placate fears about deteriorating bank balance sheets)

Economic Calendar:

Germany – Industrial Production for December (2 a.m.)

France – Private Sector Payrolls (Preliminary) for 4Q (2:45 a.m.)

BOE’s Breeden (Deputy Governor) Speaks (3:40 a.m.)

MBA Mortgage Applications (7 a.m.)

Trade Balance for December (8:30 a.m.)

Energy Information Administration Crude Oil Inventory Data (10:30 a.m.)

Fed’s Kugler Speaks (11 a.m.)

Fed’s Collins Speaks (11:30 a.m.)

Fed’s Barkin Speaks (12:30 p.m.)

Fed’s Bowman Speaks (2 p.m.)

Consumer Credit for December (3 p.m.)

Treasury Auctions $42 Billion in 10-Year Notes