ISM’s Manufacturing Survey Unlikely to Ease Stagflation Fears

The ISM Manufacturing survey is highly correlated with the NY Fed’s.

The Empire Manufacturing data pointed to increased weakness.

Rising input costs and slowing employment could stoke economic contraction fears.

Safe-haven asset demand is headed higher…

Over the last two months, investors have been worried about the domestic economic outlook. The administration of President Donald Trump has increasingly discussed plans to implement tariffs with most major trading partners. The plans are set to come to a head tomorrow when the White House is expected to introduce its reciprocal tariff plan.

Due to the buildup, Wall Street’s concerned those countries subject to the levies will turn around and implement retaliatory levies. After all, the heads of countries like Germany and Canada have said they’re already prepared to take such steps. The escalation could mean that prices for goods go up, both home and abroad, weighing on sales and economic demand.

One of the biggest issues is the lack of details around the administration’s intentions. One day it says it will implement huge levies and the next it’s backing down on those measures. The back and forth has created an increasingly volatile investing environment. And whenever economic data supports the case for slowing growth and higher prices, investors have grown increasingly anxious.

For instance, take a look at data from the Federal Reserve Bank of New York’s Empire Manufacturing Survey for March. After rising to start the year, overall activity has dropped to the lowest level in the last 15 months…

Later this morning, the Institute for Supply Management (“ISM”) will release its Manufacturing survey for March. The gauge is closely watched by Wall Street as a sign of overall economic health because it sends questionnaires to purchasing managers in various industries, across the country. Not only that, but the data is highly correlated to the NY Fed’s manufacturing survey.

Well, based on the recent Empire Manufacturing results, input prices rose while new orders and employment shrank. If the ISM results paint the same picture, it could stoke the stagflation narrative. That could cause investors to increasingly seek the safety of U.S. Treasury bonds.

But don’t take my word for it, let’s look at what the data’s telling us…

Every month, ISM sends questionnaires out to purchasing managers and manufacturing supply executives from over 400 manufacturing companies across various industries and regions. It asks them to detail the monthly change in factors such as new orders, production levels, employment, supplier deliveries, and inventories. It then compiles the numbers into an index, with industry weightings respective of GDP.

Now, according to a study from the Federal Reserve Bank of Richmond, the ISM report is closely correlated with the regional bank surveys. But the Empire Manufacturing Index tracks the ISM results closest. In fact, the two have a very high correlation coefficient of 83.4% (100% being perfect).

So, let’s look at the details…

The number most closely watched in the ISM index is the prices paid index. It’s what companies pay for the raw materials to produce goods. If they’re rising, Wall Street worries those increases will be passed onto consumers. In March, the New York Fed survey showed raw material costs rose…

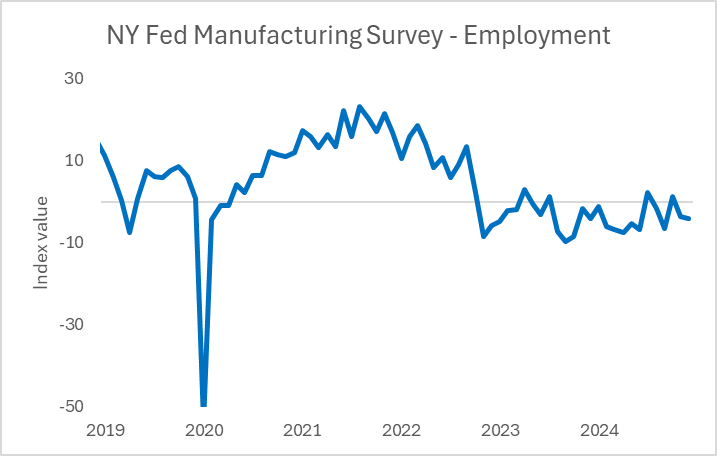

The next key number is the employment index. It tells us whether companies intend to hire or fire more workers. That’s important from an economic growth standpoint because a rising employment index means individuals with more money in their pockets… while a falling measure implies fewer people holding down jobs and less money to be spent. Based on the Empire state data, the hiring contraction got worse…

But there’s one other significant measure we want to observe. That’s the new order index. By looking at those numbers we can see what future business looks like. If orders are rising, companies will likely need to hire more employees, supporting domestic output growth. Conversely, if it’s falling, companies are unlikely to need as many workers, pointing to economic contraction. The New York Fed numbers showed a steep drop in new business…

Like I said above, the Empire data is highly correlated with ISM numbers. Now that doesn’t guarantee the March results for the two will be the same, but chances are high they will be.

Based on the numbers we just looked at, the manufacturing outlook is worsening. And, if you look at the data from the Dallas, Kansas City, and Philadelphia Fed surveys, you'll see the same trends. If the ISM report later today reflects that, it will heighten investor fears about falling growth and rising inflation. So, until Wall Street gets more comfortable with the White House’s tariff plans, the outlook will boost demand for safe-haven assets like U.S. Treasury bonds.

Five Stories Moving the Market:

The Office of the U.S. Trade Representative's annual National Trade Estimate Report detailed the roughly 60 countries whose policies and regulations it regards as trade barriers; the report showed the overall trade deficit with the U.S. increased between 2023 and 2024, driven by China, the European Union, and Mexico – Reuters. (Why you should care – these countries are likely to be the chief targets of the White House’s pending tariff policy)

Federal Reserve Bank of Richmond President Tom Barkin (centrist, non-voter) said the U.S. central bank would need to have confidence that inflation will keep falling before lowering interest rates again; he said it would take time before policymakers have a clearer idea on how President Donald Trump’s tariff policies might affect their interest-rate decisions – Bloomberg. (Why you should care – Barkin suggested an economic slowdown could provide the inflation slide the Fed’s seeking)

New York Federal Reserve President John Williams (centrist, voter) acknowledged there are risks that inflation could once again heat up, saying that monetary policy is "well positioned" for what the economy might do this year – Reuters. (Why you should care – Williams believes current policy is keeping downward pressure on inflation)

Several European Central Bank officials are still wavering on whether to cut interest rates next month, according to people familiar with the matter, suggesting the meeting remains far more open than investors are betting – Bloomberg. (Why you should care – given the euro is the biggest weighting in the dollar index, an ECB rate pause would likely place downward pressure on the dollar)

OpenAI has raised $40 billion in new funding from SoftBank and other investors, valuing the ChatGPT maker at $300 billion as it becomes one of the best-funded private start-ups in the world – FT. (Why you should care – the new funding round practically doubles the valuation compared to its last raise in October)

Economic Calendar:

Reserve Bank of Australia Monetary Policy Announcement

China – Caixin China (Small Company) Manufacturing Index for March

Japan – au Jibun Bank Manufacturing PMI (Final) for March

Japan – Tankan Manufacturing Index for 1Q

Eurozone – HCOB Eurozone Manufacturing PMI (Final) for March (4 a.m.)

U.K. – S&P Global U.K. Manufacturing PMI (Final) for March (4:30 a.m.)

Eurozone – CPI (Preliminary) for March (5 a.m.)

ECB’s Lagarde (President) Speaks (8:30 a.m.)

Fed’s Barkin (Richmond, Non-voter) Speaks (9 a.m.)

U.S. - S&P Global U.S. Manufacturing PMI (Final) for March (9:45 a.m.)

U.S. – ISM Manufacturing PMI for March (10 a.m.)

U.S. – JOLTS Job Openings for February (10 a.m.)

ECB’s Lane (Chief Economist) Speaks (12:30 p.m.)

U.S. - American Petroleum Institute Crude Oil Inventory Data (4:30 p.m.)