Job Openings Confirm Rate Cut Outlook

Job Openings Confirm Rate Cut Outlook

• Job Openings rose to 7.44 million in October.

• That compares to roughly 7 million unemployed persons.

• The ratio of job openings to unemployed is stabilizing around pre-pandemic levels.

We just received another signal the labor market is returning to normal…

I like to pay close attention to monetary policy for one major reason… it tells us whether the access to money is getting easier or harder. That’s important because the direction of interest rates tells us what kind of appetite Wall Street and Main Street will have. If rates are rising, they’ll be inclined to put more money to work in bonds, given the safety of high coupon payouts. But if rates are falling, those same investors favor the high returns of riskier assets like stocks.

Right now, Wall Street and Main Street are worried our central bank may be losing its ability to lower interest rates. The Atlanta Fed’s GDPNow forecast shows gross domestic product growth will hit 3.2% in the fourth quarter. At the same time, they’re worried about the potential for increased trade tensions next year when President-elect Donald Trump takes office.

However, those investors are forgetting the driving factors behind recent rate cuts by our central bank… the slowdown in inflation and employment growth. Over the last couple of weeks, we’ve received data confirming inflation remains on a sustainable path toward the Fed’s 2% target. And this week, we’ll get more clarity on the stability of the job market.

Well, yesterday, we got our first piece of key employment data. It came in the form of job openings numbers. And based on what I see, labor market conditions are stabilizing around pre-pandemic level of activity. That means the Fed can push forward with lowering interest rates closer to neutral (neither hurts nor helps economic growth). That should support a breakout rally in domestically focused small cap stocks.

But don’t take my word for it, let’s look at what the data’s telling us…

Every month, the U.S. Bureau of Labor Statistics (“BLS”) released its Job Openings and Labor Turnover Survey (“JOLTS”) data. The measure is based on questionnaires sent out to roughly 21,000 public and private businesses, based on industry, size, and geography. It asks them about job openings, quits, and hires. The BLS then tabulates the numbers to produce an estimate of what the state and national pictures look like.

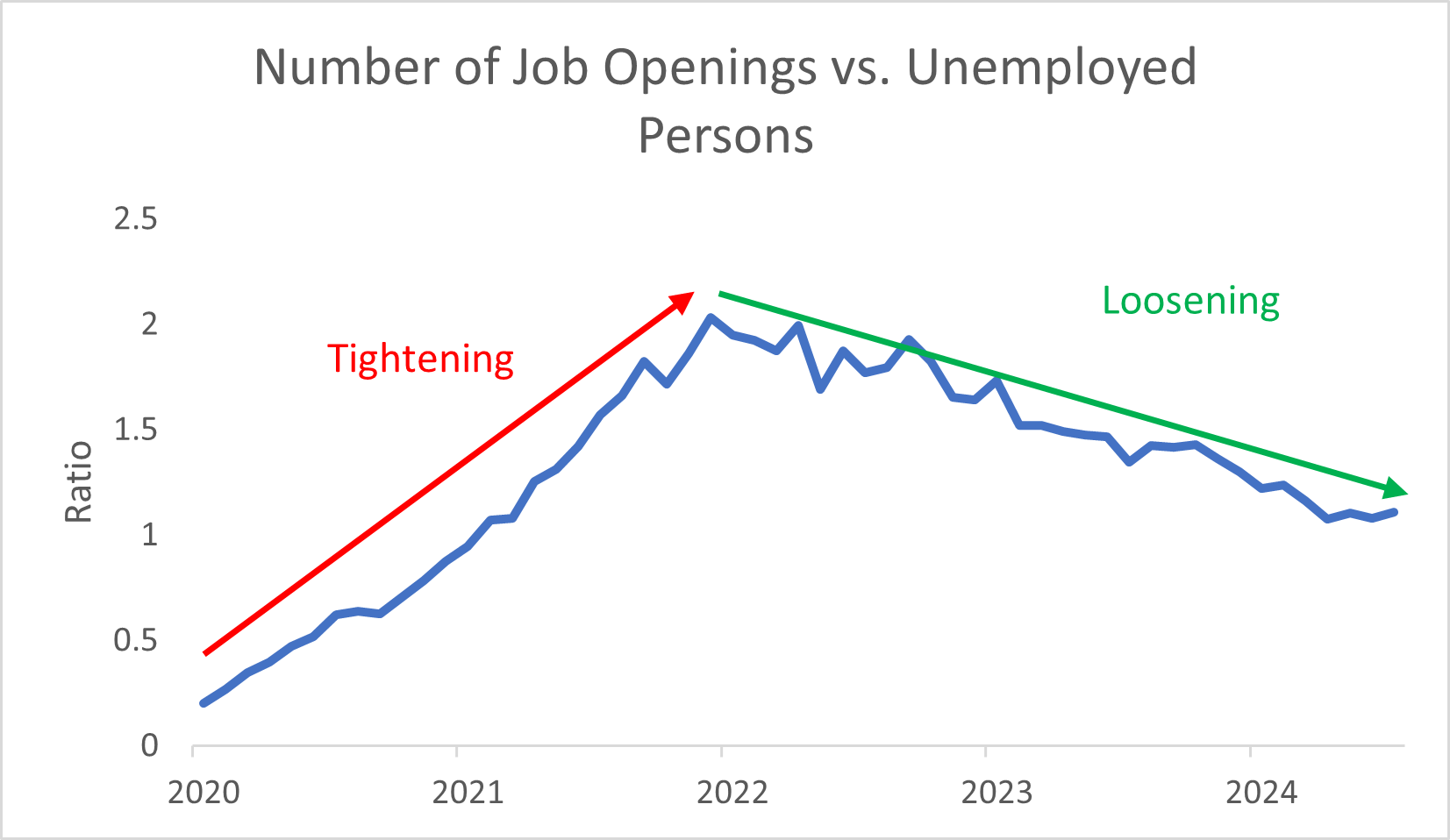

The number is important as it relates to interest-rate decisions. You see, policymakers use the ratio of job openings to unemployed persons to tell whether the labor market is tight (more jobs than available workers) or loose (more available workers than jobs). The difference being a tight market is one in which wages and inflation rise rapidly, while a loose market is one where wages and inflation experience a more gradual increase.

Yesterday, the BLS released its JOLTS data for October. The number of job openings rose to 7.74 million compared to the almost 7 million unemployed individuals…

The results mean there are roughly 1.1 available jobs for each person seeking work. That’s a far cry from the 2.1 peak we experienced back in March 2022 when the Fed began raising interest rates. And it marks the fifth straight month the number has held around these levels. But even more importantly, the number is back in line with the levels we saw prior to the pandemic.

Now look at the numbers between 2018 and 2020…

As you can see in the above chart, the ratio of job openings to unemployed persons held in a tight range between 1.1 and 1.2 between 2018 and 2020. That’s the same level where we appear to be stabilizing today.

So, let’s put it in perspective…

Between 2018 and 2020, the effective federal funds rate also held in a tight range between 1.75% and 2.5%. That’s far lower than the 4.9% rate we’re experiencing today. And inflation growth, as measured by personal consumption expenditures, averaged roughly 1.8%. Based on the trend in the six-month average, price pressures are starting to stabilize around a similar level.

When the Fed started raising interest rates, it had a singular objective… to return the economy back to normal, pre-pandemic levels of activity. According to the numbers we just looked at, that’s happening. The path lower in inflation growth has been bumpy, but it continues to drop. And hiring and unemployment figures tell us the job market is back to pre-pandemic normal. As a result, the last step in the process is normalizing borrowing costs as well.

As I said at the start, I like to follow monetary policy to see whether the access to money is getting harder or easier. Based on current annualized PCE growth of 2.3% and an effective fed funds rate of 4.9%, our central bank has plenty of room (roughly 260 basis points worth) to ease policy more. That means it should become much easier to borrow funds moving forward. As rates fall, it will disincentivize savers to invest in bonds or money market funds, instead pushing them toward higher returns in stocks. That will power a steady rally in domestically-focused small-cap stocks.

If you’re interested in investing in this trend, take a look at the Vanguard Russell 2000 ETF (VTWO). It invests in stocks in the Russell 2000 Index, seeking to track the gauge’s returns. It trades about 1.7 million shares a day so it should be easy to buy and sell.

Five Stories Moving the Market:

Australia’s commodity-rich economy grew by a less-than-expected 0.3% in the third quarter, stoking concerns that it might still be at risk of sinking into recession over coming quarters – WSJ. (Why you should care – slowing growth could lead the Reserve Bank of Australia to consider lowering interest rates sooner than later; current expectations are for the second quarter of next year)

China's services activity expanded at a slower pace in November, pressured by easing new business growth, including in exports, a private sector survey showed, as the economy braces for a rocky ride of more U.S. tariffs under a second Trump administration – Reuters. (Why you should care – recent economic data point to an uneven economic recovery in China)

Federal Reserve Bank of San Francisco President Mary Daly said an interest-rate cut this month isn’t certain but remains on the table for policymakers; Daly’s comments put her roughly in line with several other policymakers who’ve spoken this week and made clear they expect the U.S. central bank to continue cutting interest rates over the next year – Bloomberg. (Why you should care – Daly said policy will remain restrictive even with another rate cut, meaning there’s plenty of room to ease)

Federal Reserve Board Member Adriana Kugler said the economy is in a good position after making significant progress in recent years toward our dual-mandate goals of maximum employment and stable prices – Reuters. (Why you should care – Kugler signaled stabilization in the labor market and inflation growth allow the central bank to return interest rates to neutral)

Federal Reserve Bank of Chicago President Austan Goolsbee says interest rates still need to come down a "fair amount" during a keynote conversation about the Midwest economy and U.S. monetary policy – Bloomberg. (Why you should care – Goolsbee will become a monetary policy voter in January, so his statements now foreshadow future interest rate leanings)

Economic Calendar:

China – Caixin Chima (Small and Mid-Sized Company) Services, Composite PMI for November

Japan – au Jibun Bank Japan Services, Composite PMI (Final) for November

Eurozone – HCOB Eurozone Services, Composite PMI (Final) for November (4 a.m.)

BOE’s Bailey (Governor) Speaks (4 a.m.)

U.K. – S&P Global U.K. Manufacturing PMI (Final) for November (4:30 a.m.)

U.S. - MBA Mortgage Applications (7 a.m.)

ECB’s Lagarde (President) Speaks (8:30 a.m.)

U.S. – S&P Global U.S. Manufacturing PMI (Final) for November (9:45 a.m.)

ISM Non-Manufacturing PMI for November (10 a.m.)

Energy Information Administration Crude Oil Inventory Data (10:30 a.m.)

ECB’s Lagarde (President) Speaks (10:30 a.m.)

ECB’s Nagel (Germany) Speaks (12:10 p.m.)

Fed’s Powell (Chairman) Speaks (1:45 p.m.)

Fed’s Beige Book (2 p.m.)