November CPI Data to Support Fed Policy Shift

Inflation growth is set to slow even more…

Next week brings another important investing-outlook clue for the domestic stock and bond markets… the U.S. Bureau of Labor Statistics (“BLS”) releases consumer price index (“CPI”) growth figures for November.

After hitting a more than four-decade high of 9.1% growth in June 2022, inflation began dropping rapidly. By June of this year, the metric had tumbled all the way down to just 3%. But then, it began to reaccelerate as the numbers lapped the difficult year-over-year comparisons. In addition, consumer spending jumped over the summer, as households used up what remained of their excess COVID savings.

However, as we’ve moved beyond summer, economic activity has started to slow. According the federal Reserve’s November Beige Book survey, 8 of the 12 regional-bank districts noted a drop in activity. They said retail sales are falling and consumer credit delinquencies are rising. As a result, the report noted the economic outlook for the next 6 to 12 months has worsened, a downward shift from the October update.

But there’s an upside… declining growth will weigh on inflation. After all, less spending means a drop in goods demand. That should translate into prices remaining steady, at a minimum, and possibly falling if companies get stuck with inventory.

Based on what I’m seeing in central bank manufacturing surveys, inflation growth looks set to fall even more when the November data is released next week. That should tell the Fed it doesn’t need to raise interest rates further and could soon have room to cut once more. The change will support a continued rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data is telling us…

Every month, the Dallas, Kansas City, New York, and Philadelphia Feds ask manufacturers in their districts about the state of activity. The questionnaires ask companies about things like new orders, lead times, employment, and production. The survey details whether costs are rising, falling, or unchanged.

But we must focus on “prices received for goods.” The number indicates what customers pay manufacturers for their finished product. It’s akin to CPI. So, the direction of prices received is an indicator of whether inflation is rising or falling.

Now, the states where those four banks are headquartered – Texas, Missouri, New York, and Pennsylvania – account for roughly 23% of domestic economic output. So, we can get a decent idea of national demand. But the results come out ahead of CPI, so it’s like having an early indicator.

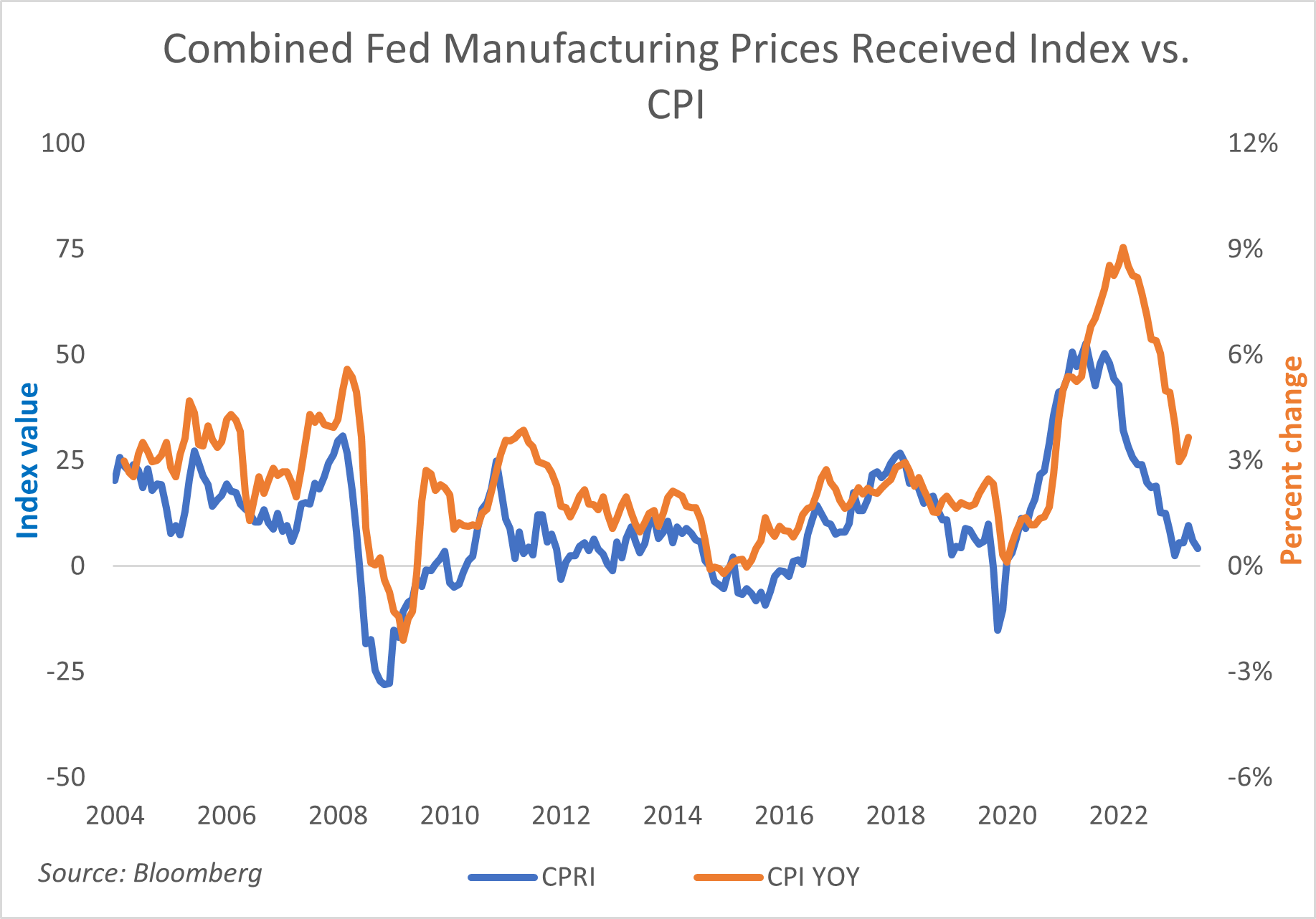

And the latest readings indicate prices received are falling…

In the above chart, I combined the readings from the four central banks into a single gauge. It’s called the combined prices received index (CPRI) and represented by the blue line. I then compared it to CPI, which is represented by the orange line. As you can see, CPRI tends to be a leading indicator. It peaked in October of 2021. Yet, it wasn’t until June of 2022 that CPI finally reached a 40+ year high before starting to roll over.

The November CPRI reading fell from 6 to 4. That’s in addition to the slide in October, which was an early indicator CPI would ease. So, don’t be surprised when the report next week confirms what my indicator’s telling us.

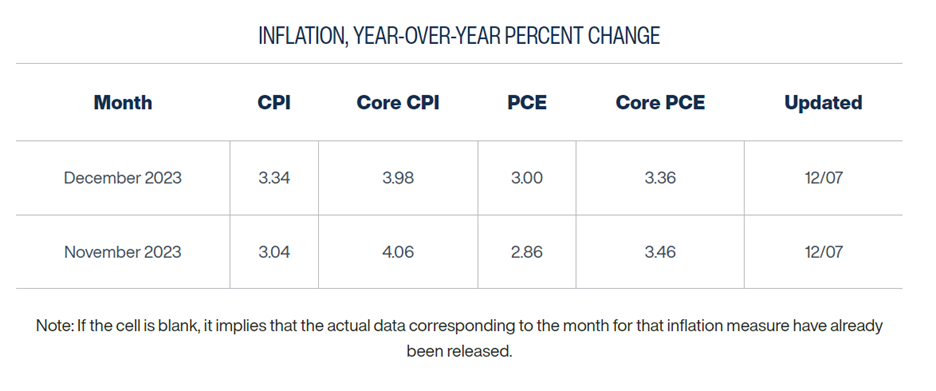

Supporting my thinking is the most recent Inflation Nowcast from the Cleveland Fed. It’s data also points to a drop…

As you can see in the table above, the Cleveland Fed model expects November CPI will drop to just 3% growth compared top 3.2% in October. That would mark the lowest reading since inflation growth began to take back in early 2021. In addition, it’s worth noting that the Cleveland Fed’s model tends to be high. In other words, there’s potential that CPI could fall below 3% when the number is released.

Currently, Wall Street expects CPI to drop to 3.1%. If we see the year-over-year result fall below 3%, it should act as a tailwind for the stock market. Because easing price pressures should increase the Fed’s conviction that inflation growth is slowing.

Eventually, if we see inflation growth come back to 2%, it will mean the Fed would have room to start cutting rates once more. That will weigh on Treasury bond yields and lead to a steady rally in the S&P 500.

Five Stories Moving the Market:

China’s Politburo pledged to strengthen the government’s fiscal measures and make monetary policy more effective, bolstering efforts to stabilize growth – Bloomberg. (Why you should care – China’s economic issues point to slowing global growth)

Chinese leader Xi Jinping and Europe’s top officials sought to ease tensions over trade and economic disputes at their first in-person summit in Beijing on Thursday – WSJ. (Why you should care – increasing trade tensions with the world’s major economies will only weigh on China’s economic growth)

Japan's economy fell faster than first estimated in the third quarter, revised data showed on Friday, as the household sector faced growing headwinds, complicating the central bank's efforts to phase out its accommodative monetary policy – Reuters. (Why you should care – declining economic growth could force the Bank of Japan easy-money monetary policy for the foreseeable future)

Apple and its suppliers aim to build more than 50 million iPhones in India annually within the next two to three years, with additional tens of millions of units planned after that, according to people involved – WSJ. (Why you should care – the shift by Apple is part of the continued supply-chain shift away from China, likely straining the country’s economy)

Nonfarm payroll growth for November is expected to show moderating employment and wage growth in November but no major deterioration in hiring; payrolls probably grew by 185,000 last month, after increasing 150,000 in October, while the unemployment rate held steady at 3.9% - Bloomberg. (Why you should care – given the recent rally in bonds, higher than expected job gains could prompt profit taking)

Economic Calendar:

ECB’s Muller Speaks (2:35 a.m.)

Bank of England Inflation Expectations for November (4:30 a.m.)

Change in Nonfarm, Manufacturing, and Private Payrolls for November (8:30 a.m.)

Unemployment Rate for November (8:30 a.m.)

University of Michigan Consumer Sentiment, Inflation Expectations (Preliminary) for December (10 a.m.)

Baker Hughes Rig Count (1 p.m.)

CFTC’s Commitment of Traders Report (3:30 p.m.)

Fed Releases Balance Sheet Updates on Commercial Banks (4:15 p.m.)