PCE Inflation Growth Held Steady in May

The Cleveland Fed expects May PCE growth sub 0.1%.

The outcome would mean annualized growth of around 2.2%.

That would mean the Fed has 220 basis points worth of rate-cut potential.

The Federal Reserve’s preferred inflation gauge is unlikely to show a resurgence…

The end of this week brings the next key update on inflation. The U.S. Bureau of Economic Analysis (BEA) releases its May personal consumption expenditures (PCE) data. This update matters because our central bank relies on this index when making monetary policy decisions.

The Fed considers PCE a more comprehensive inflation gauge because it measures total spending on goods and services consumed by individuals, including purchases made on their behalf - such as health insurance. By contrast, the U.S. Bureau of Labor Statistics’ consumer price index (CPI) focuses on out-of-pocket spending by urban consumers.

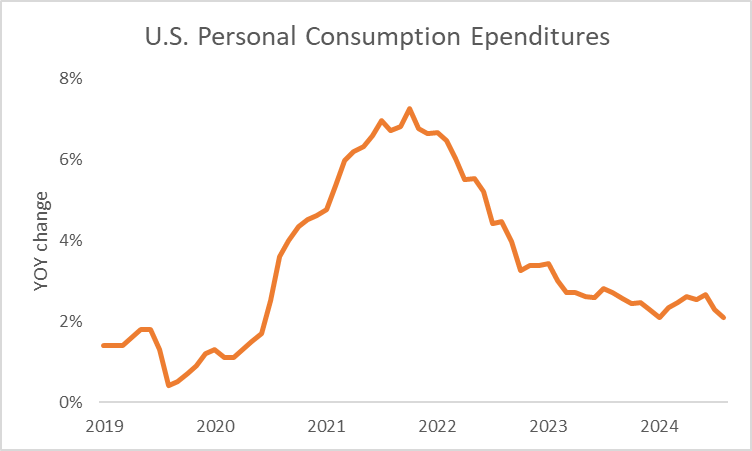

Consequently, the individual weights within PCE are less concentrated than those in CPI, making PCE less volatile. That stability reinforces the Fed’s preference. As shown in the following chart, the pace of price increases has been steadily declining since peaking in mid-2022.

Growth in services prices remains subdued, according to recent business surveys. This trend should have a greater influence on PCE compared to CPI. Based on the numbers I reviewed, the Fed’s preferred inflation gauge saw little growth in May, which supports the case for easier monetary policy later this year. This shift would likely underpin a steady long-term rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

A couple of weeks ago, the BLS released its consumer and producer price index data for April. Within those indexes, several readings offer insight into PCE trends. According to the data, items such as housing and health care rose in price, while categories like transportation, food and accommodation, as well as financial services and insurance, contracted.

Housing and medical expenses each account for roughly 17% of the PCE index, while other categories have weightings ranging from 3% to 8%. I compared the BLS inputs to the relative PCE weightings, and the numbers suggest a slight rebound in the pace of growth in May compared to April.

Confirming this is the Inflation Nowcast from the Federal Reserve Bank of Cleveland. The Fed’s economic staff continuously updates its outlook based on the most recent data. According to their forecast, PCE growth in May was sub 0.1%, roughly in line with April.

Now, let’s examine the implication for the annualized growth rate…

The table above details the pace of monthly PCE growth over the past year. To estimate the annualized rate when the new numbers are released at the end of this week, I substituted last May’s 0% growth with this year’s forecast from the Cleveland Fed. When you add up the monthly totals (after backing out the rounding), the annualized rate increases to 2.2% from 2.1% in April. That aligns with the pace Federal Reserve Chairman Jerome Powell outlined at the central bank’s monetary policy meeting last week.

As Powell has recently said, policy makers feel it’s still too early to disregard the potential inflationary impact of tariffs. The Fed needs more time to assess how policy implementation affects prices. However, based on May’s data and early indications for June, growth is easing. When subtracting May’s 2.2% PCE forecast from the effective federal funds rate of 4.4%, it suggests 220 basis points of potential rate cuts.

So, when PCE numbers are released at the end of the week, they should confirm little change in monthly growth. This outcome will give the Fed greater confidence in normalizing monetary policy when the time is right. The ability to support steady economic growth should fuel a long-term rally in the S&P 500 Index.

Five Stories Moving the Market:

The United States struck three sites in Iran, inserting itself into Israel’s war aimed at destroying the country’s nuclear program in a risky gambit to weaken a longtime foe despite fears of a wider regional conflict – AP News. (Why you should care – U.S. officials have said it wants to end the country’s nuclear program and are prepared for talks with Tehran)

Israel is very close to completing its goal of removing the dual threats of Iran's ballistic missiles and nuclear program, according to Prime Minister Benjamin Netanyahu – Reuters. (Why you should care – this could mark the final stages of Israel’s broader campaign against Iran that started in the fall of 2023)

U.S. Secretary of State Marco Rubio called on China to encourage Iran to not shut down the Strait of Hormuz; he said a move to close the strait would be a massive escalation that would merit a response from the U.S. and others – Reuters. (Why you should care – roughly 20% of the world’s oil passes through the Strait of Hormuz)

Federal Reserve Governor Christopher Waller said the central bank can lower interest rates as soon as next month, reiterating his view that the inflation hit from tariffs is likely to be short-lived – Bloomberg. (Why you should care – Waller has been the most economically prescient of all the Fed members)

Federal Reserve Bank of San Francisco President Mary Daly said she sees the central bank’s monetary policy stance as “in a good place” currently, with risks to its U.S. employment and price stability mandates as roughly equal – Bloomberg. (Why you should care – Daly said she anticipates more rate cuts in the fall)

Economic Calendar:

Fed’s Daly (San Francisco) Speaks (Sunday)

Japan – au Jibun Bank Japan Manufacturing, Services, Composite PMI (Preliminary) for June

Fed’s Waller (Board Member) Speaks (3 a.m.)

Eurozone – HCOB Eurozone Manufacturing, Services, Composite PMI (Preliminary) for June (4 a.m.)

U.K. – S&P Global U.K. Manufacturing, Services, Composite PMI (Preliminary) for June (4:30 a.m.)

ECB’s Lagarde (President) Speaks (9 a.m.)

U.S. – S&P Global U.S. Manufacturing, Services, Composite PMI (Preliminary) for June (9:45 a.m.)

U.S. – Existing Home Sales for May (10 a.m.)

Fed’s Bowman (Board Member) Speaks (10 a.m.)

ECB’s Nagel (Germany) Speaks (11 a.m.)

Treasury Auctions $76 Billion in 13-Week Bills (11:30 a.m.)

Treasury Auctions $68 Billion in 26-Week Bills (11:30 a.m.)

Fed’s Goolsbee (Chicago) Speaks (1:10 p.m.)

Fed’s Kugler (Board Member) Speaks (2:30 p.m.)

Fed’s Williams (New York) Speaks (2:30 p.m.)

U.S. - CFTC’s Commitment of Traders Report (3:30 p.m.)