Prepare for a Springtime CPI Collapse

December CPI was unchanged on a non-seasonally adjusted basis.

The six-month average pace of monthly growth is sub 0.1%.

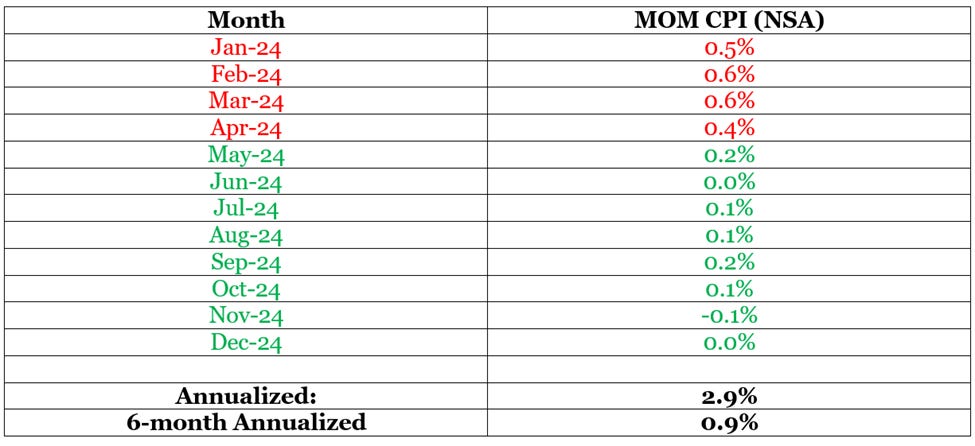

That equates to an annualized pace of 0.9%

Annualized inflation growth is on the verge of falling apart…

Early in my career, I was fortunate enough to work with some very sharp people. The firm I worked for had hired a team from one of the oldest investment banks in the country. Many of these people had spent much of their careers working for the same firm. But the company had sold itself to a foreign entity and they were moving headquarters somewhere else. So, when they joined my firm, they brought generations of passed-down business wisdom with them.

It was such a successful investment bank because it made sure the people who worked there employed best practices in everything they did. One of those habits was always being proactive instead of being reactive. The employees challenged each other to act and think about where the environment was headed. That way, they were always prepared for any challenge that lay ahead.

And the longer I spent working with the group, the more I saw these habits pay off. The research analysts, salespeople, and traders always seemed to be a step ahead of the market. Because they spent so much time studying, analyzing, and understanding, they were better able to help their clients prepare for every environment. And in the process, they made complicated situations seem routine.

Recently, I’ve been reminded of those habits I learned and now employ. Yesterday, the talking heads in the financial media were in a panic about the December consumer price index (“CPI”) data from the U.S. Bureau of Labor Statistics (“BLS”). Some of the commentators on CNBC labeled the increase in annualized growth a disaster.

Yet as I stated back in November, the pace of growth would increase into year end, before rapidly fading in the first part of this year. And as the shift happened, it would likely catch the markets and financial media off guard. Well, based on yesterday’s numbers, the rollover should soon start to happen. And if annualized inflation starts to drop as I expect, it will lead to a steady rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

Yesterday, the BLS reported its headline consumer price index rose 2.9% on an annualized basis. Now, while that was in-line with the consensus expectation, it was an increase compared to the November gain of 2.7%. So, it appeared that price pressures were rising.

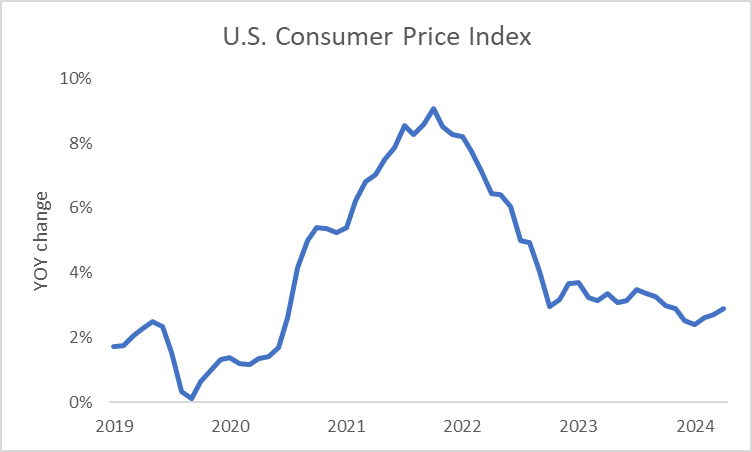

Compounding matters was the way monthly growth is reported. The BLS releases the data on a seasonally adjusted basis (accounts for things like weather). That number showed a 0.4% increase for December. It was the highest reading since April and double the number from November. The implication being that inflation growth is accelerating, hence the media reaction.

However, those outlets weren’t digging into the entire picture. To get a better sense of how the headline-annualized numbers are shaping up, I like to look at the non-seasonally-adjusted numbers (raw data). After all, that’s how the annual numbers are reported. And according to those results, inflation growth was unchanged in December compared to November...

So, the numbers drawing the headlines made inflation seem like it's heating up. But when we focus on the non-seasonally-adjusted data, we see something different taking place.

Like I said at the start, there’s a shift taking place because of the way the yearly numbers are calculated. You see, it’s a sum total of each month’s growth. By looking at the above chart, we notice the numbers from January through April of last year ran hot. But ever since, they’ve been trending lower. And moving forward, those high numbers from last year will start disappearing when the January data’s released. That means the pace of annualized growth could start to cool rapidly...

In the above table I’ve highlighted the numbers in two different shades. The red ones are the hot numbers, indicating inflation is picking up, while the green numbers tell us price pressures are cooling. If we add the data up from January through April, we see that it accounted for 2.1% of the 2.9% growth over the last 12 months. That means that May through December only accounted for 0.8%.

But to get a sense of the trend moving forward, we can observe the six-month average. Because, that number removes the older data that’s about to disappear. And according to the result, the pace of monthly inflation growth since July has averaged just under 0.07%. That works out to just 0.9% on an annualized basis....

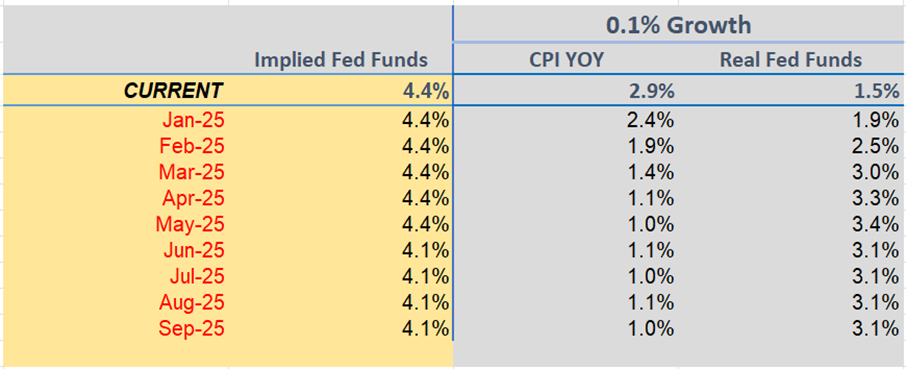

To take it step further, I calculated what the pace of inflation growth would look like moving forward based on 0.1% monthly growth. According to the result, we could see headline CPI growth fall below the Federal Reserve's 2% target as soon as February....

Not only that, but based on current interest rate expectations, the change would push the real rate of interest (implied federal funds minus CPI) above 3% before the middle of this year. That would be the highest level of the current cycle. In fact, you’d have to go back to 2006 to see a higher number.

So, like I said at the start, the media tends to be reactive. Instead of digging into what’s really going on, they’re looking to get you worked up. By getting you worked up, they’re hoping you’ll pay more attention.

But based on the numbers we just surveyed, the storm clouds are about to lift. As I showed you, inflation growth could drop below the central bank’s 2% target as soon as February. That’s an event that Wall Street isn’t anticipating. But as they figure it out, those investors will start to change course. The change will underpin a steady rally in the S&P 500.

Five Stories Moving the Market:

Economic activity increased “slightly to moderately” across the U.S. in late November and December, supported by strong holiday sales, the Federal Reserve said in its Beige Book survey of regional business contacts – Bloomberg. (Why you should care – businesses worried that potential changes to immigration and tariff policies could hurt the growth outlook)

Federal Reserve Bank of New York President John Williams said that future monetary policy actions will be driven by economic data as the central bank confronts a high level of uncertainty in large part driven by potential government policy changes – Reuters. (Why you should care – Williams still believes inflation growth is headed lower, leaving the door open for rate cuts later this year)

Federal Reserve Bank of Richmond President Tom Barkin said fresh data show continued progress on lowering inflation toward the central bank’s 2% goal, but that interest rates should remain restrictive – Bloomberg. (Why you should care – Barkin wants to see more signs of economic growth slowing before moving forward with more rate cuts)

Markets cheered a December inflation report that suggested underlying price pressures are easing; the overall consumer-price index came in relatively hot, rising 2.9% over the year, but core CPI, which excludes volatile food and energy prices, rose 0.2%, its smallest gain since July and less than the 0.3% increase expected – WSJ. (Why you should care – annualized inflation growth should be back below the Federal Reserve’s 2% target by the start of the second quarter)

Negotiators for Israel and Hamas agreed to a deal to pause their fighting in the Gaza Strip, Arab mediators and the U.S. said, opening a pathway to end a 15-month war – WSJ. (Why you should care – resolution of the conflict should help to remove a stock market overhang)

Economic Calendar:

Earnings – BAC, MS, MTB, PNC, UNH, USB

Bank of Korea Policy Announcement

China – Loan Prime Rate for January

Japan – PPI for December

BOC’s Gravelle (Deputy Governor) Speaks 12:30 a.m.)

U.K. – GDP for November (2 a.m.)

BOE Credit Conditions Survey (4:30 a.m.)

ECB Meeting Minutes (7:30 a.m.)

U.S. - Initial Jobless Claims (8:30 a.m.)

U.S. - Continuing Claims (8:30 a.m.)

Retail Sales for December (8:30 a.m.)

Philly Fed Business Outlook Survey for December (8:30 a.m.)

U.S. - Energy Information Administration Weekly Petroleum Inventories (10:30 a.m.)

Fed’s Williams (New York) Speaks (11 a.m.)

BOC’s Gravelle (Deputy Governor) Speaks (12:30 p.m.)

Fed's Balance Sheet Update (4:30 p.m.)