Recent House Price Data Signal Inflation Downside

We just received another indicator pointing to easing price pressures…

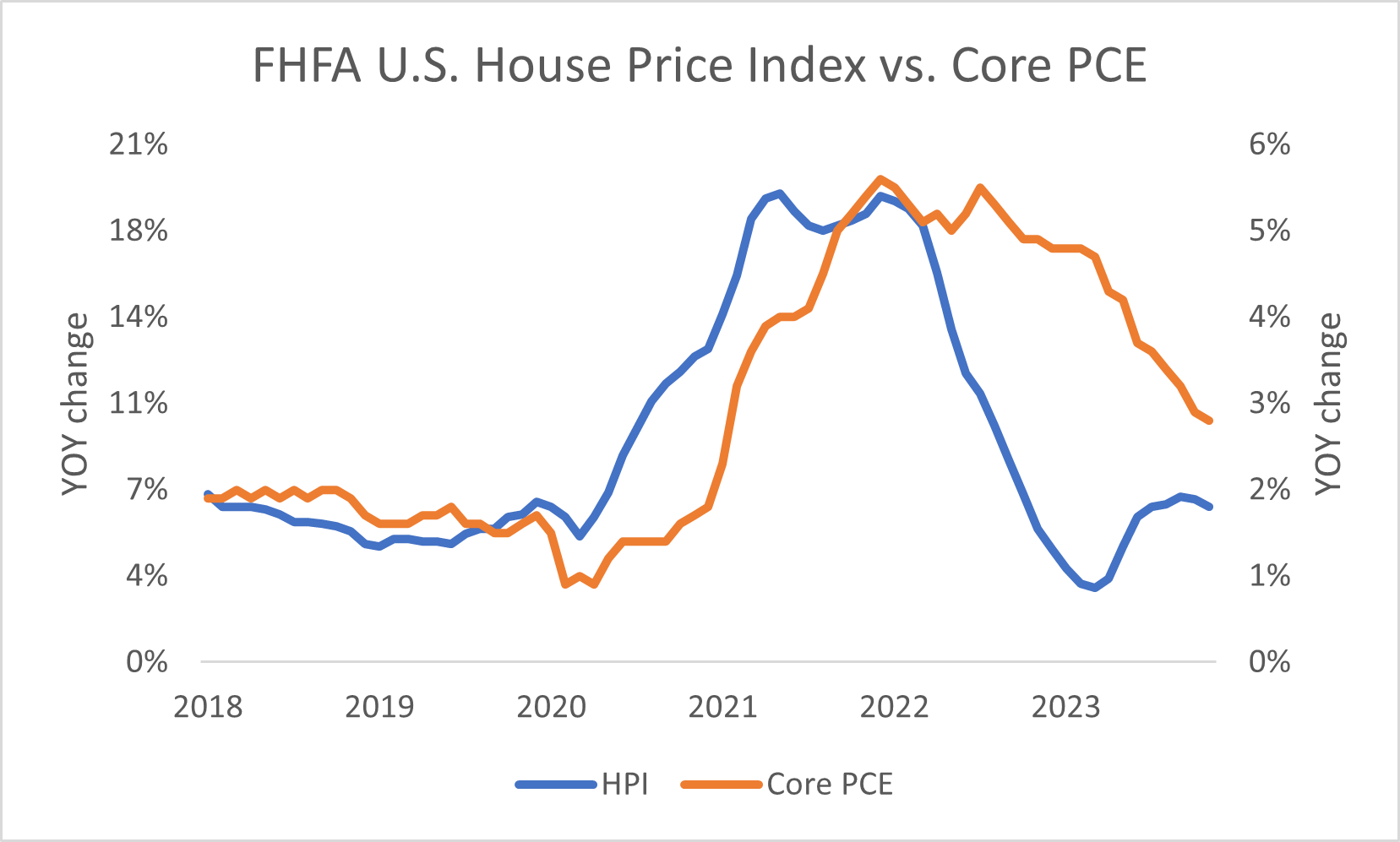

Earlier this week, both the Federal Housing Finance Agency (“FHFA”) and S&P CoreLogic Case-Shiller released Home Price Index (“HPI”) data for January. In both instances, the numbers showed price growth was weaker than expected.

According to the FHFA, prices contracted 0.1% month over month in January compared to the expectation for 0.3% growth and the prior month’s 0.1% expansion. On an annualized basis, the rate of increase slowed from 6.6% at the end of 2023 to 6.3% at the start of this year. Meanwhile, the Case-Shiller index showed an annualized gain of 6% in house prices compared with the 6.1% estimate and December’s 5.6% jump.

Now, while the results are near-term positives, we want to consider them from a long-term inflation perspective. Because, the bigger-picture trend is going to affect future interest-rate decisions from the Federal Reserve. And based on what I’m seeing, the numbers indicate price pressures should ease going forward. The change should support a steady rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

To see the broader implications of house-price shifts, let’s look at the year-over-year changes in HPI. That way we’re getting a better idea of the long-term trend versus the choppier month-to-month dynamics. And, if we’re going to gauge the interest rate outlook, we must compare the HPI data to the Federal Reserve’s preferred inflation gauge, core personal consumption expenditures (“PCE”).

As you can see in the following chart, the FHFA’s HPI tends to be a leading indicator of inflation…

Prior to the pandemic-driven surge in prices, HPI and PCE moved closely with one another. But then in mid-2020, HPI exploded higher. At the time, consumers were flush with COVID stimulus and looking to get out of densely-populated cities. However, house price growth peaked in July 2021, nine months before core PCE. The Fed signaled it would have to raise interest rates to combat rising inflation.

Today, the rate of change in house price growth is leveling off at pre-pandemic levels. A series of rapid rate increases and the evaporation of excess COVID stimulus has slowed demand. As economic activity returns toward pre-pandemic levels, I would expect the lag-effect gaps between HPI and PCE to narrow and converge once more. So, based on what the data above is showing, there’s more downside ahead in inflation growth.

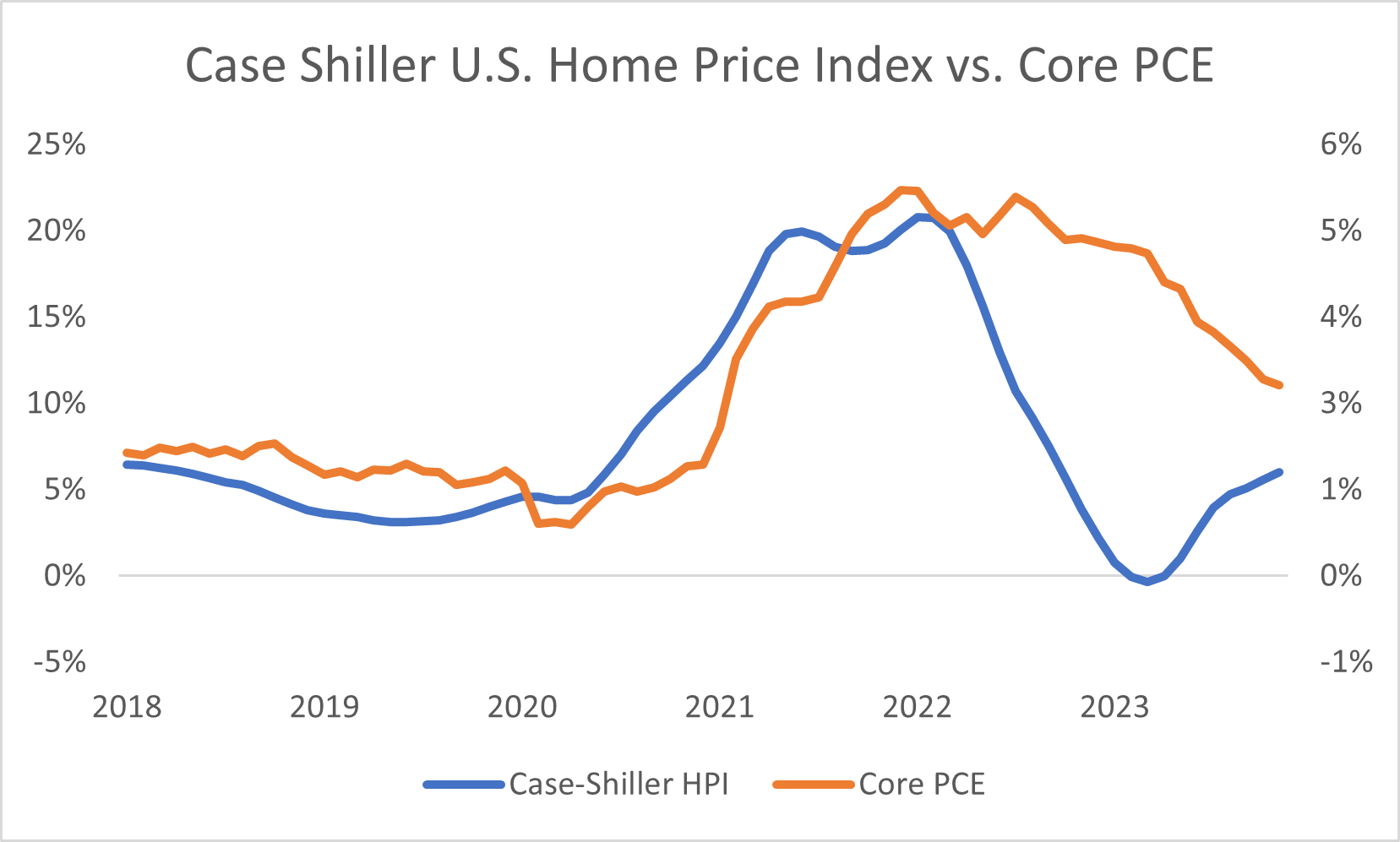

Next, let’s look at Case-Shiller’s annualized numbers compared to core PCE…

Like the earlier FHFA example, the Case-Shiller data paint a similar picture. The two gauges were in sync pre-COVID… after a stimulus-driven increase in housing demand, HPI jumped and PCE was slow to catch up… now, the numbers are falling as demand eases and economic activity shows signs of stabilizing around pre-pandemic levels. So, again, based on what the data indicate above, there appears to be more downside ahead in inflation growth.

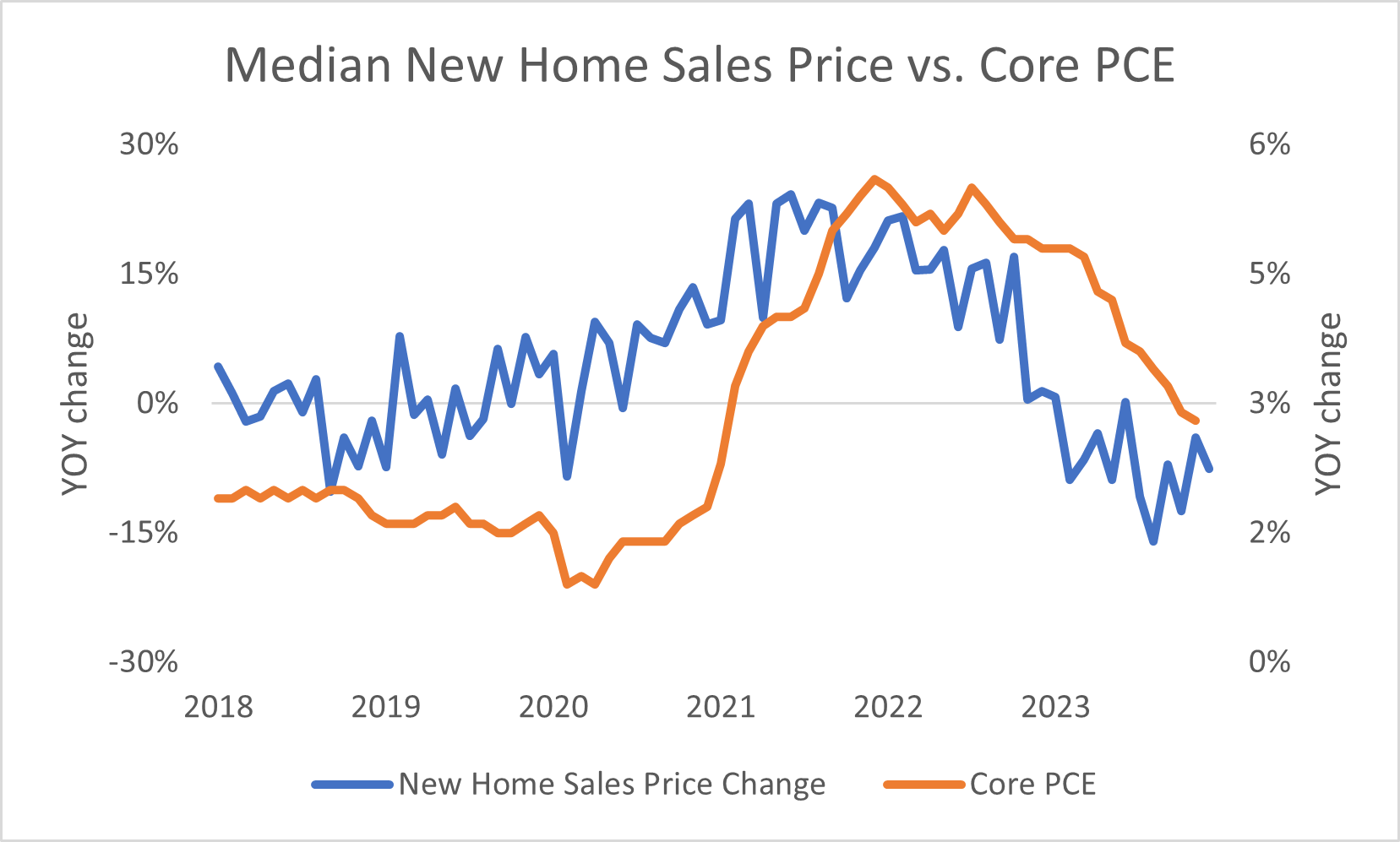

But the HPI numbers don’t paint the entire picture. They only take repeat sales into account. To truly understand what’s happening, we must also consider new home sales price figures…

According to the U.S. Census Bureau, the median price of a new single-family home fell to $400,500 in February compared to $414,900 in January. That was a drop of 7.6% on an annualized basis. In addition, it marked the tenth monthly contraction in new-home prices over the last year. In fact, the average price hasn’t been this low since July 2021.

Now, look at the relationship between the annualized change in new-home prices and core PCE…

Like the prior gauges, this data also tends to be a leading indicator of inflation. It peaked in August 2021 and PCE was slow to catch up. Yet, HPI been steadily dropping since. And based on the most recent numbers, core PCE has even more room to the downside.

So, if the Federal Reserve is going to be able to cut interest rates later this year, it needs to see inflation growth keep slowing. Based on the numbers we just observed, core PCE growth should keep easing. That means the central bank will have the cushion it needs to cut rates, even if inflation isn’t yet back to the 2% target. The change should lead to a steady rally in the S&P 500.

Five Stories Moving the Market:

Federal Reserve Governor Christopher Waller said there is no rush to lower interest rates, citing a strong economy, robust hiring, and slower progress in halting inflation growth – Federal Reserve. (Why you should care – Waller is one of the more hawkish central-bank policymakers)

Bank of Japan board members discussed the need to remain cautious at a policy meeting last week, where the bank ended its massive easing program with Japan’s first interest rate increase since 2007, according to a summary of opinions from the gathering – Bloomberg. (Why you should care – policymakers said the Japanese economy is strong enough to withstand a series of rapid rate hikes)

China’s protracted property downturn is eroding the balance sheets of the nation’s largest state banks as their bad loan ratios are creeping up; Industrial & Commercial Bank of China and competitor Bank of Communications said their non-performing loan ratios rose at the end of last year – Bloomberg. (Why you should care – balance sheet erosion could hurt banks’ ability to lend, curtailing economic growth in China)

Runaway prices at U.S. fast-food joints and restaurants have made people skittish down the income ladder and executives at chains including McDonald's and Wendy’s recently said they worry about losing business from those on the tightest budgets – Reuters. (Why you should care – lower- and middle-income households are increasingly seeing their discretionary spending shrink)

Disney ended a long-running legal battle with Florida Governor Ron DeSantis over control of the Orlando-area land that is home to its most important resort, ending a yearslong feud and handing the governor a political victory; the truce paves the way for Disney to expand its theme parks and resort properties in the state – WSJ. (Why you should care – the shift should help Disney in its efforts to improve profits and ward off activist investors from gaining control of board seats)

Economic Calendar:

Bank of Japan Summary of Opinions from March Meeting

Germany – Retail Sales for February (3 a.m.)

U.K. – GDP (Final) for 4Q (3 a.m.)

Initial Jobless Claims (8:30 a.m.)

Continuing Claims (8:30 a.m.)

GDP Annualized (Third Take) for 4Q (8:30 a.m.)

Pending Home Sales for February (10 a.m.)

Energy Information Administration Weekly Petroleum Inventories (10:30 a.m.)

Kansas City Fed Manufacturing Activity for March (11 a.m.)

ECB’s Villeroy Speaks (1:30 p.m.)

Fed's Balance Sheet Update (4:30 p.m.)