Slowing PCE Points to More Upside in Bonds

Slowing PCE Points to More Upside in Bonds

The bond-market rally is just getting started… because speculators are poorly positioned for slowing inflation growth and falling interest rates.

Since the Federal Reserve started raising interest rates in March 2022, the bond market has suffered. In January 2022, as the central bank was preparing for liftoff, the yield on 10-year U.S. Treasurys stood at 1.5%. By the peak reached this past October, that same yield had shot up to 5%.

As a result of the jump in rates, the Bloomberg U.S. Treasury Index lost 11.5% on a total return basis (dividends reinvested) or about 6.2% annualized. Now, that’s significant because since the index’s inception in 1973, it has averaged a 6.3% gain. In other words, it has underperformed by roughly 12.5% per year over the last two years.

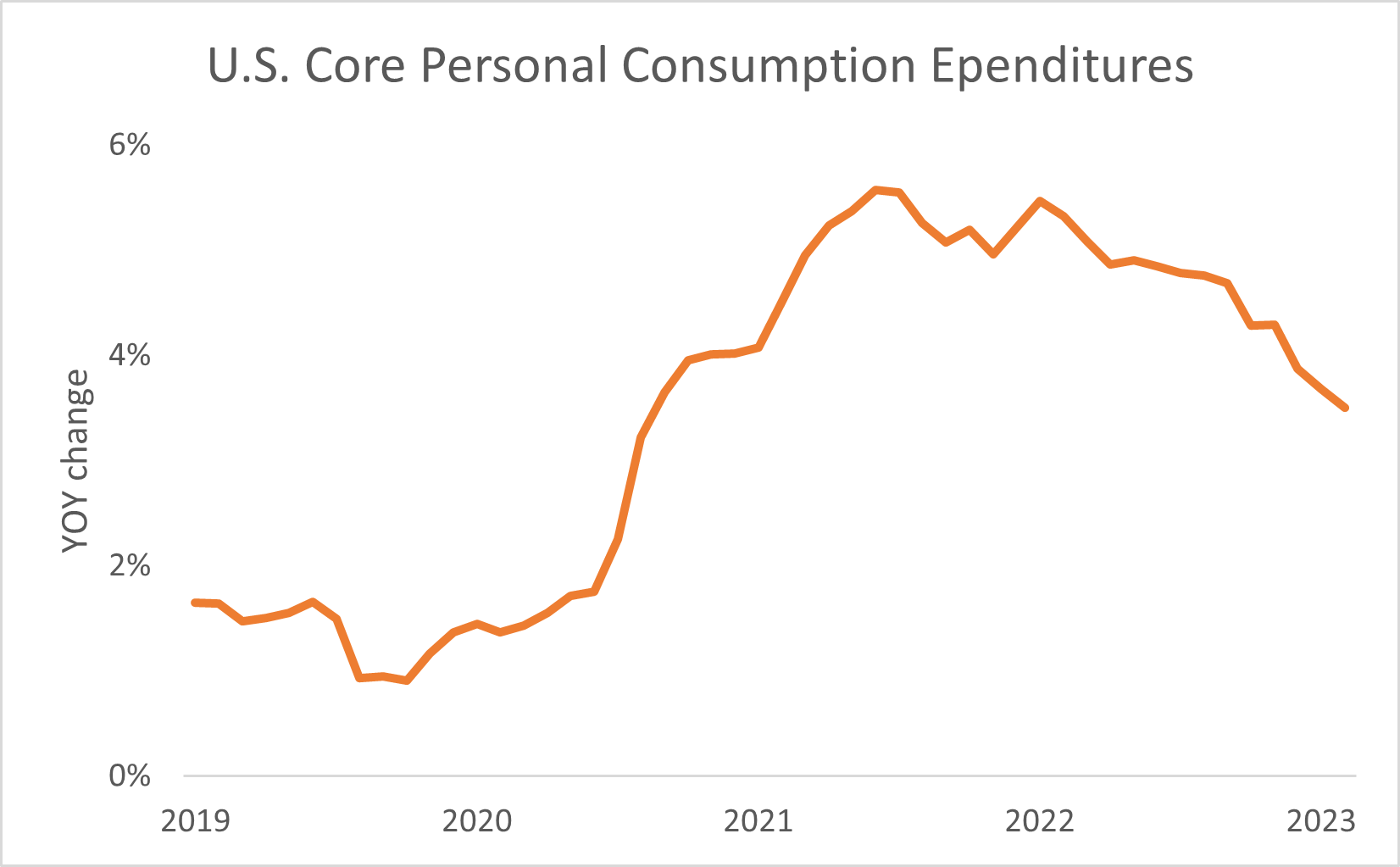

Up to this point, there’s been good reason for bond-market pessimism. After all, inflation growth has been high. Since peaking at 5.6% in February 2022, the Fed’s preferred inflation gauge, core personal consumption expenditures (“PCE”), has remained well above the stated 2% target, supporting rate hikes…

But the narrative is changing. The slowdown in inflation growth is gathering momentum. Yesterday, data from the Bureau of Economic Analysis (“BEA”) showed PCE decelerated in October to its lowest level since April 2021. And if the trend keeps up, it could give the Fed room to start cutting interest rates next year.

Based on the most recent speculator positioning, investors aren’t prepared for the change. They’re still massively short 10-year Treasury bonds. In other words, if price pressures keep easing, speculators would be forced to buy back those short positions, pushing yields down and bond prices higher.

But don’t take my word for it, let’s look at what the data’s telling us…

If we want to think about inflation growth, we must look at it through the eyes of the Fed. After all, it’s the institution that decides on where interest rates are headed. So, if we want to study the measure like our central bank does, we must watch core PCE.

PCE is like the U.S. Bureau of Labor Statistics’ better known Consumer Price Index (“CPI”). However, there’s one big difference… CPI tracks the change in out-of-pocket costs for all urban households while PCE calculates the price change of goods and services consumed by all households, including expenses on behalf of those individuals.

In other words, in the eyes of the Fed, PCE is more of an all-encompassing inflation gauge compared to CPI. But the central bank takes it one step further by looking at the core data. The change strips out the volatile price swings of food and gas. By doing so, the Fed thinks it gets a better feel for underlying price trends.

BEA released its October PCE data yesterday. The core number rose 0.2% month over month compared to the 0.3% growth in September. On an annualized basis, core PCE fell to 3.5% in October compared to 3.7% in the month prior.

I know that’s still above the Fed’s 2% target, but it’s a lot closer than the 5.6% peak back when rate hikes began. More importantly, the trend we’ve seen over the last six months points to inflation slowing even more.

Over the last year, core PCE has averaged 4.4% growth. That’s not what we want. Yet, for much of the time frame, consumers had lots of stimulus cash to spend. The Fed’s September Beige Book survey (anecdotal economic commentary) told us consumers are exhausting their savings. The survey for this month showed the economic outlook is deteriorating.

So, I wanted to look at the average core PCE growth over the last six months to get a better sense of the current trend. What I found was, the month-over-month increase had slowed to 0.2% compared to the almost 0.3% rate over that last year.

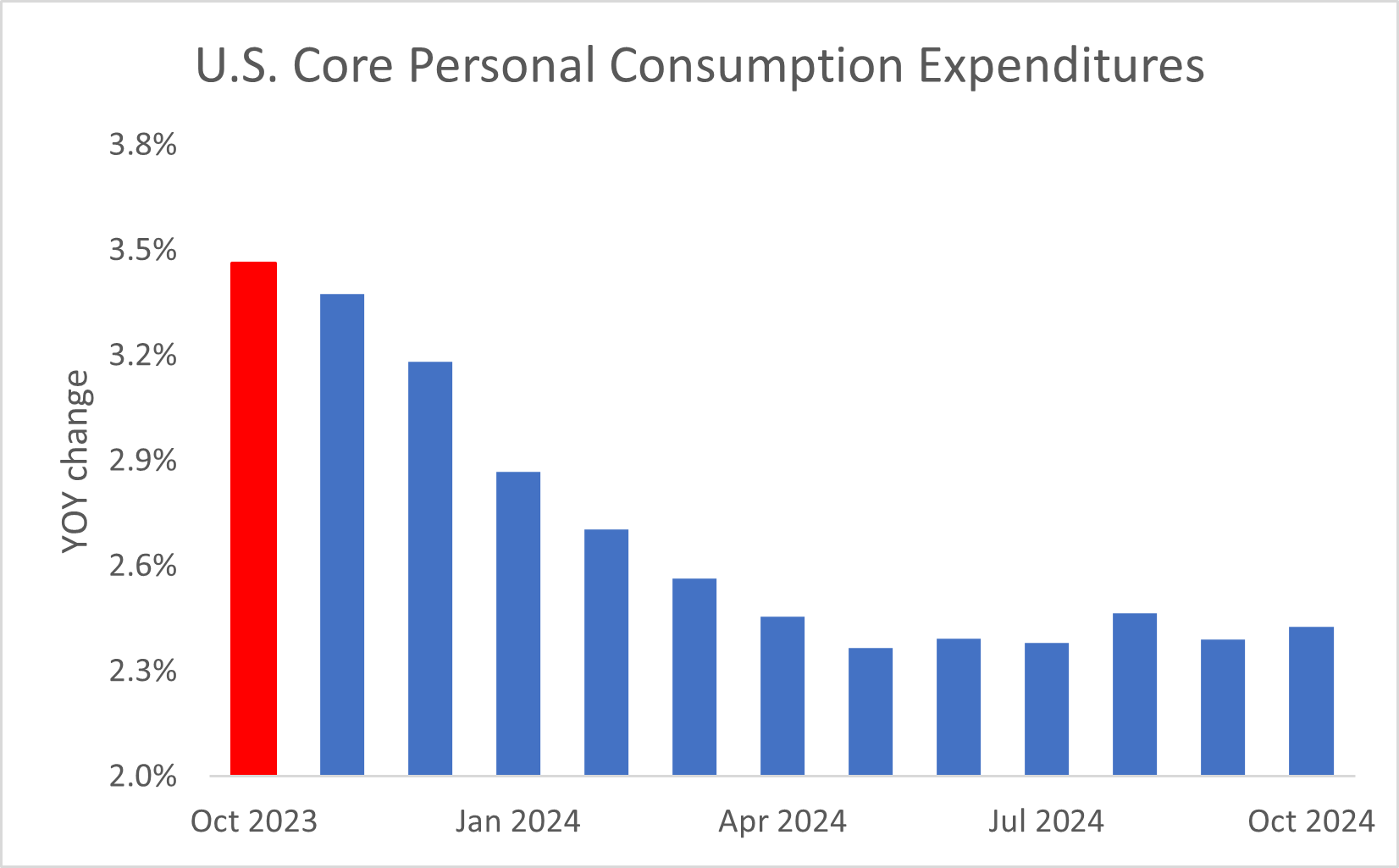

The change is important when we project the totals out over the next year. In the table below, I used the BEA’s core PCE index value and multiplied it by 0.2% to observe the annualized inflation growth potential through next October…

The red bar on the left represents 3.5% for this October. You’ll notice that moving forward, price pressures keep easing. In fact, by May, PCE will have dropped to 2.4% on a year-over-year basis. That’s close to the central bank’s 2% target.

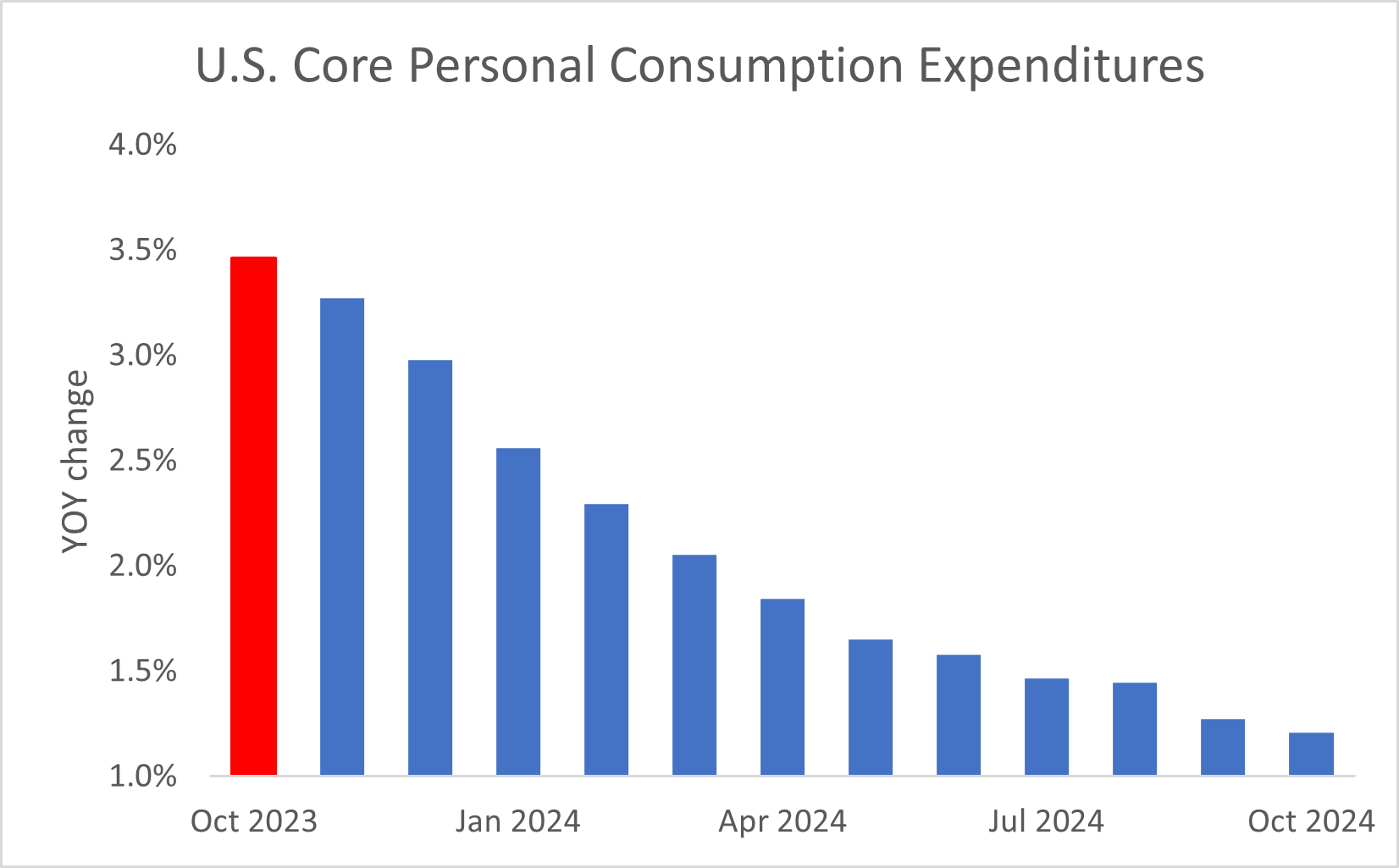

And, if economic activity continues to slow like the Fed’s Beige Book survey suggests, inflation could fall even more by this time next year. A drop to just a 0.1% monthly pace would see annualized growth tumble to just 1.2% a year from now…

The change would give the Fed the room it needs to start cutting interest rates once more. Chairman Jerome Powell has said it would begin easing policy again, once the annualized inflation numbers approached 2%.

But speculators aren’t well positioned for such an event…

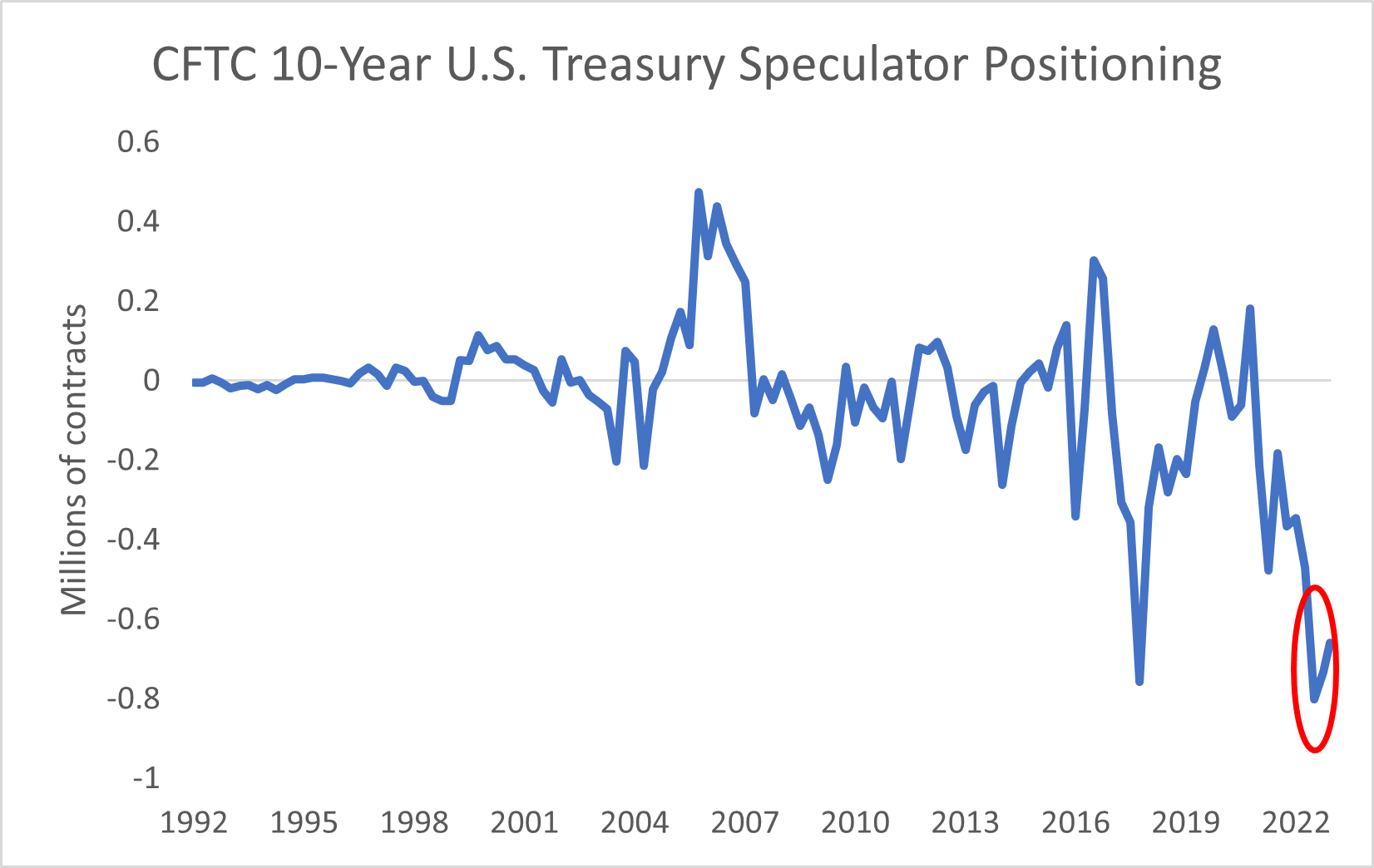

Every week, the Commodity Futures Trading Commission releases its Commitment of Traders report. It details the open interest of commercial and non-commercial entities in financial futures. Commercial positions are used by companies that have a business activity they want to hedge. In other words, they’re covered against whatever they’re buying or selling.

It’s the non-commercial positioning we want to watch. Those are speculators making one-way bets on whether an asset is going to rise or fall in price. Look at the positioning in 10-year Treasurys…

As you can see in the chart above, speculators have recently started buying back some of their shorts. That’s likely because Pershing Square founder Bill Ackman, a noted bear, has given up on his bet against Treasurys. However, you can see the short interest in the 10-year is still near record levels.

That’s important because of the inflation outlook. If the pace of inflation keeps slowing and the Fed starts easing monetary policy, bond yields will fall. That means prices will rally. That’s a problem if you’re short bonds… because you’re going to have to buy them back. The change will throw fuel on the fire causing bonds to rally even higher.

Since the start of the rate-hike cycle, the Fed has had one goal, kill the economy and slow inflation growth. Based the inflation numbers, a slowdown is happening. And the Beige Book commentary we mentioned is confirming the trend.

Board Member Christopher Waller, one of the biggest central-bank hawks (inclined to raise interest rates), recently signaled the Fed’s done. On Tuesday he said monetary policy is in a place that will bring inflation back to target. In other words, the next move is more likely to be a cut than another raise.

With the Fed not raising interest rates, institutional investors will race to lock in peak yields on an asset class that is considered one of the safest in the world. After all, 10-year U.S. Treasuries are yielding about 4.3% currently compared to the S&P 500 Index’s dividend yield of 1.4%.

For investors with a high risk tolerance and a long-term horizon, one way to invest is through purchasing the iShares 20+ Treasury Bond Fund (TLT). It seeks to track the performance of Treasury bonds with maturities of 20 years or more. If rates are headed lower (the bond market is predicting four to five cuts in 2024) the underlying price of bonds will jump, and longer-dated maturities should benefit the most.

This way, you can diversify your portfolio against an economic downturn and sleep soundly at night.

Five Stories Moving the Market:

The Caixin/S&P Global manufacturing purchasing managers' index (PMI) unexpectedly rose in November, in contrast to the official PMI which fell; but the two surveys suggest more stimulus will be needed to shore up economic growth – Reuters. (Why you should care – diminished factory activity in China implies global demand for goods made there remains weak)

The long-awaited U.S. economic slowdown has begun; signs are piling up — in recent data, in warnings from top retailers such as Walmart Inc. and in anecdotes from local businesses across the country — that after defying expectations all year and splurging over the summer, American households are starting to pull back – Bloomberg. (Why you should care – anecdotal information points to slowing domestic economic growth)

Bundesbank President Joachim Nagel said eurozone inflation is going in the right direction, and recent developments are encouraging, but a further rate hike cannot be taken off the table and cuts should not even be discussed – Reuters. (Why you should care – Nagel is one of the ECB’s biggest hawks and he’s signaling rate hikes are likely done)

Angola rejected a new output quota handed to it by OPEC and said it planned to breach it, a rare challenge to the cartel that heralds more infighting ahead – Bloomberg. (Why you should care – if one OPEC member breaches the pact, others are likely to follow, boosting supply)

The economy downshifted into fall after a fast-paced summer, as consumer spending rose 0.2% in October, down sharply from a 0.7% rise in September, the Commerce Department said Thursday, marking the slowest increase since May – WSJ. (Why you should care – a slowdown in consumer spending should weigh on inflation growth, eventually giving the Federal Reserve room to cut interest rates)

Economic Calendar:

China – Caixin China Manufacturing PMI for November

Japan – Company Profits, Capital Spending for 3Q

Japan – au Jibun Bank Japan Manufacturing PMI (Final) for November

Fed’s Barr Speaks (3 a.m.)

France - HCOB France Manufacturing PMI (Final) for November (3:50 a.m.)

Germany - HCOB Germany Manufacturing PMI (Final) for November (3:55 a.m.)

Eurozone - HCOB Eurozone Manufacturing PMI (Final) for November (4 a.m.)

U.K. - S&P Global/CIPS U.K. Manufacturing PMI (Final) for November (4:30 a.m.)

ECB’s Elderson Speaks (5 a.m.)

S&P Global U.S. Manufacturing PMI (Final) for November (9:45 a.m.)

Fed’s Goolsbee Speaks (10 a.m.)

ISM Manufacturing for November (10 a.m.)

Fed’s Powell Speaks (11 a.m.)

Baker Hughes Rig Count (1 p.m.)

Fed’s Cook Speaks (2 p.m.)

CFTC’s Commitment of Traders Report (3:30 p.m.)

Fed Releases Balance Sheet Updates on Commercial Banks (4:15 p.m.)

Fed Goes Into Media Blackout Ahead of Next Policy Meeting