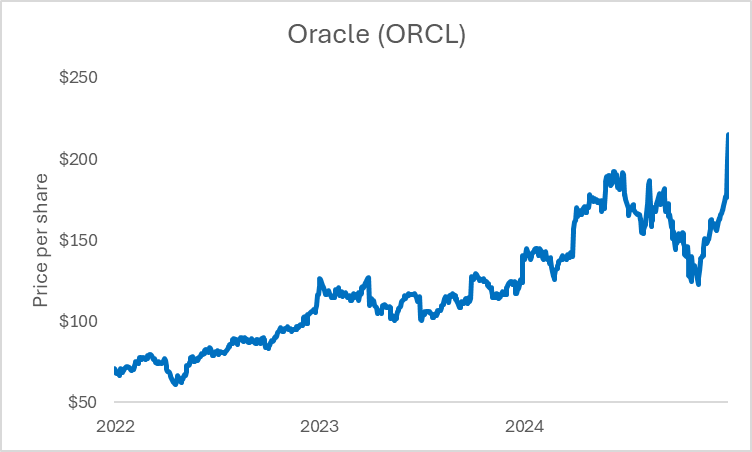

Oracle reported better-than-expected earnings and revenue.

The company talked up visibility through 2029.

Founder Larry Ellison said it can’t keep up with customer demand.

The boom in artificial intelligence (“AI”) demand is underappreciated…

Early in my finance career, I recognized a key skill that would enable me to better serve my clients: the ability to identify trends and habits. I knew that by understanding and remembering these patterns, I could help customers make smarter investment decisions. After all, times may change, but situations tend to repeat themselves. Recognizing how similar events have played out in the past allows us to separate the signal from the noise.

One trend I picked up on involves corporate earnings, particularly in the first quarter of the year. My analysis revealed that most companies try to avoid revising their financial figures after the first quarter. Because, they still have enough time to meet their annual goals. If they’re behind, they have time to catch up; if they’re ahead, they have a cushion in case of a slowdown.

But when a company adjusts annual guidance while reporting first-quarter results, it’s time to take notice.

Last week, such an event caught my attention. Enterprise software, cloud computing, and database management system provider Oracle (ORCL) reported better-than-expected first-quarter earnings and revenue. Not only that, but CEO Safra Catz raised FY2026 revenue guidance by 16% compared to the figure endorsed at the end of last year—just three months prior.

Catz attributed the change to surging AI demand. The shift should support an improved outlook for technology infrastructure companies—specifically, those building the semiconductors and networking equipment that power data centers. This momentum is likely to drive technology stocks higher, further strengthening tech-heavy indexes like the S&P 500 and Nasdaq Composite

But don’t take my word for it, let’s look at what Oracle had to say…

Catz endorsed total cloud revenue growth of more than 40% for FY2026 compared to 24% in FY2025. She stated annual cloud infrastructure revenue growth should exceed 70%, compared to 51% in 2025. She said the company is increasingly confident about meeting and exceeding its 2027 and 2028 targets. The change was driven by improved visibility into business demand.

Chairman of the Board Larry Ellison said the company will be the world’s top builder and operator of cloud infrastructure data centers. He emphasized that Oracle’s applications can integrate with all major large language models. This allows customers to train AI on their own proprietary data without sharing it publicly. He stated that this capability isn’t currently offered by competitors, strengthening Oracle’s value proposition for clients.

The company also highlighted the surging demand for multi-cloud solutions, which involve using multiple cloud computing and storage services from different providers in a single, distributed architecture. This strategy enables organizations to leverage the best features of various cloud platforms rather than relying on a single vendor. The Oracle database’s ability to interoperate with other platforms is a key driver of demand.

Further emphasizing customer interest, Catz detailed that current demand is outstripping Oracle’s available capacity. She said the company is either turning away customers or scheduling them into the future. The CEO remarked that Oracle has never faced such a situation in its history, describing the numbers as “enormous.” She also noted that the ramp-up of the Stargate AI Project—the next generation of U.S. AI infrastructure—will feed into this cycle. If the project delivers on its promises, growth will exceed even the latest expectations.

One potential concern raised by critics is Oracle’s capital expenditure forecast. However, when examined closely, the increase from $20 billion to $25 billion for FY2026 is a positive. Catz clarified that the number is based on build-out costs to meet specific customer demand, meaning the company does not order components or build infrastructure unless required by clients. She further indicated capital expenditures could rise even higher. Ellison said a customer had expressed interest in buying all worldwide capacity Oracle can build.

Now, while Amazon’s AWS, Microsoft’s Azure, and Alphabet’s Google Cloud dominate the market, Oracle’s carving out a niche with its expanding AI capabilities across cloud infrastructure, enterprise applications, and data science tools.

Oracle’s multicloud strategy enables its AI products to integrate with Azure, Google Cloud, and AWS. The company has forged partnerships that allow customers to run Oracle Database and AI workloads on other cloud platforms. These collaborations have enhanced accessibility, further boosting demand for Oracle’s services.

So, when a company with Oracle’s scale and visibility raises or lowers its demand guidance, it’s worth paying attention. Based on the commentary we just looked at, customers are asking for more data center capacity—not less. That should underpin steady demand for companies that make AI infrastructure products like semiconductors - Nvidia (NVDA), Broadcom (AVGO), and Advanced Micro (AMD) - and networking hardware - Cisco Systems (CSCO) and Arista Networks (ANET). The shift should support a long-term steady rally in the S&P 500 and Nasdaq Composite.

Keep reading with a 7-day free trial

Subscribe to The Intrepid Investor's Guidebook to keep reading this post and get 7 days of free access to the full post archives.