The End of Rate Hikes Is a Tailwind for Stocks

Last week was a turning point for the stock and bond markets… because the Federal Reserve’s tone on monetary policy changed.

Since the central bank began raising interest rates in March 2022, there have been several important shifts. The first came in June 2022 when Chairman Jerome Powell said it would raise rates by 75 basis points to 1.75% because inflation growth was too hot. He stated rate hikes must remain aggressive moving forward.

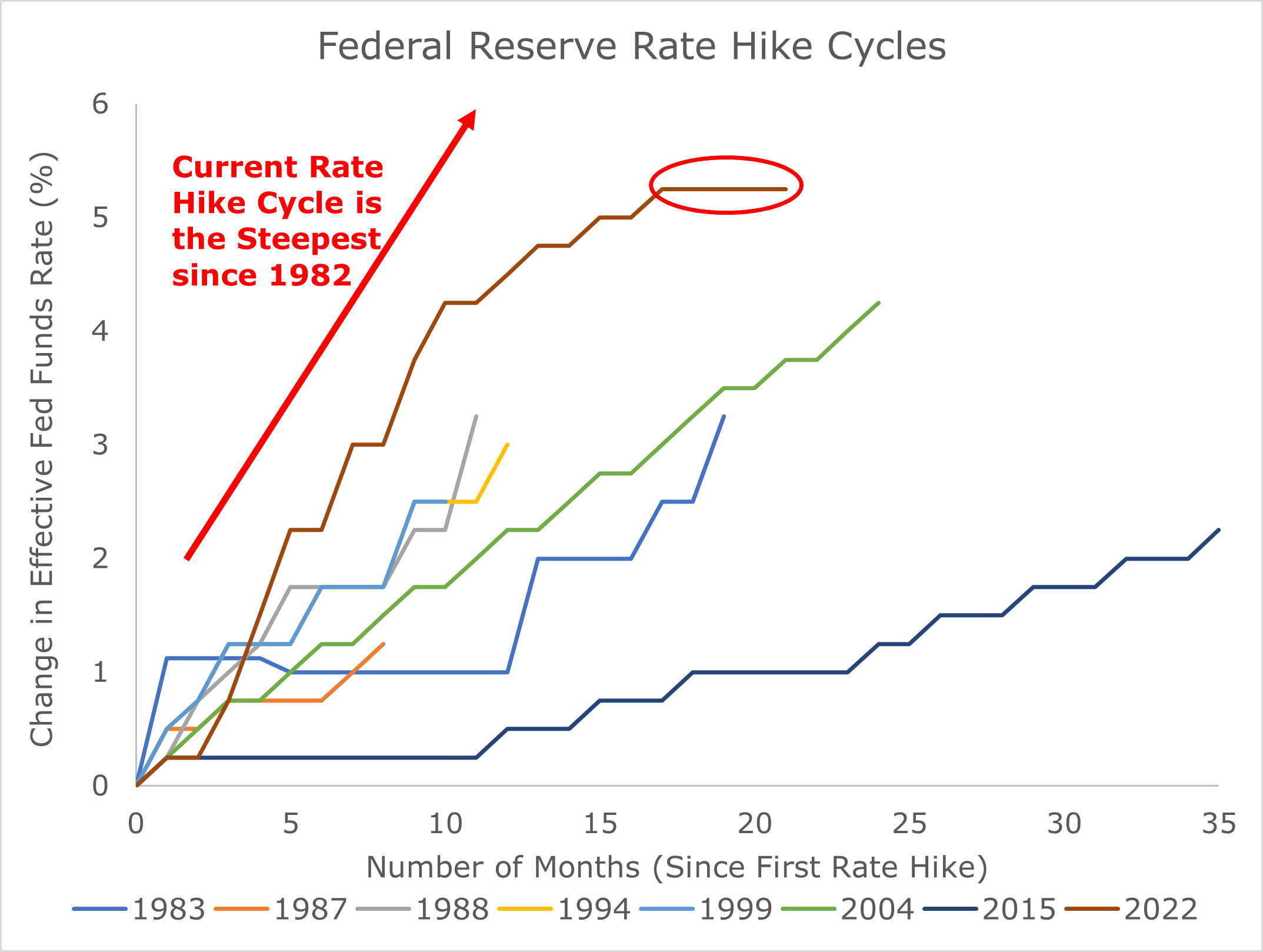

The next big shift came in June of this year. After raising interest rates from 0.25% to 5.25% over ten consecutive meetings, the Fed paused. It would make one more increase in July, appearing to complete the fastest rate hike cycle since 1982…

But after that last rate hike, the Fed kept investors guessing about the next move. Members of the rate-setting Federal Open Market Committee (“FOMC”) expressed continued concern about prices while saying more rate hikes were necessary to bring inflation growth back to the 2% target.

That was until last week… two important policymakers changed their interest-rate tone. After not having raised rates for more than four months (and two FOMC meetings), they expressed confidence monetary policy may finally be at the right level.

The change means the Fed’s next move is more likely to be a rate cut than a hike. And that should underpin a steady rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data tells us…

On Tuesday, Board Member Christopher Waller spoke at the American Enterprise Institute. The discussion focused on the economy and the challenges facing the Fed. The speech was important because Waller has been one of the biggest hawks (inclined to raise rates) and most prescient members of the FOMC.

Now, in an October speech, Waller said something had to give in the economy. The former St. Louis Fed research chief noted the rate of economic growth, based on third-quarter output of 5.2%, didn’t fit with the amount of rate increases since March 2022. He said that either the economy needed to slow, or the central bank would be forced to raise rates even more.

Last week, Waller said the economy is starting to moderate. He said economic data point to output slowing in the fourth quarter. The policymaker also noted inflation metrics show it’s falling once more. But the changes have increased his conviction that interest rates are at the right level to bring inflation back to the central bank’s 2% target. In other words, Waller thinks the Fed could be done raising rates.

On Friday, Powell spoke about the economy during a fireside chat at Spelman College. He said the job market is beginning to see more stability. He noted that the demand for workers greatly exceeded supply during the pandemic, in turn driving inflation. But now, the dynamic is starting to come back into balance where supply is rising as the need for workers eases.

The Fed chair then discussed the recent slowdown in inflation. He said over the last six months, core prices grew at 2.5%, close to the central bank’s 2% target. He noted rate hikes are having the desired effect of boosting the supply of available goods because people are spending less. As a result, it’s slowing economic growth and stabilizing prices.

Then Powell struck a tone like Waller. He said that while it’s too soon to say the Fed’s done raising rates, he believes policy remains constrictive, demand will fall, and the economy will slow. He believes that “policy is on the right path to bring inflation back to 2%.” In other words, the Fed chairman thinks it could be done raising rates.

Ever since the central bank last raised rates in July, investors have wondered if it was finished. After all, the Fed is never going to tell you when it’s done. Those comments would encourage risk taking and speculation, potentially creating more wealth, spending, and inflation.

But the comments from Powell and Waller last week may be as close as we’re going to get. Each signaled inflation is on a path to their target. And they believe the economy is finally slowing… something they’ve sought from the start.

And the end to the rate hike cycle has historically been a tailwind for stock investors…

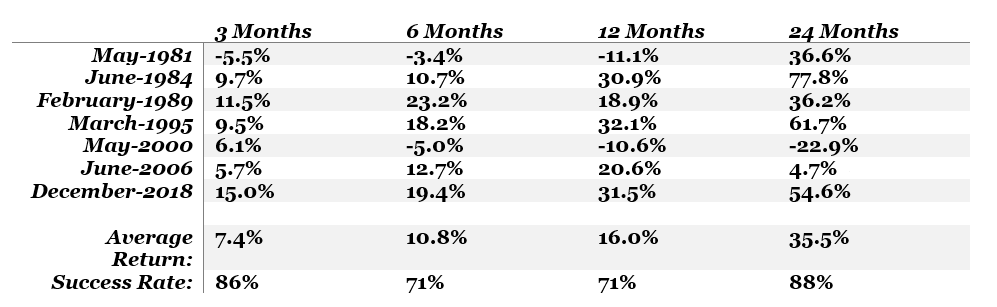

As I said at the start, this has been the fastest pace of rate increases since the early 1980’s. That’s because inflation growth hit the highest level since the early ‘80’s in June 2022. So, I went back and looked at the S&P 500’s performance on a total return basis (dividends reinvested) each time the Fed stopped raising rates. I used 3-, 6-, 12-, and 24-month time frames from the end of each month. The results were astounding…

As you can see in the table above, there have been nine times between 1981 and this year when the Fed has stopped raising rates. In the first three months, the average return is 7.4% and a positive result has happened 86% of the time. Yet, this year, the S&P 500 only gained 1% in the three months after the last rate hike in July. That tells me there’s some catching up to do.

However, what’s more important is the long-term gains. Look at the 12- and 24-month results. Those returns are far greater than the 9.5% average gain for the S&P 500 since 1928.

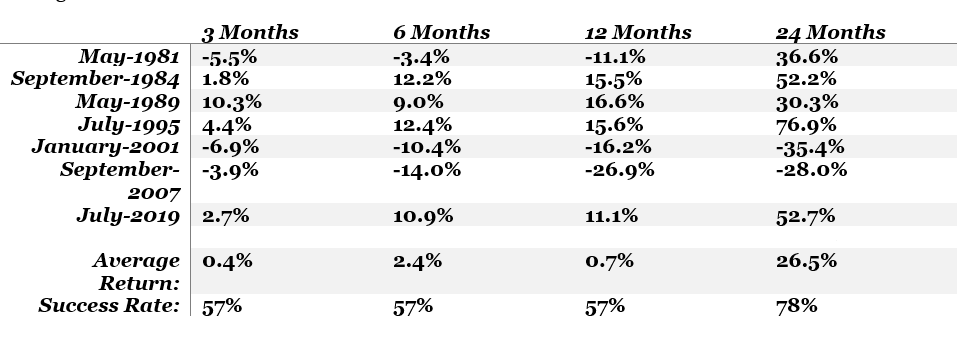

But it gets even more interesting when we look at the returns after the Fed starts cutting rates. I used the same game plan and looked at the S&P 500’s return from the end of each month central bank started easing...

Notice the difference in returns from when the central bank stops raising rates to when it starts cutting. Investors still make out well over the long term, but the short-term outcomes are far less beneficial. That’s likely because by the time the central bank’s about to ease, most investors have already realized it and jumped in. And once the economy gets going again in 12 months, stocks start to take off.

So, like I said, the Fed’s never going to tell us it’s done, but the commentary last week leans in that direction. And if that’s the case, it should spell good days ahead for patient, long-term investors.

If you want to invest in this trend, consider buying shares of the SPDR S&P 500 ETF (SPY). It tracks the S&P 500 by investing in the shares of the companies in the index. It pays dividends on a quarterly basis. And it trades just over 82 million shares a day, so it should be easy to buy and sell.

Five Stories Moving the Market:

Economists say goods prices likely have further to fall, which will ease inflation’s return to the Federal Reserve’s 2% target, perhaps as early as the second half of next year – WSJ. (Why You should care – falling prices would ease inflation, giving the Federal Reserve room to cut interest rates)

European Central Bank Vice President Luis de Guindos said the process of disinflation appears to be strong, and the current level of interest rates should be high enough to bring inflation growth back to the 2% target, but it’s still too early to declare victory – Bloomberg. (Why you should care – ECB officials are increasingly positive about the drop in inflation and the lack of need for more rate hikes)

Federal Reserve officials are increasingly confident that they don’t need to keep raising interest rates to defeat inflation; but they aren’t satisfied enough to declare an end to hikes—let alone to start a discussion about lowering rates – WSJ. (Why you should care – this should drive yields even lower, rallying bonds and precious metals)

Alternative-asset manager KKR’s infrastructure group plans to invest at least half its capital, between $1 billion and $5 billion, into digitalization and decarbonization opportunities next year, in addition to pursuing complex carve-outs from companies – Bloomberg. (Why you should care – the company feels frozen credit markets have opened up attractive valuation gaps)

U.S. manufacturing remained subdued in November, with factory employment declining further as hiring slowed and layoffs increased, more evidence that the economy was losing momentum after robust growth last quarter – Reuters. (Why you should care – slowing economic growth should weigh on inflation, ultimately giving the Fed room to lower interest rates)

Economic Calendar:

Germany – Trade Balance (Imports/Exports) for October (2 a.m.)

Riksbank Meeting Minutes (3:30 a.m.)

ECB’s de Guindos Speaks (3:45 a.m.)

Eurozone – Sentix Investor Confidence for December (4:30 a.m.)

BOE’s Dhingra Speaks (6:30 a.m.)

ECB’s Lagarde Speaks (9 a.m.)

Factory Orders for October (10 a.m.)

Treasury Auctions $143 Billion in 13- and 26-Week Bills