The Fed Has Plenty of Cushion Before Considering Rate Hikes

Don’t get sucked into the latest stock-market drama…

Investing often reminds me of sports. Because, on the field of battle, there’s always an opponent. Each side is always trying to triumph over the other by outworking, outplaying, and outscoring. And before confronting one another in a contest, they hone their craft through practice.

Now we might be used to our favorite high school, college, or professional sports teams doing this. But investors aren’t much different. You see, they’re constantly looking at data to determine which companies and economic environments are the best for buying, selling, or shorting stocks and bonds. But, instead of the Ravens playing the Giants, the gladiators in the arena are the bulls and the bears.

Over the last few weeks, the bears have dominated the stock- and bond-market narrative. They’re playing on fears about stronger-than-anticipated economic growth. The naysayers are telling anyone that will listen that the recent string of positive data means the Federal Reserve will have to hike interest rates before the year’s over.

The boobirds’ case was buoyed last week by two central-bank policymakers. New York Fed President John Williams and Atlanta Fed President Raphael Bostic, both said it would raise rates once more if the data called for such a move. That caused the S&P 500 Index to lose 3.5% last week, bring the total loss for April to 5.3%.

But the part no one talked about was their outlook for current policy. Both Williams and Bostic said they still think interest rates are in a good place to bring inflation growth back under control… it just might take a bit longer than previously expected. And they still both expect rate cuts to start later this year.

Now, there’s no guarantee rate cuts will happen. But even when we look at recent “hot” inflation data, the central bank should still have plenty of interest-rate cushion before it even needs to consider a rate hike. That should underpin a steady rally in the S&P 500.

But don’t take my word for it, let’s look at what the data tells us…

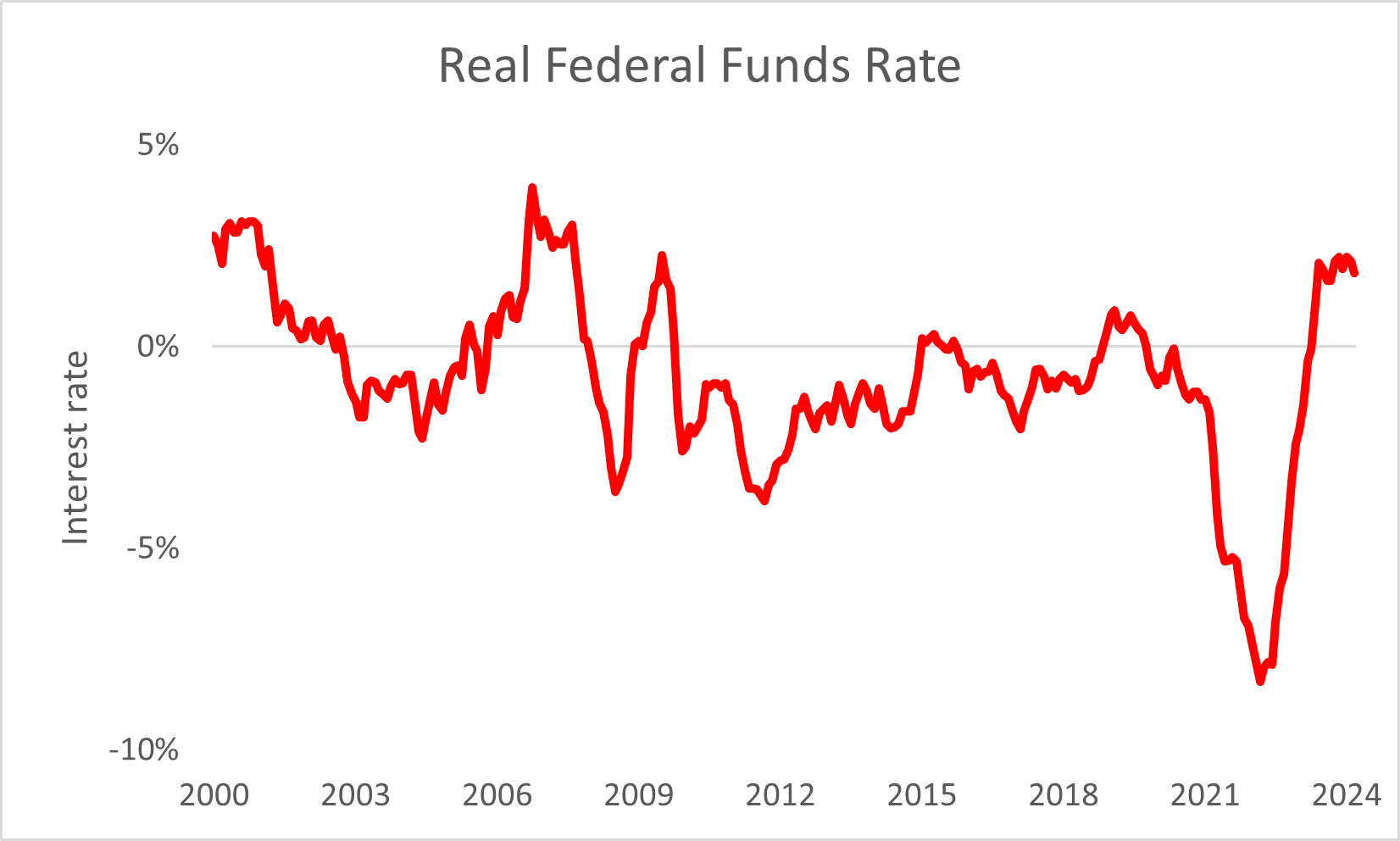

One of the best ways to look at Fed policy is through the real rate of interest. We can do this by looking at the pace of annualized inflation growth compared to the effective fund rate (the rate at which banks lend each other money overnight).

We want to find out if the number is positive or negative. Because, if real rates are positive, they’re weighing on inflation, but if they’re negative then they’re supporting price growth. That makes the difference between a central bank that needs to raise rates compared to one that has room to cut.

Now, even though core Personal Consumption Expenditures (“PCE”) are the central bank’s preferred inflation gauge, Wall Street typically derives the real rate of interest through the use of consumer price index (“CPI”) growth. And based on the current math, the number sits at 1.8%...

As you can see in the chart above, the real rate of interest got as low as -8.3% back in March 2022, just before the Fed started a series of rapid rate hikes. And then, after getting the number back to 2% by June of 2023, our central bank finally had the room it sought to stop raising.

But as we said at the start, the narrative around interest rate policy is starting to shift, At the start of this year, Wall Street was predicting seven rate cuts. Now, that was way ahead of the there that policy makers endorsed. And recently, after Chairman Jerome Powell said the rate-cut cycle has been delayed, expectations dropped to just two.

Yet as the policy shift has taken place, the rate-hike narrative has slowly crept in, spooking investors. But the data outlook paints a different story…

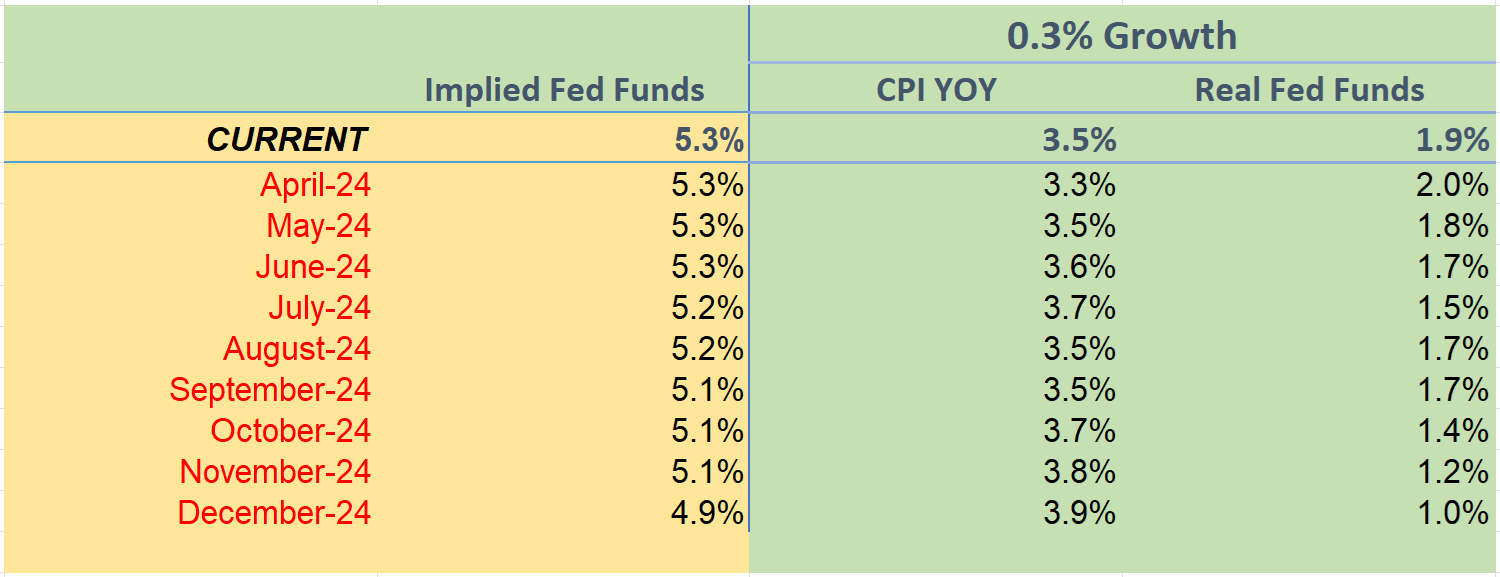

To say exactly what spending might be over the next year is impossible. But we can take the average monthly inflation growth trends we’ve experienced in the recent past, to project what the annualized numbers might look like going forward. Then we can subtract those numbers from the expected path of interest rates (which include rate cuts) to get an idea of the real rate of interest.

Now based on the last 6-, 12-, and 24-month periods, the average rate of monthly CPI growth has been 0.3%. Doing the math, here’s what real rate of interest will look like moving forward…

You’ll notice that by the end of this year, real interest rates will still be 1%, meaning they’re weighing on inflation growth.

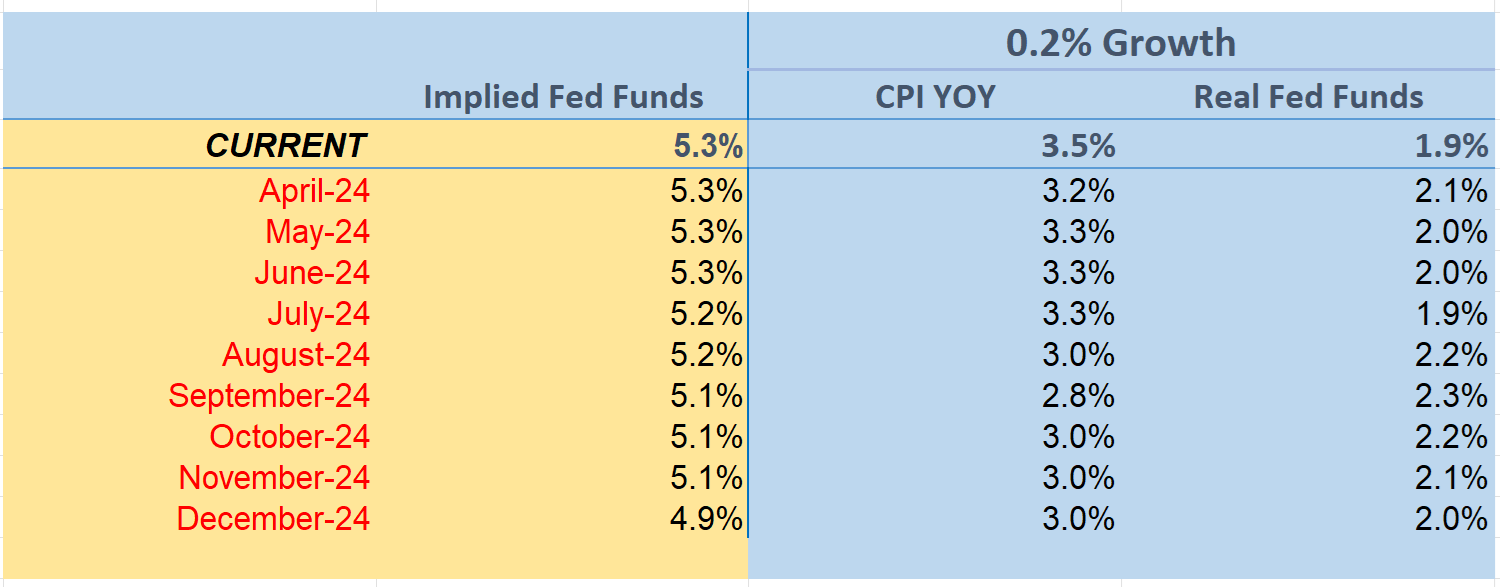

And what if the monthly average slows to 0.2%? Well, in that case, real interest rates would be closer to 2%...

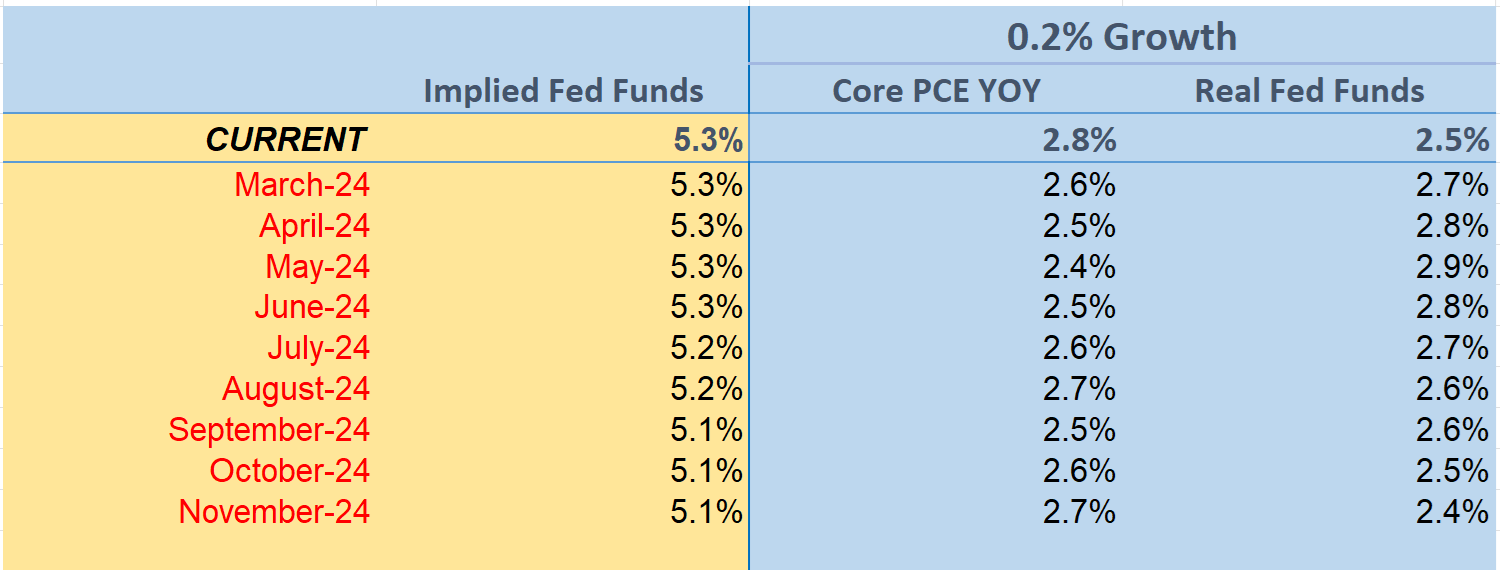

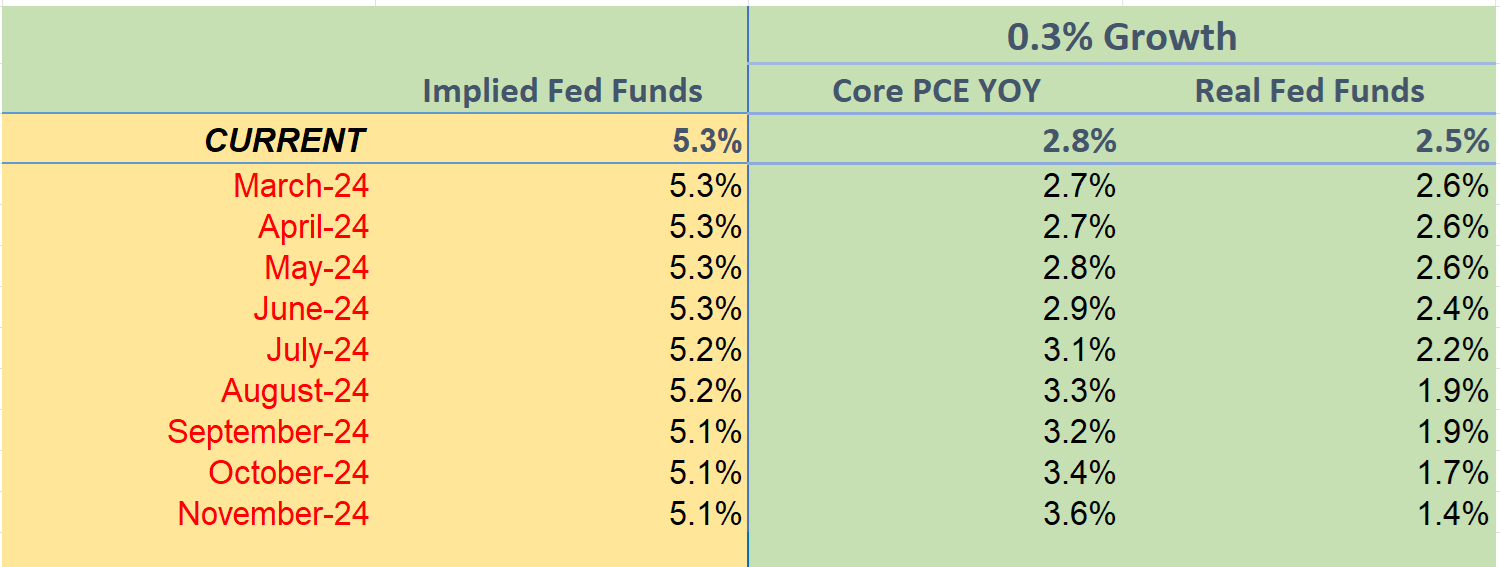

When we look at the central bank’s preferred inflation gauge, the real rate of interest cushion looks even greater.

Over the last 6- and 12-month periods, core PCE has averaged a 0.2% growth rate. If we project those type of price increases moving forward, real interest rates are still at 2.4% by the end of the year…

And if we use the 0.3% core PCE growth rate from the last two years, real interest rates are still at 1.4% by the end of this year…

In other words, none of these scenarios point to the need for the Fed to alter course and start raising interest rates once more. In fact, the only scenario that would precipitate that need is inflation growth averaging 0.5% per month moving forward.

So, like I said at the start, gladiators are always trying to hone their skills before entering the arena of battle. Right now, the stock-market bears have the advantage. But, based on the game plan, they’re bound to stumble. Because, the Fed might be in no rush to cut rates, but based on the numbers we just surveyed above, there’s certainly no need to increase borrowing costs once more.

And when the battle plans are exposed, the shorts will have to start covering their bets once more. That should lead to a steady rally in the S&P 500.

Five Stories Moving the Market:

Banks in China maintained their benchmark lending rates, following the Chinese central bank’s recent decision to stand pat on monetary policy – Bloomberg. (Why you should care – the lack of policy stimulus is likely a signal that Beijing isn’t convinced of a growth turnaround)

French central bank chief Francois Villeroy de Galhau said tension in the Middle East is unlikely to drive up energy prices and should not affect the European Central Bank's plans to start cutting interest rates in June; he added that additional cuts should follow in a “pragmatic” fashion – Reuters. (Why you should care – rate cuts by the ECB could provide the Fed with the cushion it needs to start doing the same)

Bank of Canada Governor Tiff Macklem says inflation is getting “closer to normal” and officials will monitor incoming data to check whether the downward momentum can be maintained – WSJ. (Why you should care – inflation growth returning to normal would ease the monetary policy outlook for global central banks)

Federal Reserve Bank of Richmond President Tom Barkin said demand is strong but the U.S. economy isn’t showing signs of running too hot; he added the Fed has no need to adopt a hiking bias, without these signs of a “durable” trend towards overheating – Bloomberg. (Why you should care – Barkin is noting economic demand would really have to pick up for the central bank to start raising rates again)

Bank of England Deputy Governor Dave Ramsden said the risk of British inflation getting stuck too high had receded and it might prove weaker than the BoE's most recent forecasts; he stated inflation could remain around the BoE's 2% target for the next three years - rather than rise higher later this year as the central bank forecast in February – Reuters. (Why you should care – Ramsden’s comments mean there’s potential the BOE could ease monetary policy sooner than later)

Economic Calendar:

China – PBOC Loan Prime Rate

Eurozone – Eurogroup Meetings (6 a.m.)

Eurozone – Consumer Confidence for April (10 a.m.)

ECB’s Lagarde Speaks (11:30 a.m.)

Treasury Auctions $70 Billion in 13-Week Bills (11:30 a.m.)

Treasury Auctions $70 Billion in 26-Week Bills (11:30 a.m.)