The Fed Will Be Forced to Boost Liquidity, Rallying Stocks

The Fed Will Be Forced to Boost Liquidity, Rallying Stocks

The Federal Reserve will soon be forced to ease policy once more…

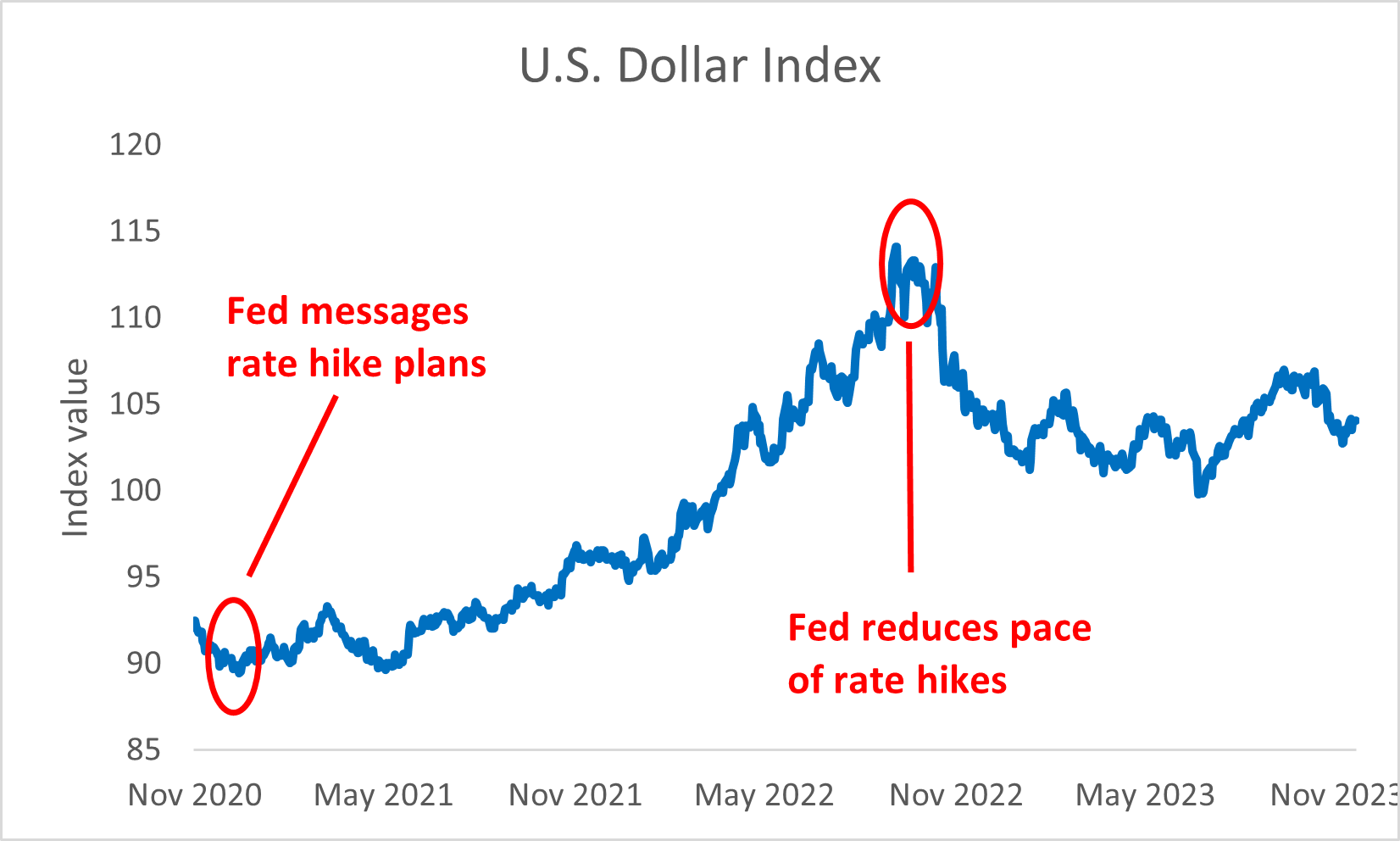

Since March 2022, our central bank has pulled every lever possible to kill economic growth. It has employed the use of early messaging about future monetary-policy decisions, aggressive interest-rate hikes, and shrinking the size of its balance sheet (quantitative tightening), as the primary tools to drive up the cost of borrowing money.

In the process, the Fed effectively drove up the yield on the dollar. After all, interest rates jumped from 0.1% to 5.3%. So, in the eyes of Wall Street, the change increased the dollar’s appeal compared to the currencies of other countries. Financial institutions increasingly hoarded the dollar, hoping to gain from the jump in value.

But there’s an additional reason why money managers increased their cash piles. With the economy performing well due to all the COVID stimulus pumped into the system, the Fed was uncertain of how high interest rates must rise to cool inflation growth. So, Wall Street didn’t want to invest in Treasury bonds too soon. After all, rising rates meant bond prices would fall, leading to markdowns and losses.

Instead, institutional investors found a better place to park their greenbacks… overnight lending markets. If rates kept going up, money managers could reap the benefits as the cost to borrow funds overnight did the same. That way, when those investors felt like rates had risen enough, they could use their cash piles to buy U.S. Treasury bonds and lock in peak yields.

Lately, signs point to slowing economic growth…

The Atlanta Fed’s fourth quarter GDPNow forecast shows domestic output will slow to 1.2% compared to a late October estimate of 2.3% and third-quarter growth of 5.2%. In addition, the Cleveland Fed’s Inflation NowCast expects the November consumer price Index (“CPI”) to contract on a month-over-month basis for the first time since May 2020.

That presents a new problem for the Fed. Because if those indicators on inflation and GDP growth are right, there’s no longer a need for additional rate hikes. The change means we’ve likely hit peak interest rates. And based on what I’m seeing, financial institutions feel the same. They’re taking money out of overnight lending markets and pouring it back into bonds, reducing financial-system liquidity.

The dynamic means the Fed will be forced to take steps, like ending its balance sheet runoff and lowering interest rates, to boost the amount of money available in the financial system. That will underpin a steady long-term rally in the S&P 500 Index.

But don’t take my word for it, let’s look at what the data’s telling us…

The central bank’s primary tool for setting interest rates is the federal funds target. It’s meant to be used as a guide for banks borrowing funds from one another overnight.

You see, due to the daily swings of deposits and withdrawals at banks, their cash balances are in constant flux. Sometimes, the changes cause a lender’s reserves to drop below the federally required minimum to ensure solvency and stability. As a result, a bank is forced to borrow funds in the overnight market.

Consequently, the cost to borrow funds in the overnight markets is an important vehicle for communicating monetary policy. Because, if a bank must pay that much to borrow money, it will charge even more to lend.

Now, if the overnight rate stays in line with the fed funds target, it’s a sign liquidity in the financial system is ample. But, if the overnight rate shoots above the fed funds target, it’s a sign the financial system is starved for funds.

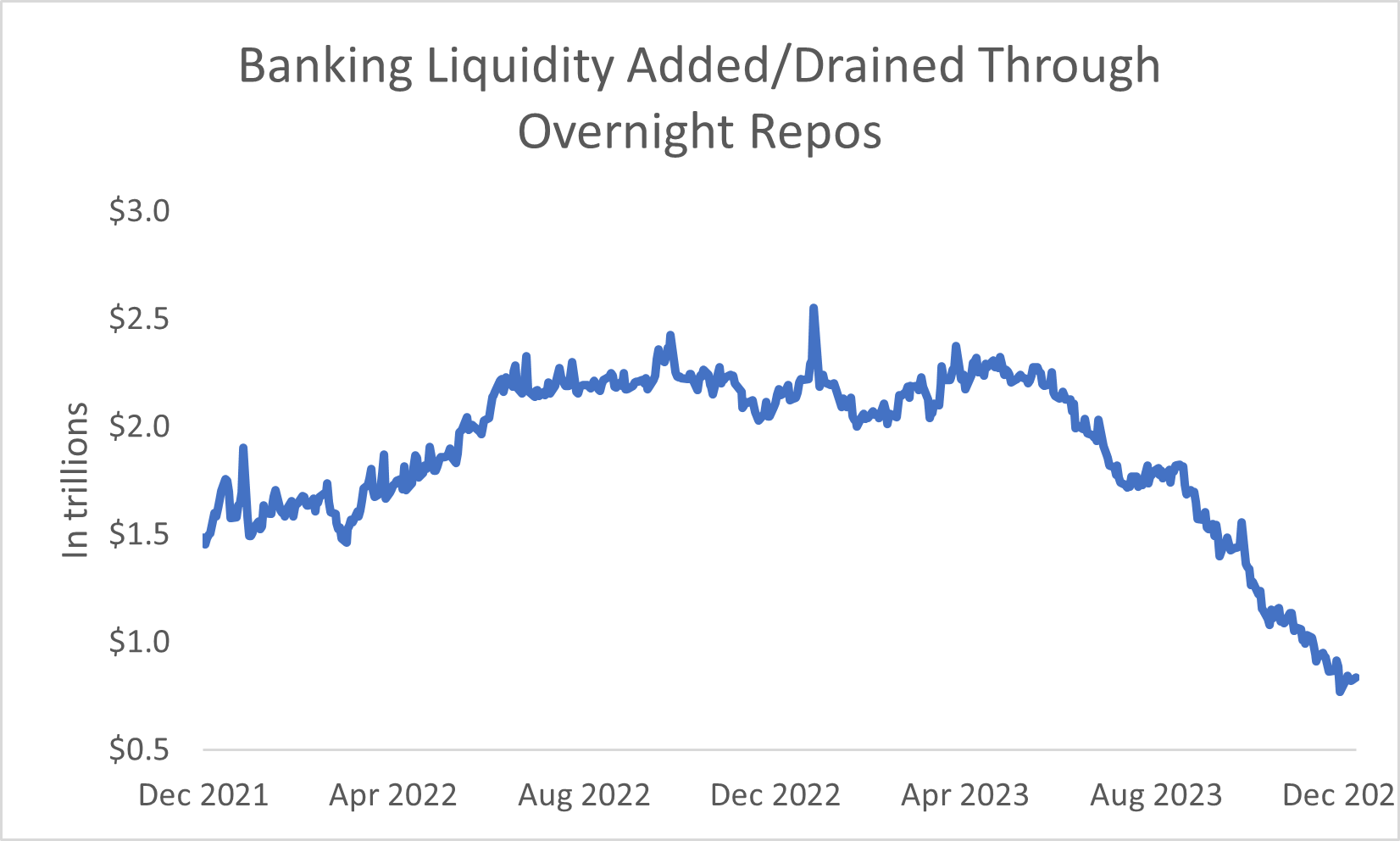

Shrinking Overnight Funds

We can see this through the New York Fed’s gauge of banking liquidity added and drained via the overnight repurchase market. Repos are agreements where one financial institution agrees to buy securities from another, selling them back at a later date and at a higher price, making a return. In this case, the transactions are overnight.

By doing this, the lending institution is allowing a bank to meet its required reserve balance, investing its cash in a low-risk manner, and keeping borrowing costs stable.

Look at the data from the end of 2021 (when the Fed began telling investors it would soon start raising interest rates) through yesterday (when it looks like rate hikes are done) …

What you ‘ll notice on the left side of the chart, is that in December 2021, roughly $1.5 trillion in funds was available in the overnight lending market. Yet, as we move into 2022, the number keeps rising.

The driver is the rate-hike uncertainty we mentioned at the start. Institutions aren’t sure about how high the fed funds target will go. Buying bonds out of the gate is a losing investment if rates keep going up. Because the underlying value will plummet. So, as the Fed gets more aggressive, and rates keep going up, more money is parked in the overnight markets. But notice the amount of funds peaked at roughly $2.6 trillion late last year. It then starts to fall…

After having raised rates by 75 basis points at three consecutive Federal Open Market Committee (“FOMC”) meetings, the central bank decided it could back off. It increased the fed funds rate by 50 basis points in December 2022 and then by 25 basis points in January 2023. That told investors that interest rates were close to the peak.

By May of this year, the fed funds rate had reached 5.13%. Then, in June, the FOMC paused rate hikes for the first time since March 2022. At that point, the amount of overnight liquidity was $2.1 trillion. By the time the last rate hike was made in July, available funds had dropped to $1.7 trillion.

Now, with policymakers signaling peak rates, the available liquidity total is down to $840 billion. That’s one-third of the 2022 crest.

The Balance Sheet Roll Off’s End

Financial institutions increasingly think the next central-bank decision is a rate cut. They don’t want to miss out on peak rates in corporate or government bonds. So, they’re removing money from the overnight lending and investing elsewhere.

At the start of December, the Secured Overnight Financing Rate (“SOFR”) jumped to 5.4%. That compares to the implied rate of 5.33% based on the fed funds target. The change may not seem like much, but it’s causing concern in the overnight markets. Because, if there’s a year-end demand increase for funds, it could drive borrowing costs higher. And it echoes what happened in 2019…

In September of that year, overnight cash demand surged due to quarterly taxes and concerns about a new virus in China. Available liquidity couldn’t meet demand. Lenders saw an opportunity to profit. The overnight rate shot up to 5.2% compared to the implied fed funds rate of 2.2%.

The Fed was forced to add liquidity back to the overnight window to stabilize borrowing. It cut rates in September and again October. At the same time it started increasing the size of its balance sheet once more. The total rose from $3.8 trillion in mid-September to $4.2 trillion by the end of the year.

Now, I’m not saying that overnight rates will take off now like they did in 2019, but this is a warning shot to the Fed. Typically, the SOFR rate is stable. The recent jump tells the central bank it went too far in raising rates and shrinking its balance sheet.

As a result, it will be forced to reintroduce financial-system liquidity. The easiest way to do so is stop shrinking its balance sheet and start reinvesting the proceeds. By doing that, the Fed will flood lenders’ balance sheets with funds. In the process, Treasury prices will rise, and yields will fall.

And eventually, as yields drop, so will borrowing costs. The change will encourage individuals and companies to borrow once more, refinancing debt and reinvesting in their businesses. The process will help spur the next economic cycle and lead to a steady rally in the S&P 500.

Five Stories Moving the Market:

China pledged to upgrade industry and boost demand at an economic meeting that skipped unveiling new policies to combat major growth threats including a spiraling property crisis – Bloomberg. (Why you should care – China’s government is likely preparing to unleash stimulus next year to spur slowing economic growth)

Core consumer prices, which exclude volatile food and energy items, likely rose 0.3% in November from the prior month and 4% from a year earlier; that monthly gain would be a slight acceleration, potentially complicating the Federal Reserve’s ability to ease policy anytime soon – WSJ. (Why you should care – the central bank bases policy decisions on core prices so it wants to see the annual pace of growth drop to 2%)

Brazil’s annual inflation rate fell to within the central bank’s target range as policymakers ready a fourth straight interest rate cut at Wednesday’s meeting – Bloomberg. (Why you should care – this is another sign that global growth continues to slow, and the central bank rate-hike tide is turning)

German investor morale improved in December, the ZEW economic research institute said on Tuesday, as expectations grew for an interest rate cut by the European Central Bank in the medium term – Reuters. (Why you should care – this is a signal that European investors are increasingly optimistic about the economic outlook)

The path U.S. consumers expect inflation to take over the next year softened in November to the lowest level in more than two years, amid retreating projections of higher gasoline and rental costs, a New York Federal Reserve survey showed – Reuters. (Why you should care – the data tells the Federal Reserve that inflation expectations aren’t anchored at high levels, opening room for rate cuts down the road)

Economic Calendar:

U.K. – Jobless Claims for November (2 a.m.)

Eurozone – ZEW Economic Growth Expectations for December (5 a.m.)

Germany – ZEW Economic Growth Expectations for December (5 a.m.)

NFIB Small Business Optimism (6 a.m.)

CPI for November (8:30 a.m.)

Real Average Hourly Earnings for November (8:30 a.m.)

ECB’s Villeroy Speaks (12 p.m.)

Monthly Budget Statement for November (2 p.m.)

American Petroleum Institute Crude Oil Inventory Data (4:30 p.m.)

Treasury Auctions $70 Billion in 42-Day Bills

Treasury Auctions $21 Billion in 30-Year Bonds