The Real Rate Cushion: Why the Fed's Not Close to Done

Fed Chair Powell signaled QT’s about to end.

Policymakers are increasingly worried about a declining labor market.

Those statements imply an improved liquidity outlook.

With inflation steady and employment softening, the Fed’s policy runway looks longer than most expect…

This week has been an important one from a monetary outlook perspective. The rate-setting Federal Open Market Committee (“FOMC”) is scheduled to meet again on October 28–29. And due to the sensitivity of the discussion, central bank officials will enter a policy commentary blackout period starting this weekend.

That means the remarks made by voting members at various conferences over the past week are the last signals we’ll get on how they plan to vote. Based on those statements, FOMC Vice Chair John Williams (New York), Christopher Waller (Board Member), Austan Goolsbee (Chicago), Michelle Bowman (Board Member), Alberto Musalem (St. Louis), Stephen Miran (Board Member), and Susan Collins (Boston) all appear to support another rate cut. In other words, at least seven of the twelve voters are in favor.

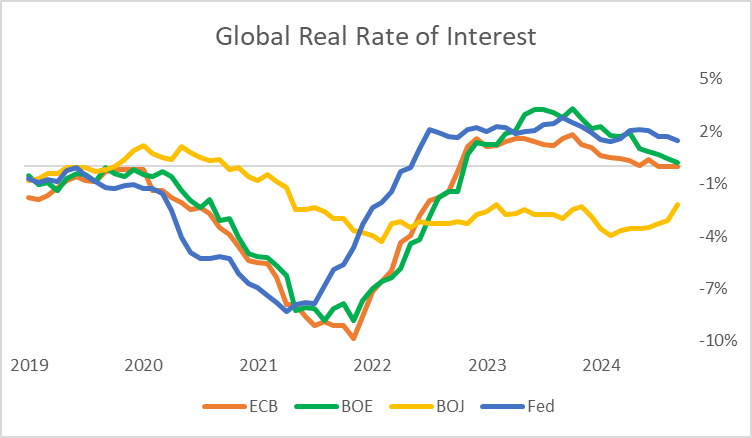

Considering the Fed currently holds the highest real rate (interest rates minus inflation) among the major global central banks, such a move shouldn’t fuel inflation growth…

But the icing on the cake came from Fed Chair Jerome Powell. Speaking at a conference in Philadelphia, he signaled policymakers are prepared to do more to support the labor market. He also confirmed the central bank is ready to end quantitative tightening (“QT”).

Powell’s remarks typically reflect the consensus view. With eight of the twelve voting FOMC members backing rate cuts, that certainly seems to be the case. At the same time, ending QT is another form of policy easing. Together, these shifts should make it easier for businesses and households to access liquidity. That should help support a steady rally in the S&P 500 Index

But don’t take my word for it, let’s look at what Powell said…

While giving a speech to the National Association for Business Economics, Powell discussed the Fed’s balance sheet. He explained the importance of using added liquidity as an effective policy tool to support economic growth. When the balance sheet expands—through the purchase of U.S. Treasurys and mortgage-backed securities—it drives down yields and borrowing costs. That supports the availability of credit to households and businesses. In other words, it’s akin to cutting interest rates.

However, when the economy no longer needs the additional assistance provided by balance sheet expansion, the opposite proves true. The central bank must stop buying bonds and shrink its balance sheet. Instead of outright selling the securities, the Fed lets them mature, receives the proceeds, and doesn’t reinvest them. As a result, the lack of buying power in the bond market can cause prices to drop and yields to rise. The shift tightens lending conditions and slows economic growth. Thought of another way, it’s like raising interest rates.

Powell said the recent balance sheet drawdown should end in the next couple of months. He stated that banking reserves are approaching equilibrium. In other words, policymakers feel there are ample funds available to borrow overnight. That helps stabilize interest rates.

The Fed chair then shifted to the outlook for the economy…

He noted that despite the lack of government data, inflation growth hasn’t changed much since before the shutdown. He also stated that domestic output growth appears to have increased. However, he said downside risks to the employment outlook have grown. Available data indicate both layoffs and hiring remain low, while perceptions of future hiring continue to worsen.

As a result, policymakers feel the rising downside risks to hiring now outweigh inflation concerns. They’re worried that by not easing rates in the current environment, they’ll be forced to take more aggressive action later. Hence the rate cut at the September monetary policy meeting.

Powell elaborated that policy must continue to move away from restrictive (which weighs on inflation growth) and more toward neutral (which neither hurts nor helps economic growth) to support job growth. He said policymakers are more willing to make adjustments in support of employment. In other words, the Fed is likely to ease again in October—and beyond.

So, let’s look at what kind of cushion the Fed has…

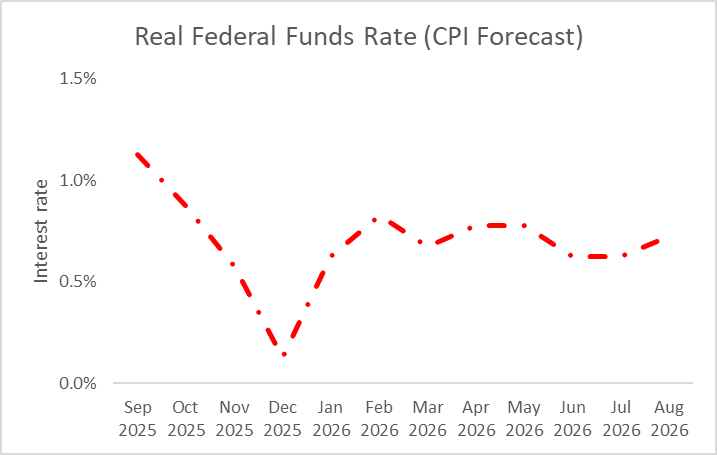

Based on the bond market’s current expectation for four more rate cuts by next August, our central bank could still wind up with additional easing potential…

I built the above forecast using a 0.2% monthly growth rate for the U.S. Bureau of Labor Statistics’ Consumer Price Index (“CPI”). It’s been growing right around that rate for the last six months. I then factored in current bond market expectations for rate cuts over the next year. I forecast the potential real rate by subtracting inflation from the fed funds forecast.

As you can see, inflation would still rise heading into the end of this year. But then, as hot CPI data from early 2025 starts to drop off, the real rate would rise again—even in the face of rate cuts. By next August, we could see four 25-basis-point reductions and still have a real rate of 0.75%. If we factor in the average real rate of -0.6% since 2000, our central bank would have over 130 basis points worth of room to ease.

At the end of the day, fading employment is the bigger problem.

Inflation growth isn’t yet back to target, but if the Fed doesn’t support the job market, spending could start to fall apart, and the broader economy with it. At that point, inflation will be the least of the central bank’s worries.

By taking proactive steps now, policymakers can avoid more drastic cuts later. The change should support the outlook for improving liquidity, borrowing, spending, and growth. All of that demand should underpin job gains—and support a steady rally in the S&P 500.

Five Stories Moving the Market:

The Japan Innovation Party (Ishin) is eyeing up a coalition with the ruling Liberal Democratic Party in a move that would set LDP leader Sanae Takaichi on the path to become prime minister while offering greater stability for a government led by her – Bloomberg. (Why you should care – Takaichi favors liberal fiscal and monetary policy, which could weigh on the yen while boosting stocks)

With U.S. technology companies pushing for AI dominance at warp speed, the “Bring Your Own Power” boom is a quick fix for the gridlock of trying to get on the grid; it’s driving an energy Wild West that is reshaping American power – WSJ. (Why you should care – data centers will likely rely on self-funded power sources until the national infrastructure can catch up, boosting demand for natural gas)

U.S. economic activity was little changed, and employment was largely stable in recent weeks even as more businesses reported headcount reductions, according to the Federal Reserve’s Beige Book survey, reinforcing concerns about labor market softening – Reuters. (Why you should care – the anecdotal commentary supports the case for further interest rate cuts)

U.S. Treasury Secretary Scott Bessent proposed a longer pause on high U.S. tariffs on Chinese goods in return for Beijing putting off its recently announced plan to tighten limits on critical rare earths – Bloomberg. (Why you should care – such an outcome would ease concerns around slowing global growth and rising inflation)

South Korea and the United States made “meaningful progress” in negotiations over $350 billion of investments in the U.S. that Seoul pledged in a deal reached in July to secure reduced U.S. trade tariffs, according to Korea’s top policy adviser Kim Yong-beom – Reuters. (Why you should care – U.S. Treasury Secretary Scott Bessent said he expects a trade deal with South Korea to be announced soon )

Economic Calendar:

Earnings: BK, CSX, KEY, IBKR, MTB, TRV, TSM, USB

BOJ’s Tamura (Board Member) Speaks

U.K. - GDP for August (2 a.m.)

U.K. – Industrial, Manufacturing Production (MoM) for August (2 a.m.)

U.K. – Exports, Imports for August (2 a.m.)

U.K. - BOE Credit Conditions Survey (4:30 a.m.)

Fed’s Barkin (Richmond) Speaks (8 a.m.)

U.S. - Philadelphia Fed Manufacturing Index for October (8:30 a.m.)

U.S. - PPI for September (8:30 a.m.) (Likely Delayed)

U.S. - Retail Sales for September (8:30 a.m.) (Likely Delayed)

U.S. - Initial Jobless Claims (8:30 a.m.) (Likely Delayed)

U.S. - Continuing Claims (8:30 a.m.) (Likely Delayed)

BOE’s Mann (Board Member) Speaks (9 a.m.)

Fed’s Barr (Board Member) Speaks (9 a.m.)

Fed’s Waller (Board Member) Speaks (9 a.m.)

Fed’s Bowman (Board Member) Speaks (10 a.m.)

BOE’s MPC Mann (Board Member) Speaks (10:45 a.m.)

ECB’s Lane (Chief Economist) Speaks (11:45 a.m.)

ECB’s Lagarde (President) Speaks (12 p.m.)

Fed’s Barkin (Richmond) Speaks (12:45 p.m.)

BOC’s Macklem (Governor) Speaks (1:30 p.m.)

Fed’s Balance Sheet Update (4:30 p.m.)

Fed’s Kashkari (Minneapolis) Speaks (6 p.m.)