The Federal Reserve signaled more rate cuts this year.

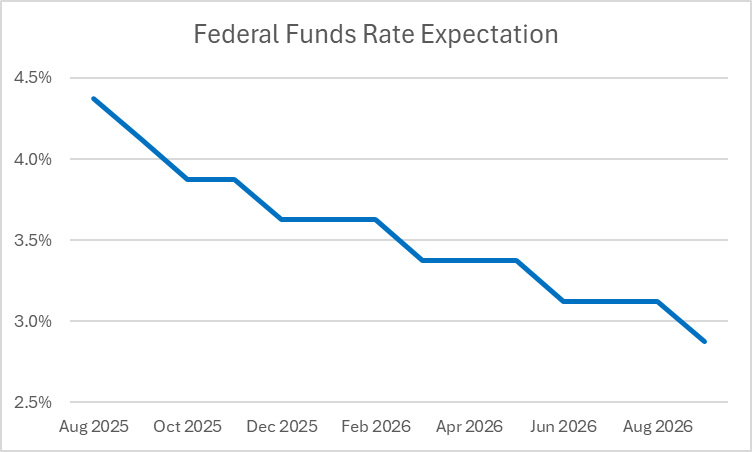

Wall Street anticipates several in 2026 as well.

The Fed’s makeup will soon lean more dovish.

The Federal Reserve just handed investors a gift, and it’s wrapped in dovish rhetoric…

Earlier this week, Fed Chairman Jerome Powell gave investors exactly what they wanted: a 25-basis-point rate cut and a signal that monetary policy could ease further before the year is out. As part of the Summary of Economic Projections, the median forecast from central bank officials showed that interest rates could drop by another 25 basis points at each of the final two meetings this year.

Based on the CME Group’s FedWatch tool forecast heading into the announcement, this was precisely what bond market speculators had expected…

Now, the bear case is that central bank policymakers only endorsed one added rate cut in 2026, unchanged from the prior forecast in June. Meanwhile, bond market speculators are currently pricing in three more rate cuts over the course of 2026. The naysayers argue that Wall Street’s outlook and that of policymakers aren’t aligned. So, they’re questioning how the stock and bond markets can keep rallying.

However, that argument overlooks two key factors: Powell’s language grew increasingly cautious on the employment outlook, and the makeup of the Fed is set to shift next year. Those two dynamics will likely sway policymakers to cut rates further, easing borrowing costs for businesses and households. That shift will support economic growth, encourage more hiring, and underpin a steady rally in the S&P 500 Index.

But don’t take my word for it—let’s look at what the data’s telling us…

After years of helping money managers and retail investors separate the signal from the noise, you learn quickly that people have short attention spans. Listening to a Fed press conference isn’t exactly a preferred activity for most. After all, it’s akin to watching paint dry.

Still, the nuanced detail that comes out is important as it relates to the outlook for the economy and the markets. If policymakers signal that money will become easier to borrow, that means more spending on goods, services, and investments. But if funds become harder to source, growth will likely stagnate, and asset prices will drop.

Wednesday's press conference wasn’t any different. The discussion felt typically dull, with reporters asking questions that didn’t pertain to the central bank’s role. Yet, Powell made three pointed statements that stood out to me:

It’s appropriate for interest rates to move toward neutral

Downside risks to the labor market have increased since July

Policymakers’ inflation expectations have eased compared to earlier this year

All three are critical when discerning the path forward. So far this year, the Fed has held back on easing because it felt tariffs made the economic outlook more uncertain. It believed the labor market remained strong and that progress on inflation had stalled. Policymakers wanted more clarity before acting.

Well, they’re starting to get it. They’ve said recent data shows downside risks to employment are rising, while inflation tied to tariffs increasingly looks like a one-time event. That’s important because a drop in hiring will hurt economic growth, while a temporary rise in inflation means growth should slow again as the numbers annualize. That gives the Fed room to cut moving forward.

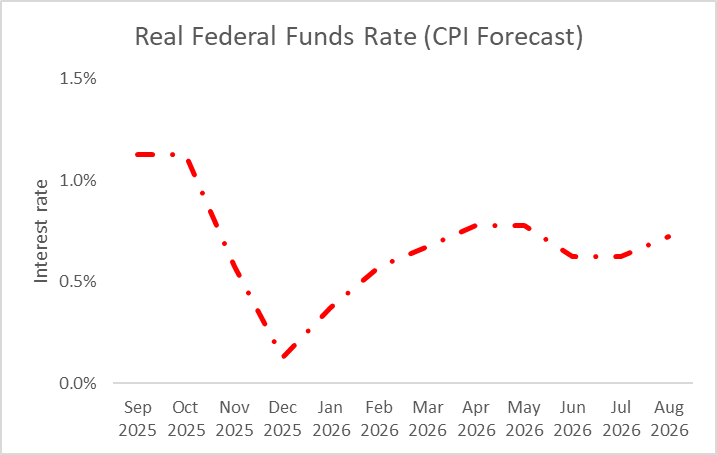

As for the neutral rate, that’s the point at which policy is neither helping nor hurting economic growth. It’s effectively the federal funds rate minus the rate of annualized inflation. On a CPI basis (using the latest data), the Fed had roughly 150 basis points of downside before hitting neutral (4.4% fed funds minus 2.9% CPI) coming into this week’s meeting.

But let’s look at where it could go based on the six-month pace of CPI growth and Wall Street’s expectation for five more rate cuts by late next year…

Based on those numbers, the central bank would still have a real interest rate of 0.5%, meaning additional room to cut before hitting neutral. If we consider that the metric averaged -0.4% between 2000 and 2020, the rate cut potential could grow to 100 basis points.

Finally, consider next year's Federal Open Market Committee composition.

Powell’s term as Chairman expires in May 2026. At that point, he’ll be replaced by a White House appointee who will likely be more inclined to ease rates. While Powell’s board appointment runs through January 2028, it’s typical for a Chair to resign once their term ends. If that happens, the White House will have another seat to fill—again, likely with someone favoring more cuts.

Meanwhile, the voting seats of the regional Fed presidents will change at the start of next year. Currently, those rotating spots are held by two notable hawks—Jeffrey Schmid (Kansas City) and Austan Goolsbee (Chicago)—and by two others—Alberto Musalem (St. Louis) and Susan Collins (Boston)—who are slightly hawkish but have recently voiced concerns about falling employment.

They’ll be replaced by Anna Paulson (Philadelphia), Beth Hammack (Cleveland), Laurie Logan (Dallas), and Neel Kashkari (Minneapolis). While Paulson is an unknown, the other three lean hawkish. Still, their tone appears more pragmatic than Schmid and Goolsbee, which should tilt the FOMC in a more dovish direction next year.

Not to be forgotten is Stephen Miran’s term, which expires in January 2026. Whether he stays or goes is more or less a wash, as the seat should remain firmly dovish.

Because of this dynamic, Wall Street expects the FOMC’s makeup to tilt more in favor of rate cuts once Powell’s term ends. That’s why two added rate cuts are priced in for next year—starting in June—compared to the Fed’s latest median forecast for just one.

While the headlines may focus on Powell’s press conference or the dot plot divergence, the real story is unfolding beneath the surface—monetary policy is loosening., the Fed’s composition is changing, and the market is already pricing in a more accommodative future. For investors willing to look past the noise, the setup is constructive and should underpin a steady rally in risk assets like stocks.

How We’re Going to Profit

Keep reading with a 7-day free trial

Subscribe to The Intrepid Investor's Guidebook to keep reading this post and get 7 days of free access to the full post archives.