The Year-End Setup Is Hiding in Plain Sight

September is typically the S&P 500’s worst performance month.

October through January tends to see the best stretch for positive returns.

December has the best percentage record of a positive outcome.

Don’t be surprised by a fourth quarter rally….

We’re quickly approaching the end of the year. For you and me, that might mean the holidays are right around the corner, and we’re looking forward to time with our families. I know my kids have already started building Christmas present wish lists, and it’s not even Halloween.

But for Wall Street, the end of the year means one thing: performance reviews and bonuses. Money managers have spent the past nine months generating returns for their investors. The more money they make for their clients, the more they expect to get paid.

Now, they want to defend those returns. The last thing fund managers want is to see all that hard work go down the tubes—along with their year-end bonus. So typically, they’ll use the final quarter to protect performance. And that means a steady rally in the S&P 500.

But don’t take my word for it, let’s look at what the data’s telling us…

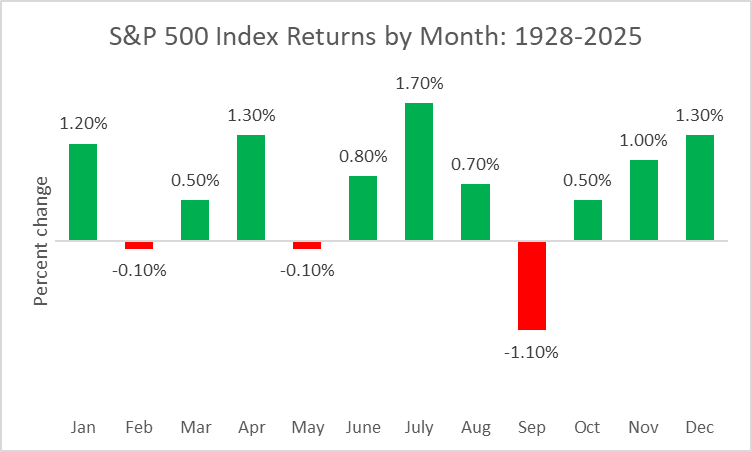

To see what I mean, look at the following chart.

It shows the S&P 500’s typical monthly return for every year since 1928. By observing this, we get a sense of what to expect as the year plays out.

To me, the first thing that stands out is the drop in September. It’s typically the weakest month of the year, with the S&P 500 tending to lose 1.1%. That’s why I warned in mid-August that a pullback was likely.

But the next thing I notice is what happens once September ends. Because afterward, in the next four months, we see the best stretch of stock market returns. From October through January, the S&P 500 usually gains 4%. The three-month run between June and August is the next best stretch, averaging 3.1%.

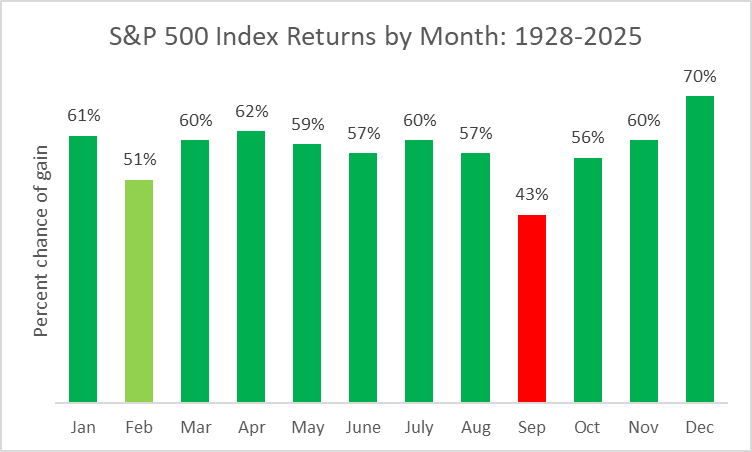

Further illustrating that point is the next chart, showing the S&P 500’s odds of producing a positive monthly return since 1928. September is the only month with odds below 50%. The chances improve greatly over the next four months…

However, the end of the year for money managers isn’t always straightforward. Depending on the fund’s charter, year-end can fall anywhere between October and December. In other words, everyone has a different timeline for closing the books.

That means many funds—hedge funds in particular—start locking in gains before year-end. By monetizing profits and reducing exposure to market risk, managers can anchor some level of performance. That way, they have a better idea of their payout potential.

This is why September tends to be volatile. Much of the risk reduction is happening. Once that’s out of the way, managers and traders can relax. At that point, they’re looking for opportunities to boost returns, not be a hero and blow it. This window is a good time to start posturing for the year ahead.

But hedge funds can make money by shorting stocks (betting against the market), while mutual fund managers typically can’t. So mutual funds are fighting with one hand tied behind their backs, so to speak, because they’re usually “long only.” In other words, they can only bet on stocks going up. If they’re going to defend their returns, now’s the time to do it.

We’re about to enter October, meaning 2025 is almost done. So far, the S&P 500 is up a little over 14% on a total return basis (dividends reinvested). That’s a tremendous year when you consider the index has returned 9.5% annually going back to 1928. In fact, the average long/short hedge fund manager is said to be up around 12% this year, according to Bloomberg. Wall Street won’t want to see that fade. They’ll do what they can to secure a decent payday.

That should help stabilize the stock market and support a steady rally in the S&P 500 into the start of 2026.

Five Stories Moving the Market:

The top four congressional leaders will meet with President Donald Trump at the White House today, a day before federal funding would expire if the two parties can’t agree on a short-term spending bill – Bloomberg. (Why you should care – an agreement would help the government to avoid a partial shutdown that could take place overnight Tuesday into Wednesday)

China’s President Xi Jinping is now chasing his ultimate prize: a change in U.S. policy that Beijing hopes could isolate Taiwan; as President Donald Trump has shown interest in striking an economic accord with China in the coming year, the Chinese leader is planning to press his American counterpart to formally state that the U.S. “opposes” Taiwan’s independence – WSJ. (Why you should care – such a policy shift would put the global semiconductor supply chain at risk and cutting-edge technology in China’s hands)

Federal Reserve Vice Chair for Supervision Michelle Bowman said the U.S. central bank should seek to achieve the smallest balance sheet possible and overhaul its regime for implementing monetary policy; Bowman argued that returning to a regime where the Fed is actively managing the balance sheet would give it better indications of market stress and functioning issues – Bloomberg. (Why you should care – shrinking the balance sheet would help to enhance the central banks’ economic crisis-fighting tools)

OPEC+ will likely raise oil output again in November as the group continues its strategy to reclaim global market share; the alliance led by Saudi Arabia will consider adding at least as much as the 137,000 barrel-a-day hike scheduled for October when it meets online October 5 – Reuters. (Why you should care – rising oil supply should help to keep a lid on gas prices and inflation growth)

Moody’s and Fitch Ratings both raised Spain’s sovereign credit rating citing an improving economy and a better labor market; Spain’s rating was upgraded one level to A from A- by Fitch, while Moody’s raised its rating to A3 from Baa1 - WSJ. (Why you should care – the shift should boost the economic outlook for Europe as a whole)

Economic Calendar:

BOJ’s Noguchi (Board Member) Speaks

Spain – CPI (Preliminary) for September (3 a.m.)

Riksbank (Sweden) Monetary Policy Meeting Minutes (3:30 a.m.)

U.K. – BoE Consumer Credit for August (4:30 a.m.)

ECB’s Nagel (Germany) Speaks (5 a.m.)

Eurozone – Consumer Confidence for September (5 a.m.)

Eurozone – Consumer Inflation Expectations for September (5 a.m.)

BOE’s Ramsden (Deputy Governor) Speaks (8 a.m.)

Canada – Manufacturing Sales for August (8:30 a.m.)

U.S. – Pending Home Sales for August (10 a.m.)

U.S. – Pending Home Sales Index for August (10 a.m.)

U.S. – Dallas Fed Manufacturing Business Index for September (10:30 a.m.)

Treasury Auctions $82 Billion in 13-Week Bills (11:30 a.m.)

Treasury Auctions $73 Billion in 26-Week Bills (11:30 a.m.)

Fed’s Williams (New York) Speaks (1:30 p.m.)

Fed’s Bostic (Richmond) Speaks (6 p.m.)