The Fed said it will slow the pace of its balance sheet unwind.

It will reduce the monthly runoff of maturing Treasurys to $5 billion.

That means it will reinvest $20 billion per month back into those bonds.

U.S. Treasury bond yields are headed lower…

Since mid-January, I’ve been highlighting the opportunity for a rally in Treasury bond prices. One of the catalysts for my optimism was commentary from Treasury Secretary Scott Bessent. He said the White House is focused on doing everything it can to lower the yield on 10-year U.S. Treasurys. He stated doing so would help to lower borrowing costs for households and businesses. After all, that’s the benchmark rate for many loans.

A second catalyst was the short position built by quant driven hedge funds. Commodity Trading Advisors and risk-parity funds were maximum short global 10-year sovereign bonds. In other words, those firms’ risk-tolerance and investing models were telling them there wasn’t any more room to keep shorting.

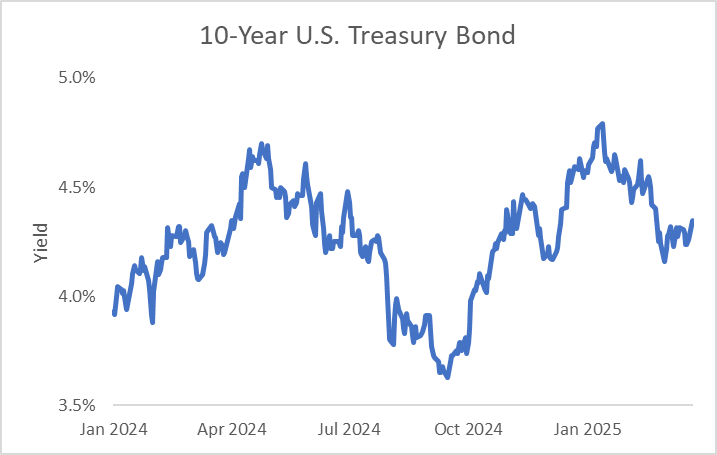

When positioning gets one-sided like that, it usually means the underlying asset is headed in the opposite direction. As you’ll notice in the following chart, mid-January is when the yield on 10-Year U.S. Treasury Bonds hit their recent peak…

But there was a third driver I highlighted in February that I felt would throw fuel on the fire. I pointed to the potential for the Federal Reserve to slow its balance sheet unwind process sooner than the expected mid-year announcement. And last week, we got just such an announcement from our central bank.

Chairman Jerome Powell said it would reduce the size of its Treasury bond unwind. That means it will begin increasing bond purchases once more rather than pocketing the cash from maturing investments. That will help to drive up prices and lower yields.

But don’t take my word for it, let’s look at what the data’s telling us…

The Fed has two main tools for implementing monetary policy… interest rates and balance sheet expansion. Rate setting is the more obvious of the two measures as it drives borrowing costs higher or lower. But for most people that aren’t finance professionals, balance sheet expansion is the less obvious tool.

You see, bond prices and yields have an inverse relationship. When the underlying price of a bond goes up, the payout falls. But when the bond price drops, the yield increases. For example, if you buy a $100 bond that pays a $5.00 coupon, the yield is 5%. But let’s say you sell that same bond at $110 to someone else. The new owner is still collecting a $5 coupon, but the yield has dropped to 4.5%. Conversely, if you had instead sold the bond at $90, the yield would have jumped to 5.6%.

The yield on 10-year Treasurys is important because it’s a commonly used rate for benchmarking all sorts of loans. So, the Fed can use bond prices as a way to convey its policy. If it expands its balance sheet holdings by buying Treasury bonds, it drives yields and borrowing costs down. But if it stops buying bonds, it allows yields and borrowing costs to rise once more.

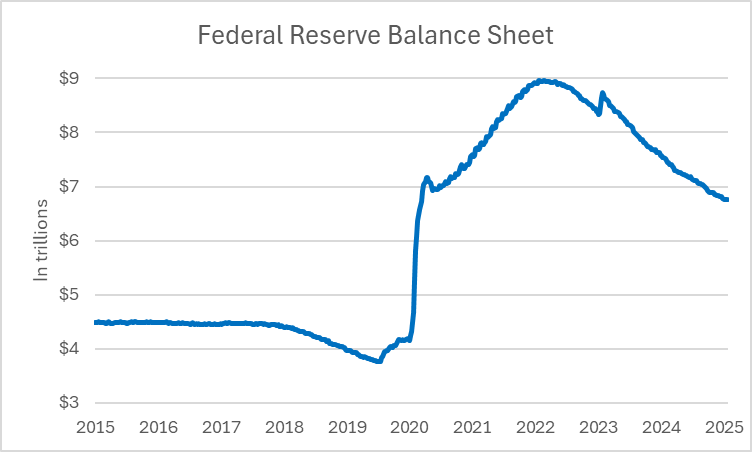

During COVID, our central bank wanted to make sure rates stayed low to support the economy. So, it began snapping up Treasurys to keep rates low. Not only that, but as those bonds matured, it reinvested the assets into even more Treasurys. As you can see in this next chart, the process caused the balance sheet to swell from less than $4 trillion in late 2019 to a peak of $9 trillion by mid-2022.

Since then, the Fed has been trying to shrink its balance sheet. With high inflation, it saw no need to keep borrowing costs super low. And at the same time, it wanted to reload its toolbox for the next crisis, so it has plenty of room to introduce economic support (aka balance-sheet expansion).

As you can see in the chart above, the size of the central bank’s balance sheet holdings has dropped. As of last week, the total was down to $6.8 trillion compared to the peak of more than $9 trillion. The new number isn’t back to pre-COVID levels, but it’s below the increase seen following a burst of stimulus to support the growth.

But the rapid drop has caused Fed officials to worry about banking system reserves…

Minutes from the January policy meeting showed the conversation may be changing. Staff noted that an agreement to increase the federal debt limit might cause overnight liquidity reserves to “decline quickly.” In fact, the Fed staff said it could create a situation where financial-system liquidity could fall below levels considered appropriate by the rate-setting Federal open Market Committee. In other words, it could place strains in the overnight market, causing rates to jump.

Now the debt ceiling was not part of the recent legislation to keep the government funded but it is still an ongoing debate in Congress. Members will need to raise it to ensure the government doesn’t default on its debt. The deadline is expected to be around mid-year. And Republicans are expected to make the legislation part of a broader reconciliation bill, meaning they won’t need Democratic votes.

So, last week, the central bank took a pre-emptive step…

As part of the latest policy announcement, the Fed said it will reduce the size of U.S. Treasury bond holdings it’s allowing to mature. Currently, it’s pocketing the cash on $25 billion worth of those assets per month. But last week, it said it would reduce that number down to just $5 billion, starting April 1. In other words, the world’s biggest buyer of U.S. sovereign debt, will begin reinvesting $20 billion into those assets once more.

If you were thinking now was a good time to lock in a high rate of return on a safe investment, well the central bank just confirmed that idea. Conversely, if you’re short Treasury bonds, that’s not the news you want to hear. So, your incentive to unwind that position just increased. But either way, all of the buying power means the same thing… lower yields and higher bond prices.

Five Stories Moving the Market:

President Donald Trump said that he might soften reciprocal tariffs he plans to impose on U.S. trading partners next month, and that some nations might be exempt; he said the reciprocal tariffs could stop short of his pledge to equalize U.S. duties with rates other nations charge – WSJ. (Why you should care – the removal of tariff uncertainty could help to dispel some of the worst-case scenarios, causing momentum investors to increase U.S. risk exposure)

Blackstone President Jon Gray warned investors against making knee-jerk decisions around President Donald Trump’s tariff drama and instead advised waiting to see how the underlying negotiations play out – Bloomberg. (Why you should care – Gray said investors making long-term asset allocation decisions should avoid getting caught up in the short-term turmoil)

Bank of England Governor Andrew Bailey said artificial intelligence had the potential to be a game-changer for Britain and the global economy just as electricity was around the start of the 20th century; Bailey said technologies that were transformative continuously improved, lowered costs and made innovation easier, boosting productivity – Reuters. (Why you should care – increased productivity related to AI uptake should continue to boost demand for high-end semiconductors)

President Donlad Trump for the second time in five days called for lower rates from the Federal Reserve, turning up the pressure on the central bank; he stressed that grocery and energy prices are coming down during a cabinet meeting – yahoo!finance. (Why you should care – the Fed wound up lowering interest rates when Trump previously introduced tariffs)

U.S. economic activity expanded at a faster pace in March as strength in services offset an unexpected downturn in manufacturing; the S&P Global Flash U.S. Composite PMI rose to 53.5 this month from 51.6 in February, as business activity rose to its highest level in three months – WSJ. (Why you should care – companies had difficulty passing on price increases due to increased competition)

Economic Calendar:

BOJ Meeting Minutes

Germany – Ifo Business Climate Index for March (5 a.m.)

U.S. – Building Permits for February (8 a.m.)

Fed’s Kugler (Board Member) Speaks (8:40 a.m.)

U.S. – FHFA House Price Index for January (9 a.m.)

U.S. – S&P CoreLogic Case-Shiller Home Price Index for January (9 a.m.)

Fed’s Williams (New York) Speaks (9:05 a.m.)

U.S. – New Home Sales for February (10 a.m.)

U.S. – Richmond Fed Manufacturing Index for March (10 a.m.)

Treasury Auctions $70 Billion in 6-Week Bills (11:30 a.m.)

ECB’s Nagel (Germany) Speaks (12 p.m.)

Treasury Auctions $69 Billion in 2-Year Notes (1 p.m.)

Fed’s Williams (New York) Speaks (2:35 p.m.)

U.S. - American Petroleum Institute Crude Oil Inventory Data (4:30 p.m.)

Not since Vance dissed Europe, which may now be less inclined to invest in US Treasury Bonds…